Accrued interest can seem complicated at first, but it’s an essential concept for any business dealing with loans, bonds, or credit. Learning how to accurately record accrued interest is key for properly managing your books and financial statements. In this comprehensive guide, we’ll explain what accrued interest is, how to calculate it, and walk through examples of recording journal entries as both a borrower and lender.

What is Accrued Interest?

Accrued interest refers to the interest that accumulates on a loan or other financial obligation over a period of time It represents the interest that has been earned but not yet paid as of a certain date.

For example, if you have a loan with 5% annual interest, that interest accrues each day the loan remains unpaid. The accrued interest gradually builds up over time

Even though the interest hasn’t been paid yet, it still needs to be recorded in your books when it is incurred. This is done through an accrual journal entry.

Accrued interest applies to:

- Loans

- Mortgages

- Credit cards

- Bonds payable

- Any other debt obligation

Now let’s look at how to calculate accrued interest and record the journal entries.

Calculating Accrued Interest

To find the accrued interest amount, you need to know:

- The interest rate (stated as a decimal – e.g. 5% = 0.05)

- The time period the interest covers

- The principal amount of the loan or debt

Then you can use this formula:

Accrued Interest = (Interest Rate x Time Period in Days) / 365 x Principal Amount

Let’s see an example:

- Principal Amount: $10,000

- Interest Rate: 6%

- Time Period: 25 days

Accrued Interest = (0.06 x 25) / 365 x $10,000

= $41.10

So the accrued interest after 25 days on a $10,000 loan at 6% is $41.10.

This is the amount that would need to be recorded in your accounting books.

Recording Accrued Interest as a Borrower

If you’ve taken out a loan or have any debts, you need to record accrued interest as an expense. This increases your interest expense account and accrued interest payable account.

The journal entry would be:

Debit: Interest Expense

Credit: Accrued Interest Payable

For the above example, the journal entry would be:

| Date | Account | Debit | Credit |

|---|---|---|---|

| 6/30/22 | Interest Expense | $41.10 | |

| 6/30/22 | Accrued Interest Payable | $41.10 |

This properly records the accrued interest expense for the period and the corresponding payable amount now owed.

Accrued interest payable is a current liability, since the amount is usually paid within a year. The interest expense hits the income statement, reducing net income.

Recording Accrued Interest as a Lender

If you have loaned money to someone and are earning interest income, you need to record the accrued interest as revenue. This increases your accrued interest receivable account and interest revenue account.

The journal entry would be:

Debit: Accrued Interest Receivable

Credit: Interest Revenue

Using the same example above, if you were the lender you would make this entry:

| Date | Account | Debit | Credit |

|---|---|---|---|

| 6/30/22 | Accrued Interest Receivable | $41.10 | |

| 6/30/22 | Interest Revenue | $41.10 |

This records the amount of interest owed to you that is still outstanding. The corresponding interest revenue increases your total revenues for the period.

Accrued interest receivable is considered a current asset, since the amount is typically collected within 12 months.

Why Recording Accrued Interest Matters

Properly recording accrued interest is important for several reasons:

-

It adheres to the matching principle in accounting, where revenues and expenses are recorded in the same period they are incurred regardless of payment timing.

-

It captures the full economic activity during a period, not just cash transactions. This presents a more accurate picture of profitability.

-

It impacts the balance sheet, representing liabilities and assets accurately.

-

It affects key financial ratios related to solvency, liquidity, and profit margins.

-

It ensures interest expenses and revenues are fully reflected on the income statement.

-

It improves forecasting, as past accruals indicate patterns for future interest obligations.

Timing of Accrued Interest Entries

Accrued interest is typically recorded at the end of each accounting period, such as each month or quarter. This periodic entry captures the interest that accumulated over the preceding period.

However, organizations can record accrued interest more frequently, such as daily or weekly, depending on their specific accounting needs. More frequent entries provide greater precision in allocating interest expenses or revenues to narrower time periods.

Accrued interest can also be recorded at the time a loan or debt is initially issued. This initial entry records the interest owed from the issue date to the end of the current accounting period.

For example, if a loan was taken out on March 19 and the accounting period ends on March 31, the initial accrued interest entry would cover March 19 to March 31.

Accrued Interest vs. Cash Basis Accounting

Recording accrued interest follows the accrual basis of accounting. This differs from cash basis accounting, where income and expenses are recognized only when cash is received or paid out.

