Calculating cash flow from financing activities is an important part of analyzing a company’s financial health. As an investor or analyst, you want to know where a company’s cash is coming from and how it is being used. Cash flow from financing activities shows the flow of cash between a company and its owners and creditors.

In this comprehensive guide, I will explain what cash flow from financing activities is, what types of activities it includes, how to calculate it, and how to analyze it to gain insights into a company.

What is Cash Flow from Financing Activities?

Cash flow from financing activities is one of the three sections of the cash flow statement, the other two being cash flow from operating activities and cash flow from investing activities

The cash flow statement shows how cash has moved in and out of a business during a specific period of time. It breaks down the sources and uses of a company’s cash and is a key indicator of financial health.

Specifically, cash flow from financing activities measures the flow of cash between a company and its owners and creditors. It shows where a company gets funding from and how that funding is used.

Common financing activities include:

- Issuing or paying off debt

- Issuing or repurchasing stock

- Paying dividends to shareholders

- Making principal payments on loans

- Making interest payments on debt

Positive cash flow means more money is coming into the company from financing activities. Negative cash flow means more money is being paid out.

Analyzing cash flow from financing can give insight into how dependent a company is on external funding and how sustainable its capital structure is It is an important metric for assessing liquidity risk

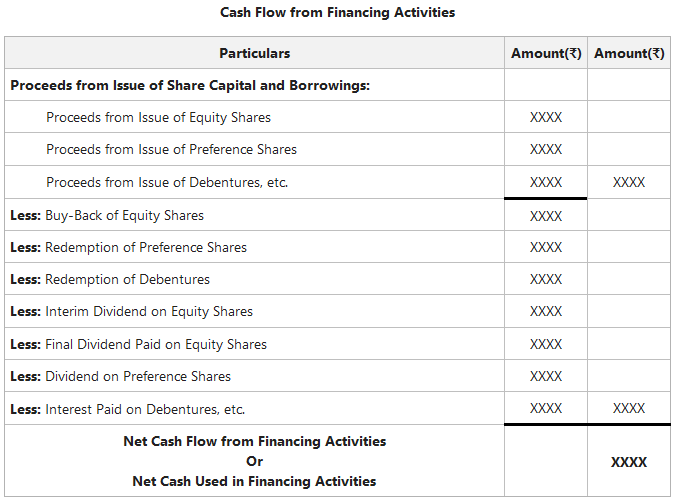

What to Include in Cash Flow from Financing Activities

When calculating cash flow from financing activities, include all cash inflows and outflows related to a company’s capital structure and dividend policy.

Cash Inflows

- Issuing common stock

- Issuing preferred stock

- Issuing bonds payable

- Taking out new loans or increasing existing loan balances

- Receiving payments on notes receivable from shareholders

Cash Outflows

- Repurchasing common or preferred shares

- Repaying bonds at maturity

- Making principal repayments on loans

- Paying dividends on common or preferred stock

- Making interest payments on debt

- Paying loan origination fees

How to Calculate Cash Flow from Financing Activities

Cash flow from financing activities can be calculated using two methods:

1. Direct Method

The direct method lists all major cash inflows and outflows from financing activities.

Cash flow from financing activities = Net cash inflows – Net cash outflows

For example:

- Issued $5 million in bonds: +$5,000,000

- Repaid $2 million in loans: -$2,000,000

- Paid $1 million in dividends: -$1,000,000

- Net cash from financing activities: +$2,000,000

This method provides more detail on specific financing activities but takes more effort to calculate.

2. Indirect Method

The indirect method starts with the beginning and ending debt and equity accounts on the balance sheet and makes adjustments for non-cash items to arrive at the cash flow amount.

Cash flow from financing activities = (Current period debt and equity) – (Previous period debt and equity) – Non-cash items

For example:

- Ending long-term debt balance: $15,000,000

- Beginning long-term debt balance: $10,000,000

- Change in long-term debt: +$5,000,000

- Non-cash items like unamortized discounts: -$500,000

- Cash flow from long-term debt activities: +$4,500,000

The indirect method is easier to calculate but provides less detail. Companies use a mix of both methods when preparing official cash flow statements.

How to Analyze Cash Flow from Financing Activities

When you calculate cash flow from financing activities, you also need to analyze and interpret the results to gain insights into the company. Here are some key things to look for:

-

Trends – Is cash flow from financing activities increasing or decreasing over time? What could be driving this?

-

Dependency – Is the company relying heavily on external financing to fund growth? This may indicate risk.

-

Debt levels – Is the company taking on more debt or paying debt down? Watch for signs of excess leverage.

-

Stock issuance – Is the company issuing a lot of new stock to raise cash? This could dilute existing shareholders.

-

Dividends – Is the dividend payout growing faster than operating cash flows? This may be unsustainable long-term.

-

Comparison to peers – How does the company’s cash flow from financing compare to competitors?

Analyzing financing cash flow trends, debt levels, stock issuance, dividends and peer comparisons can provide early warning signs of risk or insights into how financially stable a company is over time.

