Accumulated depreciation is an important metric that reduces the book value of assets to account for wear and tear over time. But how exactly do you calculate accumulated depreciation?

In this comprehensive guide, we’ll walk through the meaning of accumulated depreciation, the step-by-step calculation, and how to analyze and use this metric to understand the real net value of your assets.

What is Accumulated Depreciation?

Depreciation expenses allocate the cost of an asset over its useful life. This represents the wear and tear, aging, and obsolescence of the asset.

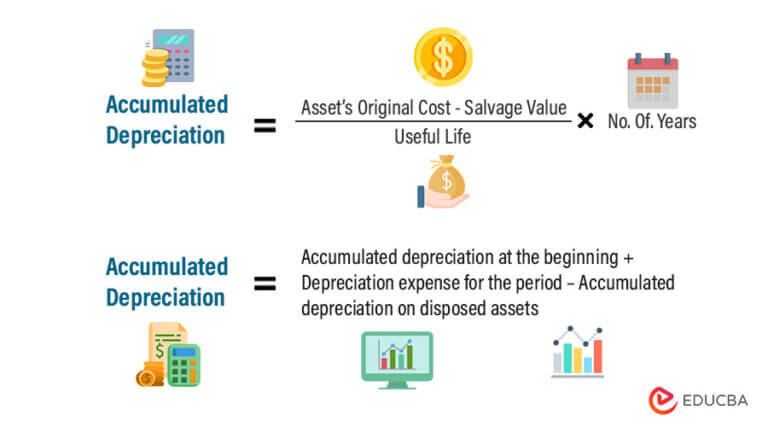

Accumulated depreciation is the total amount of depreciation expense charged against an asset up to a single point in time. The accumulated depreciation balance does not close at year end. Instead, it accumulates over the life of the fixed asset.

For example, a company purchases equipment for $150,000. The expected useful life is 10 years and the salvage value is zero. The annual depreciation expense is $15,000 ($150,000 / 10 years). At the end of year 1, accumulated depreciation is $15,000. At the end of year 2, it is $30,000 ($15,000 x 2 years).

The formula is:

Accumulated Depreciation = Prior Years' Depreciation + Current Year DepreciationSo this running total reflects the cumulative depreciation amounts recorded to date on an asset.

Next we’ll go through the step-by-step process to calculate accumulated depreciation.

How to Calculate Accumulated Depreciation

Follow these key steps to calculate accumulated depreciation for an asset:

Step 1: Determine Depreciation Expense for the Period

To find the depreciation expense for the current period:

- Take the asset cost

- Subtract the salvage value

- Divide this by the useful life in years

This gives you the depreciation expense to record for each period.

For example:

Asset Cost = $150,000Salvage Value = $0Useful Life = 10 yearsAnnual Depreciation = ($150,000 - $0) / 10 years = $15,000So depreciation expense for each year is $15,000.

Step 2: Calculate Total Prior Years’ Depreciation

To determine accumulated depreciation, you first need the total depreciation from prior years.

- For year 1, prior depreciation is $0.

- For year 2, prior depreciation is the depreciation from year 1 = $15,000

- For year 3, it’s the depreciation from years 1 and 2 = $15,000 + $15,000 = $30,000

So accumulate the depreciation expense for all prior years.

Step 3: Add Current Year Depreciation

Take the depreciation expense for the current year. For example, in year 4 this would be $15,000.

Add this to the total prior years’ depreciation.

In year 4:

Prior years' depreciation = $30,000 Current year depreciation = $15,000Accumulated Depreciation = $30,000 + $15,000 = $45,000This gives you the accumulated depreciation up until the current period.

Step 4: Subtract Accumulated Depreciation from Asset Cost

On the balance sheet, accumulated depreciation is shown as a contra account, reducing the book value of the asset.

So you subtract accumulated depreciation from the asset account:

Asset Cost = $150,000Accumulated Depreciation = $45,000 Net Asset Value = $150,000 - $45,000 = $105,000This net asset value more accurately reflects the remaining useful life of the asset.

And that’s the 4 step process for calculating accumulated depreciation! Now let’s look at how to analyze and use this important metric.

How to Analyze and Use Accumulated Depreciation

Understanding your accumulated depreciation balance provides key insights:

-

Value assets accurately – Subtracting accumulated depreciation from your fixed assets shows their net realizable value.

-

Assess useful life – A high accumulated depreciation balance can indicate an asset is near the end of its useful life.

-

Plan capital expenditures – Knowing net book values helps determine when assets need replacement.

-

Determine sales value – Accumulated depreciation provides a Minimum Selling Price for assets you want to dispose.

-

Manage taxes – Depreciation reduces taxable income so tracking accumulated depreciation is important.

-

Compare assets – Accumulated depreciation ratios (depreciation/cost) show which assets lose value fastest.

Monitoring your accumulated depreciation ensures your financial statements reflect assets at their true value. It also provides key insights into capital planning and lifecycle management.

Key Takeaways on Accumulated Depreciation

-

Accumulated depreciation is the total depreciation recorded on an asset up to a single point in time.

-

It is calculated by adding the current period’s depreciation expense to the prior periods’ accumulated depreciation.

-

This contra account is subtracted from the asset account to reflect its net book value.

-

Analyzing accumulated depreciation ratios helps manage assets and plan capital expenditures.

-

Tracking accumulated depreciation provides a more accurate view of asset values on the balance sheet.

Understanding accumulated depreciation is vital for both financial reporting and effective asset management. Follow the calculation steps outlined to determine accumulated depreciation for your fixed assets. This will provide insights into capital planning and help report assets accurately on financial statements.

Accumulated depreciation

Is accumulated depreciation an asset or liability?

Deprecation can provide certain tax benefits to help offset taxable income generated from investments. Accumulated depreciation is also useful in this sense. But determining whether accumulated depreciation is an asset or liability requires some explanation. Let’s first review depreciation.

Is accumulated depreciation a debit or credit?

While depreciation expense is a debit (increase in expense) shown in the income statement, accumulated depreciation is usually the offsetting credit (contra-asset reduction in balance sheet). Why is it mandatory that depreciation expense be included in the P and L?

What is cost less accumulated depreciation?

Cost c. Cost less accumulated depreciation and accumulated impairment losses d. Cost less accumulated depreciation These are biological assets that have attained harvestable specifications (for consumable biological assets) or are able to sustain regular harvests (for bearer biological assets).