Tangible assets are physical assets that have monetary value and can be quantified. For companies, proper classification and valuation of tangible assets provides key insights into the total asset base and is critical for accurate financial reporting.

This guide explains what constitutes a tangible asset the most common classification methods and best practices for categorizing tangible assets on the balance sheet.

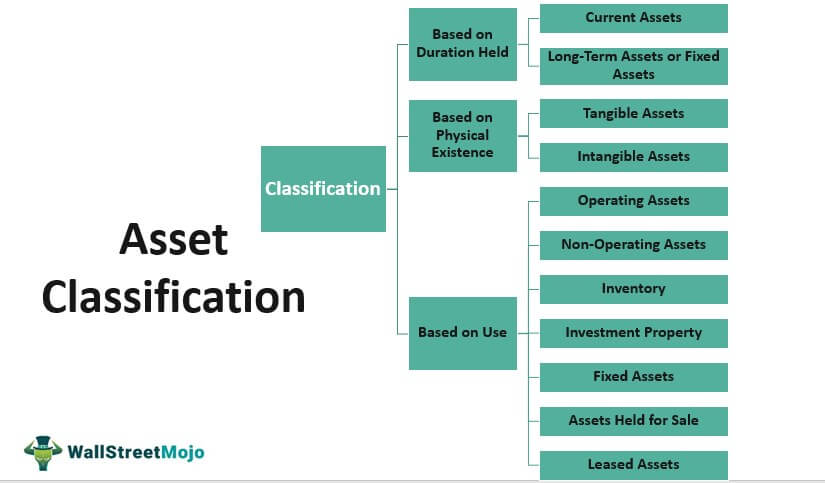

What are Tangible Assets?

Tangible assets are company-owned fixed assets with a physical form and presence. Some key examples include:

- Land

- Buildings and real estate

- Machinery and equipment

- Furniture and fixtures

- Vehicles

- Inventory

- Computer hardware

To qualify as a tangible asset an item must

- Have a physical substance and mass

- Be used in company operations to generate revenue

- Provide future economic benefits like production capabilities or marketability

- Be legally owned or controlled by the company

- Have a useful lifespan of over one year (not be a consumable)

Tangible assets are the opposite of intangible assets like patents, trademarks, copyrights, and brand recognition, which lack physical substance.

Why Proper Classification Matters

Categorizing tangible assets appropriately serves several important purposes:

- It organizes assets logically on the balance sheet for financial reporting.

- It enables calculation of accurate depreciation expenses.

- It provides insights into how asset investments align with company strategy.

- It determines the potential resale or salvage value of assets if liquidated.

- It impacts valuation ratios like return on assets that assess management effectiveness.

Without proper classification, assets may be improperly valued or depreciated, leading to financial misstatements.

Overview of Classification Methods

There are three primary methods companies use to classify tangible assets:

1. Appraisal Method

In the appraisal method, an independent appraiser assesses the fair market value of tangible assets based on what they could be sold for.

Appraisals account for factors like:

- Asset condition – Whether used or unused, working or damaged

- Comparable sales – What similar assets have sold for

- Replacement costs – How much it would cost to replace the asset

Appraisals require professional judgment, so this method is more complex and costly. But it provides the most accurate approximation of realizable value.

2. Liquidation Method

The liquidation method classifies assets based on their net cash value if liquidated or scrapped today.

It calculates:

Liquidation value = Resale proceeds – Costs to sell the asset

Resale proceeds represent what the used asset could be sold for in a fire sale. Costs include transportation, auction fees, removal expenses, broker commissions, and legal fees.

Since liquidation assumes forcibly selling assets well below cost, this method minimizes asset value. It is primarily used for bankruptcy proceedings.

3. Replacement Cost Method

In the replacement cost method, assets are valued at what it would cost to replace them with a similar new asset serving the same function.

Factors considered include:

- New purchase price based on current market rates

- Delivery and installation costs

- Import duties and sales taxes

- Other direct costs to bring the asset into usage

This method is easier to implement than appraisal but does not account for depreciation of used assets.