Real World Examples

Let’s look at real cash flow from financing activities examples from Amazon and Coca-Cola Company to see these principles in action.

Amazon’s Cash Flow from Financing Activities

Below is the cash flow from financing section from Amazon’s statements for the year ended December 31, 2021:

| Amazon’s Cash Flow from Financing Activities | |

|---|---|

| Proceeds from long-term debt and other | $5,337 million |

| Repayments of long-term debt and other | ($4,908 million) |

| Principal repayments of finance leases | ($3,347 million) |

| Principal repayments of financing obligations | ($56 million) |

| Net proceeds from short-term debt | ($1,544 million) |

| Proceeds from issuance of common stock | $3 million |

| Repurchase of common stock | ($6,458 million) |

| Other | ($224 million) |

| Net cash used for financing activities | ($11,197 million) |

- Key things to note:

- Amazon primarily used cash for repayments of long-term debt and repurchases of common stock

- Cash outflows exceeded inflows, resulting in negative net cash from financing

- Heavy use of debt repayments and stock buybacks may indicate a focus on reducing leverage on the balance sheet

Coca-Cola Company’s Cash Flow from Financing Activities

Below is Coca-Cola’s cash flow from financing activities for the year ended December 31, 2021:

| Coca-Cola’s Cash Flow from Financing Activities | |

|---|---|

| Proceeds from issuance of debt | $18,457 million |

| Payments on debt | ($11,401 million) |

| Proceeds from exercise of stock options | $1,091 million |

| Purchases of stock for treasury | ($438 million) |

| Dividends | ($7,190 million) |

| Other financing activities | ($863 million) |

| Net cash provided by financing activities | $656 million |

- Key things to note:

- Coca-Cola had a net inflow from financing activities

- Issuances of debt provided a large cash inflow

- Dividends were the largest single cash outflow

- The company is still accessing debt markets to raise capital

Analyzing real examples like these provides insights into the capital structure, debt levels, and dividend policies of each company. We can see how financing activities impact the overall cash position.

Limitations of Cash Flow from Financing Activities

While analyzing financing cash flow is useful, there are some limitations to consider:

- It provides less insight into operating performance than other financial metrics

- The indirect method can smooth over fluctuations compared to the direct method

- It doesn’t account for future commitments like interest or principal payments

- It doesn’t reflect balance sheet changes from non-cash activities

Cash flow from financing activities should be assessed in conjunction with other metrics to get a full picture of financial health. It has limitations on its own but provides a valuable piece of the puzzle.

Being able to accurately calculate and analyze cash flow from financing activities is an important skill for investors, creditors, and analysts evaluating company performance. It provides insights into capital structure, funding sources, dividend policies, and liquidity risk.

Remember to include all cash inflows and outflows from debt, equity, dividends, and interest. Compare trends over time and to industry peers. Assess along with other metrics for a complete view.

Mastering financing cash flow analysis takes time, but will provide you with valuable information on a company’s financial strength and sustainability in the long run.

Cash Flow from Financing Activities Formula

The formula for calculating the cash from financing section is as follows:

Note that the parentheses signify that the item is an outflow of cash (i.e. a negative number).

By contrast, debt and equity issuances are shown as positive inflows of cash, since the company is raising capital (i.e. cash proceeds).

- Debt Issuances → Cash Inflow

- Equity Issuance → Cash Inflow

- Share Buybacks → Cash Outflow

- Debt Repayment → Cash Outflow

- Dividends → Cash Outflow

Cash Flow from Financing: Common Line Items

| Cash from Financing | Definition |

|---|---|

| Debt Issuances |

|

| Equity Issuances |

|

| Share Buybacks |

|

| Debt Repayment |

|

| Dividends |

|

How to Compute Cash flows from Financing Activities

What is the cash flow from financing activities formula?

The cash flow from financing activities formula is the sum of all cash inflows and outflows. This includes stock repurchases, dividend payments, debt issuance, and debt repayment. In this formula, cash outflows are negative numbers and are represented within parentheses.

How do you calculate cash flow from financing?

Cash Flow from Financing = Debt Issuances + Equity Issuances + (Share Buybacks) + (Debt Repayment) + (Dividends) Note that the parentheses signify that the item is an outflow of cash (i.e. a negative number). By contrast, debt and equity issuances are shown as positive inflows of cash, since the company is raising capital (i.e. cash proceeds).

What is included in cash flow from financing activities?

Finance activities include the issuance and repayment of equity, payment of dividends, issuance and repayment of debt, and capital lease obligations. Companies that require capital will raise money by issuing debt or equity, and this will be reflected in the cash flow statement. What’s Included in Cash Flow from Financing Activities?

What is cash flow from financing activities (CFF)?

Cash Flow from Financing Activities (CFF): The net cash impact of raising capital from equity/debt issuances, net of cash used for share buybacks, and debt repayments — with the outflow from the payout of dividends to shareholders also taken into account. The formula for calculating the cash from financing section is as follows: