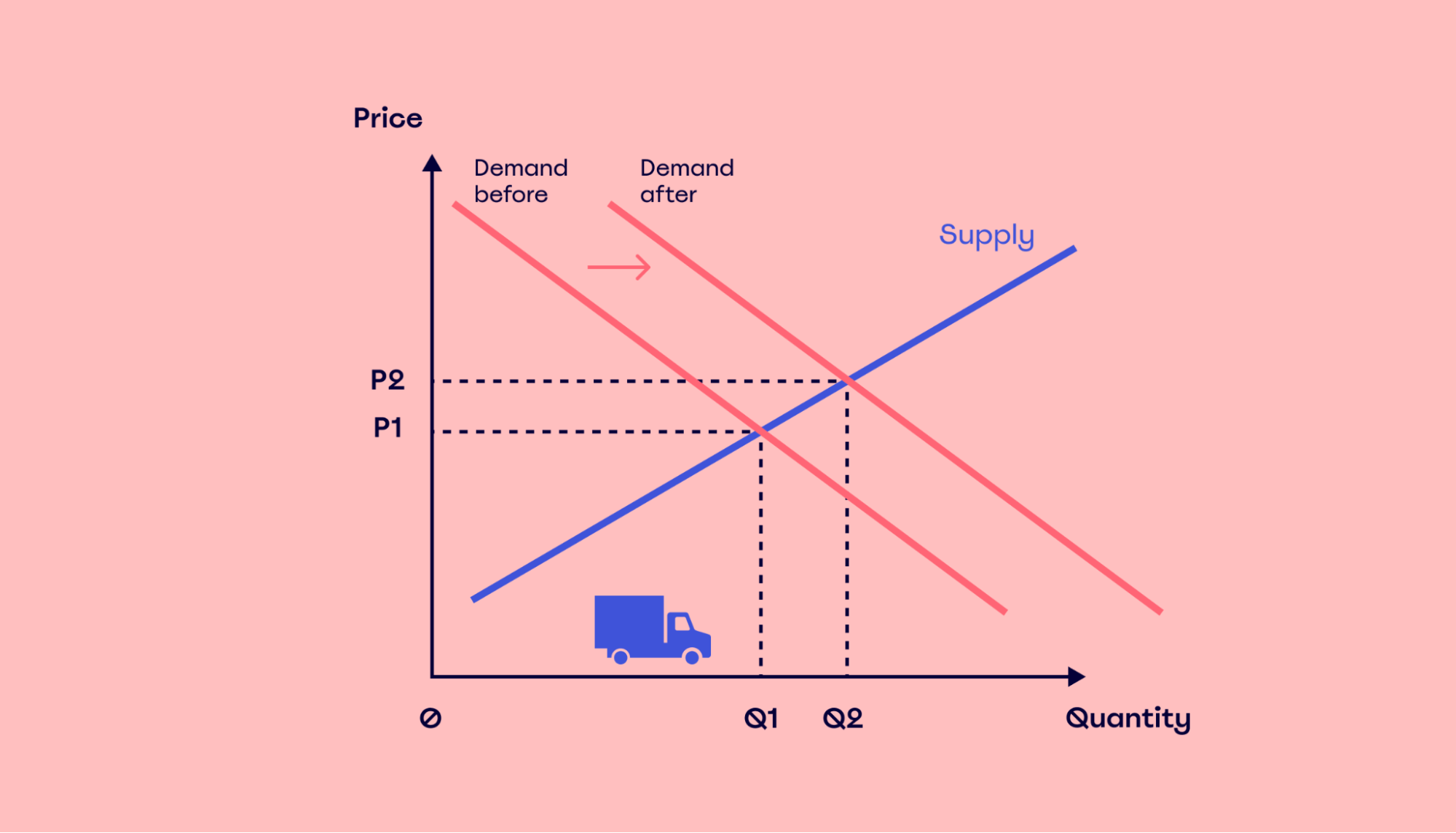

The simplest model of a market involves two things: supply and demand. The price and quantity of the goods sold in the market are a function of both. When a natural disaster hits, the immediate effect can be two-fold. In such situations, it’s not unusual that the demand for certain products may increase. For example, if everyone is trying to leave an area, the demand for gas may rise.

