Variable costing is an accounting method that focuses on the cost of producing goods or services and can be used to create a more accurate income statement. This method is particularly useful for businesses that produce multiple items, as it can provide more insight into the actual cost of the items produced. Variable costing income statements provide a complete picture of the costs associated with producing a product or service, providing helpful information when making decisions about pricing and production. In this blog post, we will discuss the definition of a variable costing income statement and provide an example to illustrate its usefulness. We will also discuss the advantages and disadvantages of using this type of statement. Understanding the concept of a variable costing income statement can be a great way to help businesses make informed decisions about pricing and production.

Variable Costing (the Variable Costing method in Managerial Accounting)

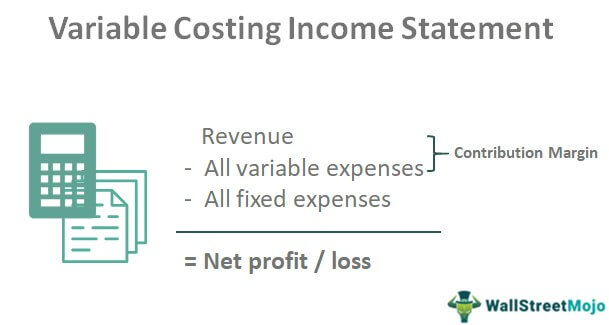

What is a Variable Costing Income Statement?

The contribution margin will frequently be significantly higher than the gross margin in many businesses because so much of their production costs are fixed, while only a small portion of their selling and administrative costs are variable.

The formula for Net profit or loss is:-

This can be utilized by you on your website, in templates, etc. , Would you kindly provide us with a hyperlink for the article’s attribution? For example: Source: Variable Costing Income Statement (wallstreetmojo com).

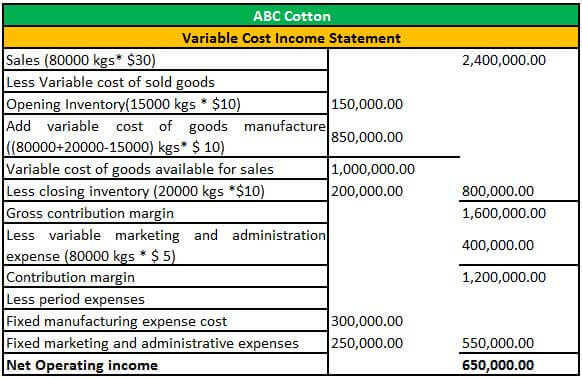

Examples of Variable Costing Income Statement

Cotton is sold by ABC Cotton for $30 per kilogram. The data for the year 2016 is given below:-.

We have created a variable cost income statement using the data above.

Let us understand how this statement is prepared.

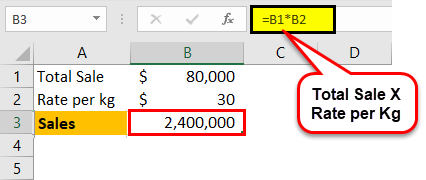

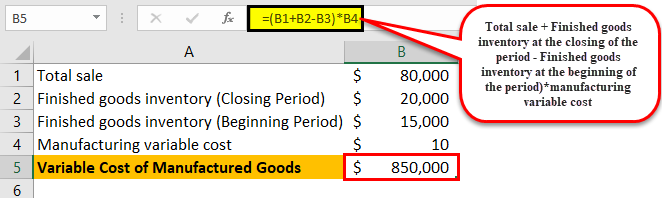

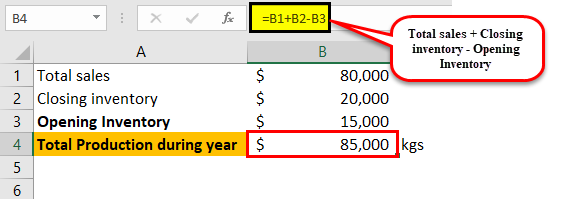

Sales are computed as a total sale in kilograms, i e. , 80000 multiplied by per kg cost, i. e. , $30.

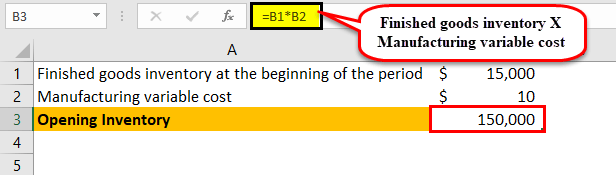

Calculate variable Opening Inventory

Opening Inventory is the stock of finished goods at the start of the period, i e. , 15000 kgs multiplied by manufacturing variable cost, i. e. , $ 10. So,.

