Reserves are part of profits or gain that has been allotted for a specific purpose. Reserves are usually set up to buy fixed assets, pay bonuses, pay an expected legal settlement, pay for repairs & maintenance and pay off debt.

In accounting, a reserve refers to a portion of retained earnings that has been set aside for a specific purpose Reserves provide companies with a useful tool for financial planning and risk management.

This article will explain what reserves are, the types of reserves, how to create them, and how they are presented on financial statements.

What is the Purpose of Reserves?

Reserves serve several key purposes

-

Earmark funds for future needs – A company can reserve profits to save for known or likely future expenditures, such as expanding operations, replacing equipment, or settling litigation. This ensures funds are on hand when needed.

-

Smooth earnings – Setting aside reserves in profitable years provides a cushion for leaner times. Companies can use reserves to maintain dividend payments despite dips in income.

-

Signal financial prudence – Reserves demonstrate a conservative approach to investors. A healthy reserve balance inspires confidence in a company’s stability.

-

Meet regulatory requirements – In some cases, reserves are mandated by law or accounting standards. Banks must maintain loan loss reserves, for example.

Overall, reserves give companies greater control over retained earnings for needs ranging from discretionary saving to required risk management.

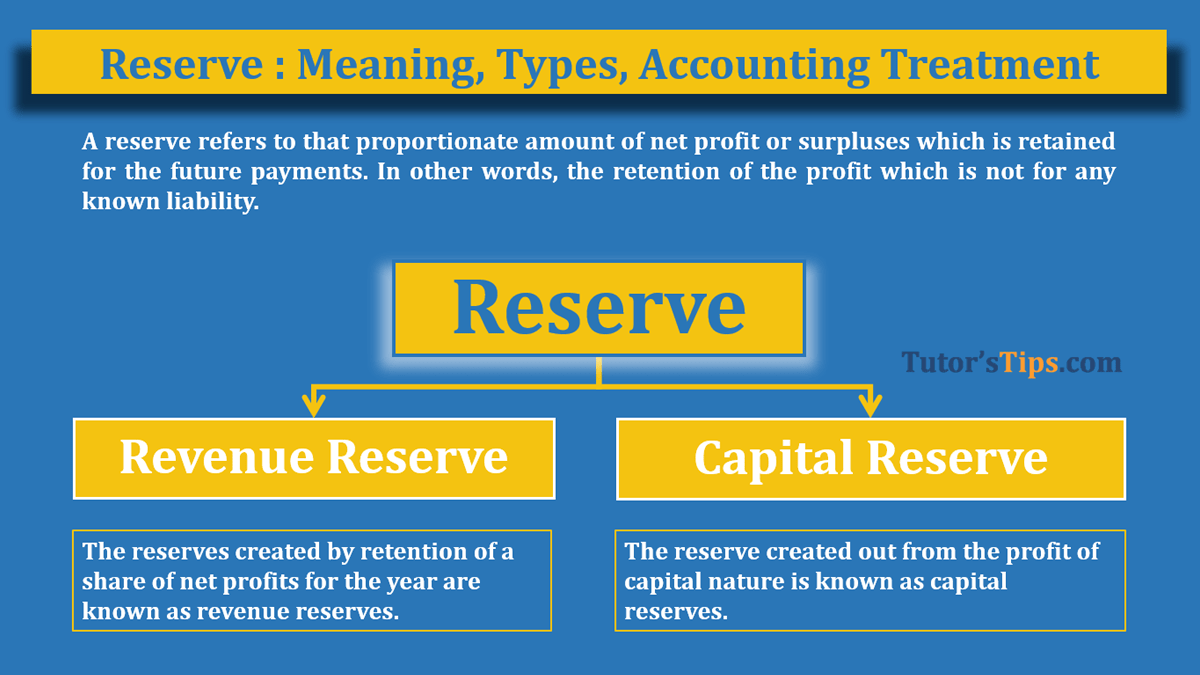

Types of Reserves

There are two major categories of reserves:

1. Capital Reserves

Capital reserves come from sources unrelated to regular operations. Typical sources include:

- Sale of fixed assets above their book value

- Stock issuance above par value

- Premiums on new share issues

- Gains from mergers and acquisitions

Capital reserves cannot be used to pay cash dividends. The funds are reserved solely to strengthen the company’s finances.

2. Revenue Reserves

Revenue reserves are appropriations of surplus from operating activities. Common examples include:

-

General reserve – A generic reserve for any future purpose. Most flexible use.

-

Dividend equalization reserve – Smooths dividend payments when profits fluctuate.

-

Contingency reserve – Covers possible losses from risks like lawsuits.

-

Loan loss reserve – Absorbs loan defaults at banks. Required by regulators.

-

Inventory reserve – Offsets obsolete or damaged goods.

