Labor price variance, or direct labor rate variance, measures the difference between the budgeted hourly rate and the actual rate you pay direct labor workers who directly manufacture your products. Labor efficiency variance measures the difference between the number of direct labor hours you budgeted and the actual hours your employees work. Compare these two variances to determine how well your small business managed its direct labor costs during a period.

Understanding labor variances is a crucial yet often overlooked aspect of managing labor costs for a business. At its core, a labor variance measures the difference between the actual labor cost incurred during a period versus the standard or budgeted labor cost. There are two main types of labor variances – labor efficiency variance and labor price variance. While they may sound similar at first glance, understanding the key differences between these two variances can have a significant impact on monitoring and controlling direct labor costs.

In this comprehensive guide we will break down exactly what labor efficiency and labor price variances are, how to calculate them, and most importantly – how to interpret the results to make better decisions for your business. Whether you are an accounting manager or small business owner this guide aims to demystify labor variances so you can leverage them as a useful labor cost analysis tool.

What is Labor Efficiency Variance?

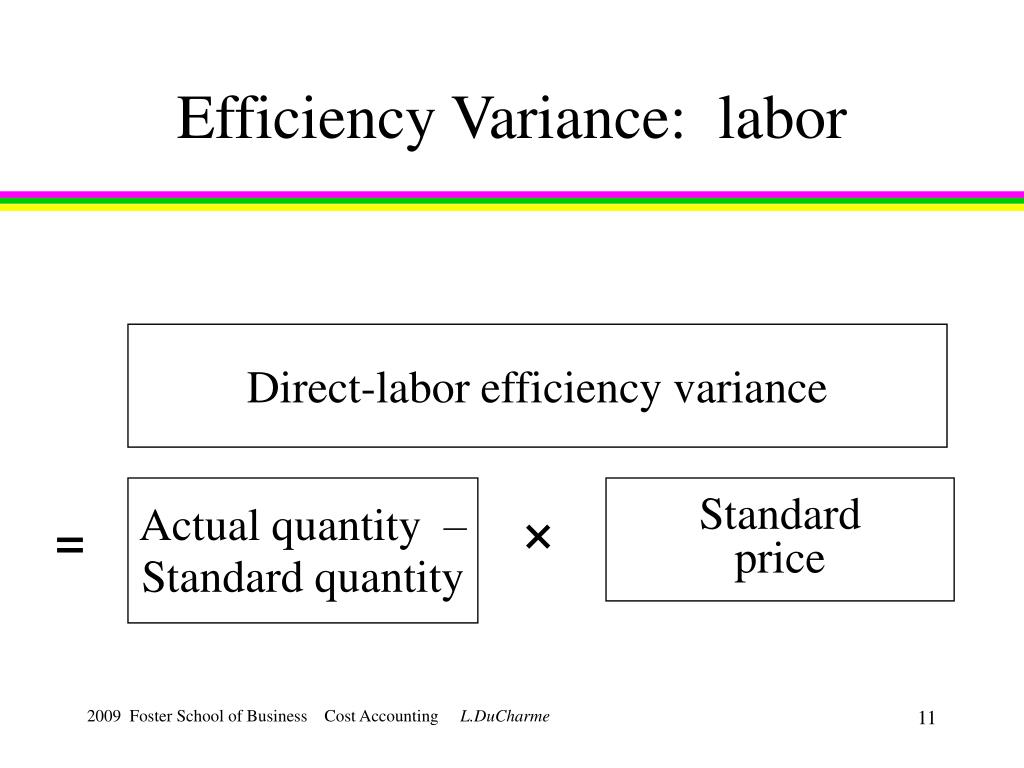

Labor efficiency variance specifically measures the difference between the standard hours allowed for the actual output achieved versus the actual hours worked, It focuses entirely on the variable of time – evaluating if workers are meeting expected productivity standards

The formula to calculate labor efficiency variance is:

(Standard hours allowed – Actual hours worked) x Standard labor rate

A positive labor efficiency variance means fewer actual hours were used than standard hours. This is considered favorable because it means your labor was used more efficiently.

A negative labor efficiency variance means more actual hours were used than the standard This is unfavorable because it indicates inefficiencies in the labor process

Some common reasons for an unfavorable labor efficiency variance include:

- Inexperienced or insufficiently trained workers

- Defective materials resulting in rework

- Equipment downtime

- Poor process layout or workflow

What is Labor Price Variance?

Labor price variance specifically measures the difference between the standard rate you budgeted to pay workers versus the actual rate paid. It focuses entirely on the variable of pay rate – evaluating if labor cost aligned with expectations.

The formula to calculate labor price variance is:

(Standard rate – Actual rate paid) x Actual hours worked

A positive labor price variance means the actual rate paid was lower than the standard rate. This is considered favorable because it means you paid less for labor than originally budgeted.

A negative labor price variance means the actual rate paid was higher than the standard. This is unfavorable because it indicates labor expenses exceeded your budget.