With the cash basis, interest expenses and revenues would not be recorded until the actual interest payment occurs. This violates the matching principle and potentially distorts financial statements.

Overall, accrual accounting and recording accrued interest provides a more accurate representation of a business’s true financial health and activities over time.

Accrued Interest Accounting Tips

Here are some tips and best practices to help you master accrued interest accounting:

-

Ensure your accounting system includes accounts for accruing interest expenses and revenues. Common account names are Accrued Interest Receivable, Accrued Interest Payable, Interest Revenue, and Interest Expense.

-

Review loan agreements and debt contracts to identify interest rates and payment schedules. This data feeds into your accrual calculations.

-

Automate accrued interest calculation and journal entries where possible. This saves time and minimizes manual errors.

-

Record interest accruals regularly at month end or quarter end. Don’t let interest build up unrecorded for too long.

-

Reconcile accrued interest accounts to underlying loan balances and payments. The amounts should align.

-

Document accrual calculations and entries clearly. This documents proper procedures are followed.

-

Consult an accounting professional if you need help. Accrued interest accounting can get complex with multiple loans or variable interest rates.

The Importance of Accurate Recordkeeping

As you can see, properly recording accrued interest requires careful attention to detail. Interest expenses and revenues can significantly impact the income statement and balance sheet.

Following the steps outlined here will ensure your books stay compliant with accounting standards and provide the most precise view of your company’s financial situation. Consult with an accounting professional if you need guidance in this area.

Proper accrued interest accounting isn’t overly complicated once you understand the fundamentals. Taking a methodical approach will put your business on solid financial footing. Accurate books translate directly into smarter business decisions and better bottom line results.

What Is Accrued Interest?

In accounting, accrued interest refers to the amount of interest that has been incurred, as of a specific date, on a loan or other financial obligation but has not yet been paid out. Accrued interest can either be in the form of accrued interest revenue, for the lender, or accrued interest expense, for the borrower.

The term accrued interest also refers to the amount of bond interest that has accumulated since the last time a bond interest payment was made.

- Accrued interest is a feature of accrual accounting, and it follows the guidelines of the revenue recognition and matching principles of accounting.

- Accrued interest is booked at the end of an accounting period as an adjusting journal entry, which reverses the first day of the following period.

- The amount of accrued interest to be recorded is the accumulated interest that has yet to be paid as of the end date of an accounting period.

:max_bytes(150000):strip_icc()/accured-interest-fa7c00af884947a7a32cd1daa57c3462.jpg)

Accrual Accounting and Accrued Interest

Accrued interest is a result of accrual accounting, which requires that accounting transactions be recognized and recorded when they occur, regardless of whether payment has been received or expended at that time. The ultimate goal when accruing interest is to ensure that the transaction is accurately recorded in the right period. Accrual accounting differs from cash accounting, which recognizes an event when cash or other forms of consideration trade hands.

The revenue recognition principle and matching principle are both important aspects of accrual accounting, and both are relevant in the concept of accrued interest. The revenue recognition principle states that revenue should be recognized in the period in which it was earned, rather than when payment is received. The matching principle states that expenses should be recorded in the same accounting period as the related revenues.

To illustrate how these principles impact accrued interest, consider a business that takes out a loan to purchase a company vehicle. The company owes the bank interest on the vehicle on the first day of the following month. The company has use of the vehicle for the entire prior month, and is, therefore, able to use the vehicle to conduct business and generate revenue.

At the end of each month, the business will need to record interest that it expects to pay out on the following day. In addition, the bank will be recording accrued interest income for the same one-month period because it anticipates the borrower will be paying it the following day.

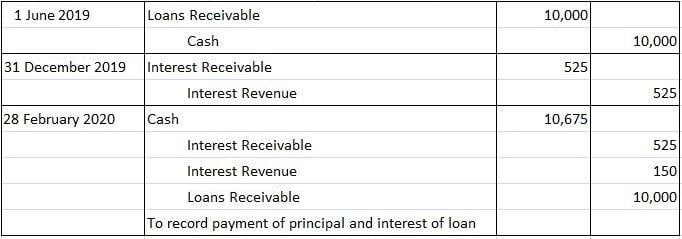

Adjusting Entry Example: Accrued Interest Expense

FAQ

What is the journal entry for accrued interest?

How is accrued interest treated in accounting?

What is the journal entry for accrual?

How do you record accrued accounts?