Revenue reserves offer flexibility within rules set by management or external standards.

How are Reserves Created?

A board resolution is needed to establish a reserve. The entry debits retained earnings and credits the reserve account for the same amount. For example:

Retained Earnings $100,000

Reserve for Equipment Replacement $100,000

This transfers $100,000 from retained earnings to the reserve. The process reverses when funds are deployed.

Boards can create reserves at their discretion based on business needs and financial priorities. There are no universal standards dictating optimal reserve levels or uses.

Reserve Presentation on Financial Statements

Reserves appear on the balance sheet under the equity section. They aren’t separated from retained earnings. For example:

Retained Earnings

Beginning balance $1,500,000

Net income $250,000

Transfer to reserve ($100,000)

Ending balance $1,650,000

Notes may break out reserves included in this ending total. But reserves aren’t reported as distinct line items.

The income statement will also show the transfer reducing net income available for retention.

Benefits and Limitations of Reserves

Key benefits of reserves include:

- Forces savings for future needs

- Attracts investors with conservative policies

- Allows flexibility in using retained earnings

Potential limitations are:

- Excess reserves can depress stock price by reducing dividends

- No legal restrictions on using reserved funds

- Reserves can smooth earnings to misrepresent performance

Overall, used strategically, reserves grant companies significant financial control and stability.

Examples of Reserves in Action

Here are a few examples of reserves employed:

-

A clothing retailer sets aside an inventory obsolescence reserve to dispose of unsold seasonal items.

-

An oil company establishes a decommissioning reserve to fund retiring depleted fields.

-

A manufacturer creates a warranty reserve to offer repairs for a set period after sales.

-

A fast food chain boosts its litigation reserve to cover damages from a class action lawsuit.

-

A bank increases its capital reserve when regulators demand larger loss provisions.

Each scenario shows reserves targeting financial risks unique to that business.

Key Takeaways on Reserves

-

Reserves are portions of retained earnings allocated for specific purposes.

-

Common reserves include those for dividends, contingencies, equipment, litigation, and regulatory requirements.

-

Boards create reserves through retained earnings transfers disclosed in footnotes.

-

Reserves grant financial flexibility but aren’t legally restricted funds.

Understanding reserves empowers more strategic use of retained profits to control risks and optimize growth.

Frequently Asked Questions About Reserves

1. What is the difference between a reserve and a provision?

Provisions are estimated liabilities booked under accrual accounting. Reserves are equity accounts that set aside retained earnings. Provisions impact net income; reserves don’t.

2. Are reserves listed separately on the balance sheet?

No, reserves are included in the retained earnings or similar total equity line. Details may be given in footnotes.

3. Can reserves appear on the asset side of the balance sheet?

Extremely unlikely. Reserves arise from profits and reduce equity. Assets represent economic resources, which reserves are not.

4. Do reserves guarantee funds will only be used per their title?

No. Reserves are an informal designation with no legal standing. Boards can deploy reserved funds for any purpose.

5. Is there an ideal reserve percentage of retained earnings?

No set rule. Reserves depend on factors like industry, profit margins, growth plans, and risk exposures. Conservatism suggests at least 10-20%.

Conclusion

Reserves provide companies with a useful tool for disciplined financial management. Setting aside retained profits to hedge risks, smooth earnings, and save for the future provides stability. Boards should actively assess reserve needs rather than passively let profits accumulate. Astute reserve policies demonstrate prudence to investors while empowering strategic growth.

What are Reserves in Accounting?

When an enterprise earns a profit during the end of a year, a certain part of it is retained in the trading concern to meet future exigencies, growth outlooks etc., The amount of money that is kept aside is known as Reserves in Accounting.

They assist in securing the financial situation of an enterprise and can be utilised for different purposes such as stable dividend repayments, expansion, meeting contingencies, legal requirements, investments, improving the financial situation, etc., It is also termed as retained earnings.

For instance – Reserve for Dividends Equalisation, General reserve, Reserve for Increased Cost of Replacement, Reserve for Expansion, etc.,

It is shown on the liability side of a balance sheet (B/S) below the heading ‘Reserves and Surplus’ with capital if an enterprise suffers losses, then it is not created.

- Capital Reserve

- Revenue Reserve

What is Capital Reserve?

The capital reserve is established out of capital profits and are normally not allocated as dividends to the shareholders. It cannot be established out of profits acquired from core operations of an enterprise.

- Profit earned before an enterprise’s embodiment

- Premium acquired on the issue of debentures and shares

- Gain on re-issuance (redistribution) of forfeited shares

- Profit kept aside for redemption of debentures or preference shares

- Gain on sale of fixed assets

- The surfeit on revaluation of liabilities and assets

- Capital redemption reserve