= finished goods inventory at the start of the period* variable manufacturing costs

The variable cost of manufactured goods is

Manufacturing variable cost = (Total sale + Finished Goods Inventory at the Closing of the Period – Finished Goods Inventory at the Beginning of the Period)

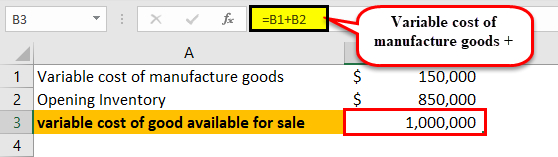

=Variable cost of manufacturing goods + Opening Inventory

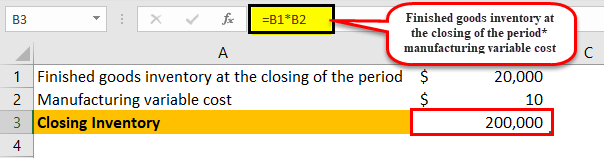

Calculate the closing inventory that is

Manufacturing variable costs =Finished goods inventory at period’s end

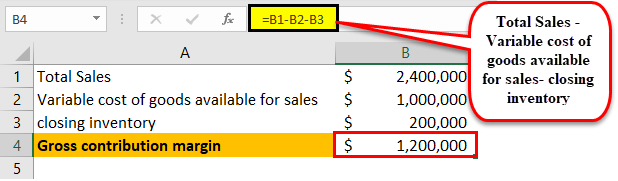

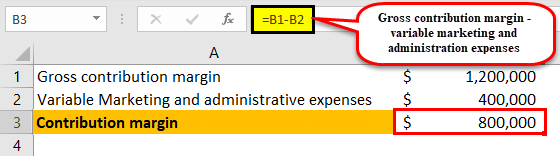

Now, we will get the Gross contribution margin.

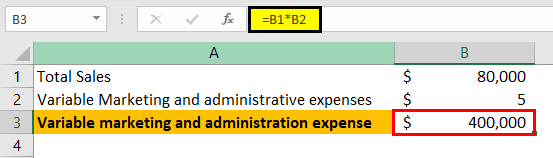

Calculate variable marketing and administration expenses, which is

=Total sale*Variable Marketing and administrative expenses

Contribution margin calculated i.e.

=Gross contribution margin – variable marketing and administration expenses

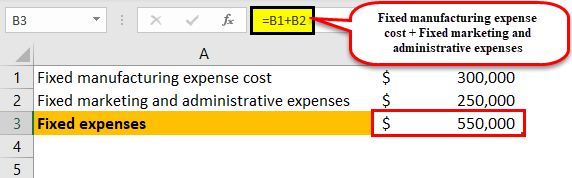

Now, we have to calculate fixed expenses

= Fixed marketing and administrative costs plus Fixed manufacturing expense cost

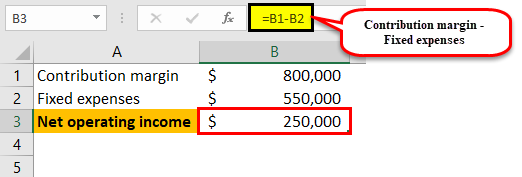

Finally, we will get net operating income

= Contribution margin – Fixed expenses

Total production over the course of the year equals total sales plus closing inventory less opening inventory

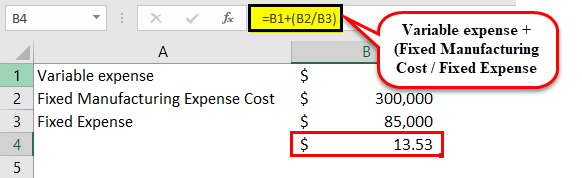

Manufacturing expenses per unit=Variable expense + Fixed Expense

Variable Costing vs. Absorption Costing

Under variable costing, the following costs go into the product:

Under absorption costing, the following costs go into the product:

For your reference, the diagram below offers a breakdown of which expenses are included in variable costing vs absorption costing methods:

Keep in mind that while period costs are expenses incurred during the period, product costs are costs that go into the product.

IFC is a manufacturer of phone cases. The company’s income statement for its most recent year end (2018) is excerpted below:

IFC does not report an opening inventory. The business produced 1,000,000 phone cases in 2018 and reported total manufacturing costs of $598,000 (roughly $0). 60 per phone case).

