The general ledger and general journal are two of the most fundamental concepts in accounting and bookkeeping. Though they sound similar and serve complementary purposes there are some notable differences between the two that are important to understand. In this comprehensive guide we’ll break down what each one is, how they work, and the key differences between general ledger vs general journal.

What is a General Journal?

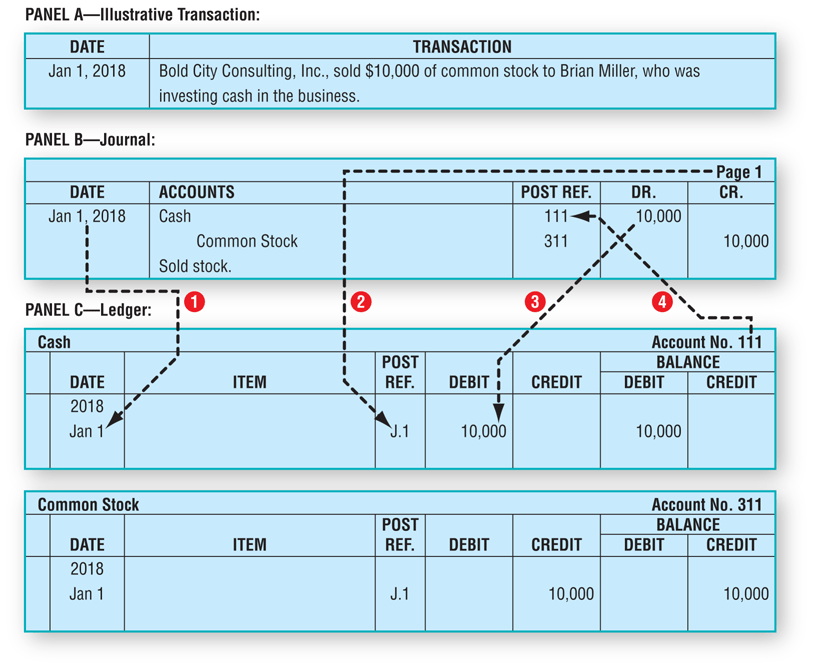

A general journal is the first point of entry for recording financial transactions in the accounting process. It’s a chronological log where transactions are recorded in order by date. The general journal follows the double-entry method of bookkeeping, meaning each transaction is entered with a debit to one account and a credit to another.

Some key details about general journals

- Records all transactions in chronological order

- Follows double-entry accounting method

- Has columns for date, account names, serial numbers, debits/credits

- Records miscellaneous transactions not logged in specialized journals

- Entries are made manually or automatically via accounting software

A general journal provides a comprehensive look at all business transactions, acting as a historical record that can be referenced as needed. This gives accountants visibility into the types of transactions taking place and when. Journals are manually maintained in accounting books or automatically created in computerized accounting systems.

What is a General Ledger?

Whereas journals chronologically log transactions as they occur, ledgers summarize transaction data by account. The general ledger is the master set of accounts used to compile the financial statements. It contains aggregate debit and credit balances for asset, liability, equity, revenue and expense accounts.

Some key details about general ledgers:

- Summarizes transaction data by account type

- Tracks balances for asset, liability, equity, revenue, expense

- Has T-shaped account tables with debits on the left and credits on the right

- Aggregates data from journals to create the trial balance

- Maintained manually or in accounting/ERP software

The ledger provides a big picture overview of account balances that informs the preparation of the income statement and balance sheet. While transaction-level details are recorded in journals, ledgers give visibility into the net debit/credit activity across all accounts. Entries are posted to the general ledger accounts after being recorded in the appropriate journal.

Key Differences Between General Ledger and General Journal

Now that we’ve defined what each one is individually, let’s look at some of the main differences between general ledger and general journal:

Order of Entry

The first difference comes down to order of entry. Transactions are initially recorded in the general journal in chronological order. Then, the journal entries are posted to the corresponding general ledger accounts.

Level of Detail

Journals provide granular transaction-level details including date, account(s), description, and amount. Ledgers summarize all activity by account, showing just the net debit/credit balance.

Structure

Journals typically have columns for date, description, account name, debit/credit amount. Ledgers use T-shaped account tables with the account name at the top and debits on the left and credits on the right.