Best Practices for Classifying Tangible Assets

When categorizing tangible assets, here are some key guidelines to follow:

-

Group assets consistently – Classify assets the same way from year to year within your asset hierarchy. Follow accounting conventions for your industry.

-

Segment assets by function – Classify assets based on their purpose within business operations, such as manufacturing equipment, office furniture, computer hardware, etc.

-

Separate capitalized and expensed items – Capitalized assets should be reported distinctly from small supply items that are expensed immediately.

-

List individually material items – Major assets that are individually significant to operations should be itemized rather than grouped together.

-

Note restrictions – Identify assets encumbered by liens, pledges as collateral, or legal contracts restricting sale.

-

Track holding purpose – Distinguish assets held for productive use from those held for investment or resale.

-

Disclose physical location – Note the physical location of tangible assets, especially for multinational companies across different regions.

-

Record fully depreciated assets – Continue to list tangible assets that are fully depreciated but still in use. Identify their depreciated status.

-

Show construction in progress – List assets not yet placed into service separately as construction in progress rather than treating as completed assets.

Presentation on the Balance Sheet

On the company balance sheet, tangible assets are included under non-current assets segmented into sub-categories.

Typical classifications include:

- Property, Plant, and Equipment

- Land

- Buildings

- Manufacturing Equipment

- Office Furniture

- Leasehold Improvements

- Accumulated Depreciation

- Natural Resource Assets

- Mineral and Timber Resources

- Investment Property

- Intangible Assets

- Patents

- Trademarks

- Licenses

- Goodwill

Within each classification, assets are normally listed in order of liquidity starting with those easiest to liquidate like accounts receivable.

Illiquid assets like land are listed last. Declining asset balances like accumulated depreciation are shown as negative amounts.

Tangible Asset Valuation Methods

Once classified, tangible assets must be assigned a monetary value on the balance sheet reflecting their fair value. Common valuation approaches include:

-

Historical cost – Assets are valued at original purchase or construction cost less accumulated depreciation.

-

Reproduction cost – Assets are valued at what it would cost to reproduce an identical new asset.

-

Replacement cost – Assets are valued at the cost to replace with a new asset serving the same function.

-

Liquidation value – Assets are valued at the net proceeds that would be realized if the asset was sold today.

-

Market comparison – Assets are valued based on the sale price of comparable asset sales.

Historical cost valuation is most common since it is verifiable. Other methods may be used for impairment testing or insurance valuation.

Accurately classifying and valuing tangible assets according to accounting standards and financial reporting regulations is crucial for providing investors, regulators, and management with a reliable perspective on a company’s asset base and valuation.

With a logical classification system and consistent accounting treatment, companies can manage their tangible assets effectively and optimize utilization to drive operations and growth.

Types of Assets: Financial, Tangible, and Intangible

What are tangible assets?

Tangible assets are assets with a physical form and that hold value. Examples include property, plant, and equipment. Tangible assets are seen and felt and can be destroyed by fire, natural disaster, or an accident.

How do you classify tangible assets?

They may also use their assets as collateral, which is when a business uses the asset as security for the repayment of a loan. Classifying tangible assets is the process of documenting and categorizing them in order to have a record of each asset’s value. Here’s a list of steps to help you classify tangible assets correctly: 1.

What is the difference between tangible assets and intangible assets?

Tangible assets, also called fixed assets, are physical items like vehicles, cash, inventory, plants, and equipment that contribute to a company’s overall value. Intangible assets, such as patents, copyrights, and goodwill, lack physical form but still hold value, contrasting with tangible assets.

Why should you classify tangible and intangible assets correctly?

As you can see, tangible and intangible assets have different characteristics and implications for accounting. By classifying your assets correctly, you can simplify your accounting and provide more accurate and relevant information to your stakeholders. 3. Depreciation Methods for Asset Classification