The other effect is that supply for certain products may decrease. For example, it may be more costly to transport gas in areas affected by a natural disaster, thus reducing the supply of gas and, in turn, increasing the price.

The law of supply and demand is one of the most fundamental concepts in economics. It explains the relationship between the supply of a product or service and the demand for that product or service, and how this relationship affects prices. As a blogger trying to explain complex economic topics in simple terms I think it’s important to have a solid understanding of supply demand, and how they determine prices.

A Quick Recap of Supply and Demand

First, let’s do a quick recap of the key principles of supply and demand

-

The law of supply states that as the price of a product increases, suppliers will be willing and able to supply more of that product. As the price falls, suppliers will reduce the quantity they supply.

-

The law of demand says that as the price of a product falls, buyers will demand a higher quantity. As the price rises, demand will fall.

-

Equilibrium price is the market clearing price where supply equals demand. At this price, the exact quantity producers wish to supply is perfectly balanced with the quantity buyers wish to consume.

-

Surpluses occur when the quantity supplied exceeds the quantity demanded at the current price. This will cause downward pressure on prices.

-

Shortages happen when demand exceeds supply at the current price. This causes upward pressure on prices.

How Price Changes Impact Supply and Demand

Now let’s dig deeper into how changes in price impact supply and demand.

When the price of a product rises, it typically reduces demand while simultaneously encouraging additional supply. Let’s walk through an example:

-

Imagine the equilibrium price for baseball hats is $20. At this price, suppliers produce 10,000 hats per month and consumers purchase 10,000 hats. Supply equals demand.

-

If the price increased to $25 per hat, here’s what would happen:

-

Consumers would demand fewer hats due to the higher price. Let’s say demand would fall to 8,000 hats per month.

-

The higher price would incentivize suppliers to produce more hats. So let’s say supply would rise to 12,000 hats per month.

-

-

At the new $25 price, supply exceeds demand. There is a surplus of hats on the market.

-

This surplus will cause downward pressure on prices. Suppliers will be willing to accept lower prices to sell their excess inventory. The price will fall back towards the equilibrium level.

The opposite happens when the price decreases. Lower prices encourage demand while simultaneously discouraging supply. This shortage causes upward pressure on prices.

So in essence, changes in price act as signals that incentivize producers and consumers to rebalance supply and demand at the new price level. This is the “invisible hand” of the free market in action.

Factors Influencing Price Elasticity

However, it’s important to understand that supply and demand don’t always respond proportionally to price changes. Some products experience greater changes in quantity supplied or quantity demanded in response to price shifts than others.

For example, a 10% rise in the price of a new iPhone model may only reduce demand by 5%. Meanwhile, a 10% increase in the price of generic cough medicine may result in a 15% drop in demand.

Economists use the term “price elasticity” to describe this sensitivity to price changes. Products where changes in price have a strong influence on demand are said to be price elastic. Products where demand is not significantly altered by price shifts are inelastic.

What factors determine the price elasticity of supply and demand? Here are some of the key factors:

-

Availability of substitutes – Products with many close substitutes tend to be elastic because consumers can easily switch when prices rise. Unique products with few direct substitutes tend to be inelastic.

-

Necessity vs. luxury – Necessities like food and medicine tend to be inelastic since consumers will continue buying them even when prices are high. Luxury goods and services are more elastic because consumers can live without them if needed.

-

Time horizon – Demand tends to be more inelastic in the short run and more elastic over time. Consumers need time to research alternatives and change behaviors when prices rise.

-

Share of income – Goods that make up a large share of a consumer’s budget tend to be price inelastic. When the price rises significantly, it forces them to keep buying. Minor expenses tend to be elastic.

-

Price range – For low-priced items, changes in price have less impact on demand, so they tend to be inelastic. Luxury goods with high prices tend to have more elastic demand.

These factors interact to determine how much demand and supply respond to a change in price, influencing the strength of the impact on the equilibrium price and quantity.