Broad vs. Specific Focus

General journals record all miscellaneous transactions not logged in specialized journals. General ledgers aggregate activity across various journals into account balances.

Purpose

Journals chronologically log raw accounting data. Ledgers classify and summarize transaction data by account.

Medium

Journals were traditionally paper-based books but are now digital. General ledger info was manually compiled but is now maintained in accounting systems.

Reporting

Journals provide transaction-level details. Ledgers inform the trial balance and financial statements by providing ending account balances.

As you can see, while journals and ledgers complement each other in the accounting process, they serve different purposes and offer unique views of the company’s financial data.

Real-World Examples

To better illustrate how general ledgers and journals work together, let’s walk through some real-world examples.

Example 1

Acme Company takes out a new $10,000 business loan from First National Bank on March 5, 2022.

- In the general journal, this would be recorded with the date, accounts, and debit/credit amounts:

Date | Debit | Credit3/5/2022 | Cash - $10,000 | Notes Payable - $10,000 - In the general ledger, it would show up as:

CashDebit | Credit10,000Notes PayableDebit | Credit 10,000Example 2

On March 7, 2022, Acme sells $5,000 worth of product to a customer and receives payment in cash.

- The general journal entry would show:

Date | Debit | Credit3/7/2022 | Cash - $5,000 | Revenue - $5,000- The general ledger would summarize it as:

Cash Debit | Credit15,000 RevenueDebit | Credit5,000Example 3

On March 10, 2022, Acme pays $1,000 for monthly utilities.

- The journal entry would be:

Date | Debit | Credit 3/10/2022 | Utilities Expense - $1,000 | Cash - $1,000- The ledger would show:

CashDebit | Credit 14,000Utilities ExpenseDebit | Credit1,000As you can see from the examples above, the journal provides the detailed, chronological transaction record while the ledger summarizes the account activity.

Key Takeaways

- General journal records transactions chronologically

- General ledger summarizes transactions by account type

- Journals provide granular details; ledgers show net balances

- Journals log all transactions; ledgers focus on account activity

- Journal entries are posted to the corresponding ledger accounts

- Journals offer transaction record; ledgers inform financial statements

While journals and ledgers serve unique purposes, they work together to paint a comprehensive picture of the finances and transactions of the business. Maintaining both provides visibility into granular accounting data and high-level trends across accounts.

The general ledger and general journal are core components of the accounting process. Though they are distinctly different, they work in tandem to log, classify, summarize, and report on business transactions. While new technology and accounting software has streamlined the process, the basic functionality of journals and ledgers remains critical.

Understanding the key differences between general ledger and general journal provides insight into how the double-entry accounting system works. It also allows accounting professionals to leverage these tools appropriately to record granular accounting data, track account activity, and accurately report on company finances.

Difference Between a General Ledger and a General Journal

The general ledger and the general journal are key elements of a companys financial record-keeping system, serving different functions.

General Journal

The general journal, often simply called the journal, is a chronological record where all the companys transactions are initially recorded. Each entry in the journal typically includes the date of the transaction, the accounts affected, the amounts to be debited or credited from each account, and a brief description of the transaction. This process is known as journalizing.

General Ledger

The general ledger, or ledger, is the primary accounting record of a company which is used to sort, store and summarize the company’s transactions. Unlike the journals chronological format, the ledger groups transactions by account.

For example, all transactions involving cash will be posted from the general journal to the cash account in the general ledger. Similarly, all transactions that involve sales revenue will be posted to the sales revenue account in the general ledger, and so on for every account.

Key Differences

- Purpose: The general journal is used for recording all the companys transactions in chronological order, while the general ledger is used for sorting, storing, and summarizing these transactions by account.

- Structure: The general journal is organized chronologically, while the general ledger is organized by account.

- Level of Detail: Each entry in the general journal includes a detailed description of the transaction, while the general ledger typically contains less detail for individual transactions but provides a summary of all transactions for each account.

In a typical accounting cycle, transactions are first recorded in the general journal, then posted to the relevant accounts in the general ledger. Balances from the general ledger are then used to prepare the trial balance, financial statements, and other reports. This flow of information ensures that the companys financial records are accurate, complete, and up-to-date.