A recent special order for 1,000,000 phone cases costing $400,000 was placed with the manufacturer. The manager is hesitant to accept this special order despite having ample capacity because it is less than the cost of $598,000 to produce the initial 1,000,000 phone cases as stated in the company’s income statement. The manager wants you to decide whether the business should accept this order as the company’s cost accountant.

For starters, it’s crucial to understand that the $598,000 in manufacturing costs for 1,000,000 phone cases covers fixed expenses like insurance, equipment, building maintenance, and utilities. Therefore, in order to decide whether to accept this special order, we should use variable costing.

Variable costing:

Total = $305,000 / 1,000,000 units produced = $0. 305 variable cost per case.

1,000,000 phone cases on special order will cost nothing to produce. 305 x 1,000,000 = $305,000. As a result, the contribution margin is $400,000 – $305,000, which equals $95,000.

The special order ought to be approved in light of our variable costing method. The special order will increase the company’s profits by $95,000.

Understanding the manager’s reluctance to accept the order is critical. The decision-maker made a mistake by including fixed costs in the cost calculation. Given sufficient capacity, the business won’t have to incur additional fixed costs to fulfill the special order for one million. As you can see, variable costing is crucial for making decisions.

A business that had previously been successful could ultimately be destroyed by a downward spiral of product discontinuation decisions. This example highlights the fact that a good manager will not rely solely on data from absorption costing. The decision-making process must be guided by variable costing techniques that identify product contribution margins (as more fully explained in the following paragraphs).

With variable costing, the contribution margin is calculated by deducting all variable costs from sales. Nepal’s presentation divides variable costs into two categories. The variable manufacturing costs (direct materials, direct labor, and variable manufacturing overhead) are all included in the variable product costs. To arrive at the variable manufacturing margin, these expenses are deducted from sales. Some of Nepal’s SG&A costs also vary with sales. As a result, in order to determine the true contribution margin, these amounts must also be deducted. When making crucial decisions, management must consider all variable costs (whether connected to manufacturing or SG&A). For instance, Nepal may pay sales commissions based on sales; it would be incorrect to ignore those from consideration when determining the “margin” that is to be generated from a specific transaction or event. Fixed factory overhead and fixed SG&A costs are deducted from the contribution margin.

In order to avoid making the wrong decisions about product discontinuation, variable costing data is very helpful. Many businesses offer multiple products. Typically, some will be more profitable than others, and it may be a wise business move to concentrate on the top-performing units while ceasing to offer others. Assume that a company offers products A, B, and C. Each is being produced in an equal amount, and the business can fully meet customer demand with its current capacity (i e. , producing more will not increase sales). Regarding its marketing, general, and administrative activities, the company is not experiencing any variable costs.

Based on absorption costing methods, the additional unit appears to produce a loss of $0.50, and it appears that the correct decision is to not make the sale. Variable costing suggests a profit of $0.50, and the information appears to support a decision to make the sale. Management may well decide to sell the additional unit at $9.50 and produce an additional $0.50 for the bottom line. Remember, no other costs will be generated by accepting this proposed transaction. If management was limited to absorption costing information, this opportunity would likely have been foregone.

Based on absorption costing methods, the additional unit appears to produce a loss of $0.50, and it appears that the correct decision is to not make the sale. Variable costing suggests a profit of $0.50, and the information appears to support a decision to make the sale. Management may well decide to sell the additional unit at $9.50 and produce an additional $0.50 for the bottom line. Remember, no other costs will be generated by accepting this proposed transaction. If management was limited to absorption costing information, this opportunity would likely have been foregone.

Nepal does not maintain inventory, so the income under absorption and variable costing is equal. The difference is only in the manner of presentation. Study the arrows carefully to see how the amounts from the absorption costing approach would be repositioned in the income statement for the variable costing method. This may seem like a lot of trouble to make over nothing since the outcome is the same for both approaches. Although decision logic is frequently influenced by consideration of contribution effects, keep in mind that “gross profit” is not the same as “contribution margin.” Additionally, the periodic income will vary between the two methods as inventory levels change.

FAQ

What is variable costing example?

Examples of variable costs include raw material and packaging costs for manufacturing companies, as well as credit card transaction fees and shipping costs for retail businesses, which fluctuate with sales. A variable cost can be contrasted with a fixed cost.

Which type of income statement is used for variable costing?

A variable costing income statement is one in which all variable expenses are subtracted from revenue to produce a separately-stated contribution margin, which is then subtracted from all fixed expenses to produce the period’s net profit or loss.

Which is the best example of a variable expense?

Your monthly rent or mortgage are examples of fixed expenses that largely remain constant. Variable costs include those that fluctuate or are unforeseen, such as restaurant bills or auto maintenance