Real-World Examples

To make this more concrete, let’s look at some real-world examples of how supply, demand, and price elasticity influence pricing:

-

Gasoline: Gas prices can spike during supply disruptions. But because most drivers have few alternatives to fueling their cars, demand is inelastic and quantities sold decline only modestly. Drivers absorb the higher prices.

-

Concert tickets: Tickets for popular bands are typically inelastic because of scarcity and lack of substitutes. So even when prices skyrocket on resale markets, dedicated fans will pay.

-

Airline tickets: Coach seats are often elastic because leisure travelers can book other carriers or destinations. But business travelers are often less sensitive to pricing since they need to go to specific destinations.

-

Agricultural products: Flooding and drought impact crop yields, causing swings in supply. But food is an inelastic necessity, so reduced supply sharply increases prices.

These examples demonstrate that the sensitivity of supply and demand to price shifts has a major influence on real-world pricing. Factors like product uniqueness, timeliness, and consumer budget share determine this sensitivity.

How Supply and Demand Shape Pricing

In conclusion, the fundamental law of supply and demand is crucial for understanding how market prices are determined in free markets. As consumers and producers respond to price signals, the equilibrium price and quantity will adapt to balance the market.

However, the degree to which supply and demand respond to these price shifts depends on price elasticity. Products where quantity is highly sensitive to price will see greater fluctuations as supply and demand rebalance. More inelastic goods may see less dramatic swings in response to the same supply or demand shocks.

So when you are analyzing prices for a product, think carefully about the market conditions impacting supply and demand as well as the likely price elasticity for that item. With a strong grasp of these economic concepts, you can better anticipate and explain the pricing dynamics at work.

What’s the Difference Between Price Gouging and Inflation?

While price gouging is often the result of a business decision, inflation is directly impacted by the market.

Inflation is a general increase in prices caused by economic factors like demand, costs, and money supply over time. For this reason, inflation can be identified as an overall increase in prices throughout an economy over time, while price gouging is localized and opportunistic.

Another notable difference is that inflation is a natural occurrence, while price gouging is known for negatively impacting consumers and communities, often during crises or when consumers have no choice but to purchase a product.

How Does Supply and Demand Work?

The concept of supply and demand is used to explain how price is influenced by the supply of goods and services available and the consumer demand for those products.

Broken down, supply is the amount of goods available and demand is the customers’ willingness to pay for the good or service.

In the online course Economics for Managers, Harvard Business School Professor Bharat Anand explains demand in terms of customer willingness to pay.

“Demand curves can move over time because willingness to pay moves over time—even for the same product,” Anand says.

Willingness to pay is influenced by countless factors, including:

- Income

- Geography

- Weather

- Age

- Gender

- Brand loyalty

- Service levels

- Advertising

- Competing products

- Expectations

- Legality

- Packaging

- Environmental or social impact

- Necessity

In instances when the demand for a good or service suddenly increases, it’s natural to assume the price of the product will rise. But what about the price of essential items during a time of crisis? In these cases, most customers are willing to pay any price to obtain the needed item. But does the booming demand always justify the increased rates? When costs rise to unfair levels due to a lack of supply or boost in demand, it’s often referred to as “price gouging.”

Supply and Demand Explained in One Minute

Why does demand increase as prices fall?

Demand increases as prices fall. On the supply side, the law posits that producers supply more of a resource, product, or commodity as prices rise. Supply falls as prices fall. The price at which demand matches supply is the equilibrium, the point at which the market clears.

How does the law of supply and demand affect prices?

The law of supply and demand is an economic theory that explains how supply and demand are related to each other and how that relationship affects the price of goods and services. It’s a fundamental economic principle that explains when supply exceeds demand for a good or service, prices fall.

What is supply and demand in economics?

supply and demand, in economics, relationship between the quantity of a commodity that producers wish to sell at various prices and the quantity that consumers wish to buy. It is the main model of price determination used in economic theory. The price of a commodity is determined by the interaction of supply and demand in a market.

What happens if demand increases or decreases?

An increase in demand, all other things unchanged, will cause the equilibrium price to rise; quantity supplied will increase. A decrease in demand will cause the equilibrium price to fall; quantity supplied will decrease. An increase in supply, all other things unchanged, will cause the equilibrium price to fall; quantity demanded will increase.