Some common reasons for an unfavorable labor price variance include:

- Unexpected overtime or shift differentials

- Use of contract labor at a higher billable rate

- Across-the-board pay increases

Comparing Labor Efficiency vs. Labor Price Variance

While both labor efficiency and labor price variances provide insights into labor costs, it is important to analyze them in tandem to get the full picture. Here are some examples of how the variances may interact:

-

Favorable efficiency, favorable price: This is the ideal scenario, indicating labor costs are being well-controlled through both efficient use of time and closely managed pay rates.

-

Favorable efficiency, unfavorable price: This may occur if workers are incentivized with overtime pay to be more productive. The extra hours generate efficiencies but come at a higher hourly cost.

-

Unfavorable efficiency, favorable price: Operational issues may be undermining productivity, but labor rates stayed low due to use of junior or lower-cost workers.

-

Unfavorable efficiency, unfavorable price: Problems with both labor productivity and cost control. Requires urgent attention to address root causes.

By considering both variances together, you can better pinpoint where the opportunities for improvement lie – whether in process flow, worker training, incentive structures, or budget management.

Steps for Calculating and Analyzing Labor Variances

Now that we’ve covered the what and why of labor variances, let’s discuss the how. Follow these steps to effectively calculate and derive insights from your labor variance analysis:

-

Gather data: Collect actual labor hours worked and rates paid for the period, as well as your standard hours and rates from budgets.

-

Calculate variances: Plug the data into the formulas above to determine the labor efficiency and labor price variances.

-

Compare actual vs. standard: Side-by-side comparisons of actuals vs. standards often provide initial clues on variance drivers.

-

Consider contextual factors: Look at influencing factors like new hires, operational changes, incentive programs etc. that may explain the variances.

-

Identify root causes: Dig deeper into the reasons behind major discrepancies between actuals and standards.

-

Develop recommendations: Based on your findings, provide suggested actions to improve performance going forward.

-

Track over time: Calculate variances each period to monitor labor cost control and operational effectiveness.

-

Refine standards: As needed, update standards to ensure they reflect current conditions.

Best Practices for Managing Labor Variances

To leverage labor variances for ongoing labor cost control, keep these best practices in mind:

-

Set realistic standards based on historical data, benchmarks, and operational plans. Avoid overly loose or tight standards that render variances meaningless.

-

Timely calculation and analysis of variances, while the period is still fresh. Don’t let them sit until they are too late to address.

-

Design reports highlighting only significant or unusual variances to filter out noise. Focus attention on material issues.

-

Share key variance analyses across departments to improve collaboration. Production insights inform HR on training needs, for example.

-

Incorporate follow-up on variance-driven actions into management routines like daily production meetings.

-

Use flex budgets that update standards to reflect changing conditions versus static budgets that quickly become outdated.

Key Takeaways on Labor Variances

Having a solid grasp of labor efficiency variance vs labor price variance helps unlock one of the most valuable tools for monitoring and managing direct labor costs. Key takeaways include:

-

Labor efficiency variance evaluates productivity in hours used vs. standard. Labor price variance evaluates cost management through actual pay rates.

-

Analyze the variances together to get a complete picture of labor cost performance.

-

Identify root causes and improvement opportunities – don’t look at variances in isolation.

-

Variances are more insightful when realistic standards are set and consistently tracked over time.

-

Timely calculation, sharing of analysis, and follow-through are critical to drive continuous improvement.

Approached strategically, labor variances can reveal volumes about the effectiveness of both production and HR practices. Mastering their use will provide ongoing visibility into labor cost management and empower data-driven decision making.

Labor Price Variance Calculation

Labor price variance equals the standard hourly rate you pay direct labor employees minus the actual hourly rate you pay them, times the actual hours they work during a certain period.

For example, assume your small business budgets a standard labor rate of $20 per hour and pays your employees an actual rate of $18 per hour. Also, assume your employees work 400 actual hours during the month. Your labor price variance would be $20 minus $18, times 400, which equals a favorable $800.

Direct Labor Usage Variance

A labor variance that is a positive number is favorable and can result in profit that is higher than expected. A favorable variance occurs when your actual direct labor costs are less than your standard, or budgeted, costs, reports Accounting Coach.

A labor variance that is a negative number , on the other hand, is unfavorable and can result in profit that is lower than expected. An unfavorable variance occurs when actual direct labor costs are more than standard costs.

Price variance vs efficiency variance

What is the difference between labor efficiency variance and labor cost variance?

The direct labor quantity standard is usually referred to as labor efficiency variance while the price standard is referred to as labor rate variance. Labor cost variance = (Standard hours for actual output x Standard rate) – (Actual hours x Actual rate)

How much is a favorable labor efficiency variance?

Your labor efficiency variance would be 410 minus 400, times $20, which equals a favorable $200. Accountants perform standard costing by comparing expected costs with actual costs and analyzing the differences. Knowing the direct labor cost per unit makes pricing and margin management much easier.

What is labor price variance?

Labor price variance is a direct measurement of the actual cost of company labor. For example, if the company pays its employees a standard rate of $15 per hour but budgets for $20 per hour, the labor price variance shows how much variance there is between projected and actual labor costs for a specific number of hours the employees work.

What is direct labor efficiency variance?

The difference between actual time incurred to manufacture a certain number of units and the time allowed by standards to manufacture that number of units multiplied by standard direct labor rate is called direct labor efficiency variance or direct labor quantity variance.