Creating a film budget is an integral part of the production process. Without a budget, you canât bring your vision to life. But with so many elements to consider and so many variations of the budget needed throughout the production process, putting one together can be daunting.

In this article, Ill explain the basics of budgeting, including what a film budget entails, and some simple tips that you can follow to get your budget started.

A production budget is an essential tool for manufacturers to plan and control their production costs and inventory. But what exactly goes into creating an accurate production budget? In this article, we’ll provide a detailed overview of the key components of a production budget, including beginning inventory, sales forecasts, production capacity, and more.

Why Create a Production Budget?

Before jumping into what’s included, it’s helpful to understand why a production budget is necessary in the first place Here are some of the main benefits

-

Matches production to expected sales demand – A production budget ensures you don’t over or under produce based on sales forecasts This avoids excess inventory costs or lost sales from stockouts.

-

Optimizes use of production capacity – By planning production levels, you can fully utilize machines, labor, and materials without exceeding limits

-

Controls costs – With detailed cost estimates, you can keep labor, materials, and overhead costs within budget.

-

Guides purchasing and scheduling – The budget provides plans for raw material purchases and production scheduling.

-

Aids in managing cash flow – Knowing expected production costs and timing helps manage cash flow requirements.

Key Components of a Production Budget

Now let’s look at the key inputs that go into creating a comprehensive production budget:

1. Time Horizon

The first step is deciding the timeframe or budget period. Common periods are monthly, quarterly, or annually. The duration depends on factors like:

-

Product characteristics – How long does it take to manufacture a single unit? Products with short run times can use shorter budgets.

-

Demand patterns – Is demand seasonal or steady? Seasonal demand may require monthly or quarterly budgets.

-

Capacity – Larger manufacturers may need annual or quarterly budgets to plan capacity.

Selecting the appropriate timeframe provides the necessary level of detail without creating excessive work.

2. Beginning Inventory

The beginning inventory is the current stock of finished goods at the start of the budget period. This includes units completed but not yet sold. The beginning inventory establishes the base stock available to sell before new production.

Tracking beginning inventory by product and managing it carefully is crucial for an accurate budget. Too much inventory ties up cash while too little can lead to stockouts and lost sales. Beginning inventory directly offsets the required production quantities.

3. Sales Forecast

The sales forecast estimates consumer demand and target sales by product over the budget period. This drives the production requirements. Creating an accurate forecast requires analyzing past sales trends, seasonality, market conditions, and sales pipelines.

Most manufacturers forecast at the SKU level to match production to demand for each specific product. Advanced forecasting techniques include moving averages, exponential smoothing, and regression analysis. Overestimating the forecast leads to excess inventory while underestimating causes stockouts.

4. Ending Inventory Target

While beginning inventory is the current stock, the ending inventory is the desired stock at the end of the budget period. This is also called the target finish goods inventory. Maintaining a sufficient ending inventory acts as a buffer against stockouts from forecast errors or demand spikes.

Companies typically set ending inventory targets based on factors like lead times, seasonality, sales volatility, and customer service levels. For example, products with long lead times or seasonal sales spikes need higher inventory cushions.

5. Production Capacity

Producing the budgeted quantities requires adequate capacity. The budget should consider available hours based on number of shifts and days per week. This gets compared to machine hours required for the product mix. Any capacity bottlenecks must get identified and addressed.

Capacity analysis involves calculation of workstation cycle times and throughput rates. Capacity may necessitate overtime, additional shifts, or productivity improvements to achieve the budget. Updated capacity planning helps avoid unrealistic production assumptions.

6. Production Costs

The three main categories of production costs that get budgeted are:

-

Direct material costs – Costs of raw materials used in production, based on quantities needed and purchase prices.

-

Direct labor costs – Wages and benefits for production workers to manufacture the products.

-

Manufacturing overhead – Indirect production costs like utilities, equipment maintenance, and supervision.

Detailed line item budgets for each cost provide visibility for monitoring spending versus the approved budget. Identifying costs by cost center also enables tracking costs by production area.

7. Production Plan

The culminating production budget summarizes the key outputs:

- Number of units to produce by product

- Material purchases by item and quantity

- Labor hours and staffing levels by production line and shift

- Machine hours needed on key equipment

- Manufacturing cost estimates by department

The completed budget provides a detailed plan to guide raw material procurement, capacity scheduling, inventory management, and cost control.

8. Master Budget Integration

While used for production planning, the production budget also gets integrated into the company’s overall master budget. The master budget includes other components like the sales budget, material purchases budget, and cash budget.

The production budget links to the sales budget for finished goods. It provides production costs and capacity utilization for the financial budgets. This enables aligning production plans with financial objectives.

Developing the Production Budget

Now that we’ve covered the key components, let’s look at the process for developing the production budget:

-

Determine the budget period – Select the appropriate monthly, quarterly, or annual timeframe.

-

Identify products – List out all products and SKUs to be included in the budget.

-

Forecast sales – Develop sales forecasts by product for the budget period.

-

Set ending inventory targets – Determine desired finish goods inventory by product.

-

Identify beginning inventory – Record current finish goods inventory levels.

-

Analyze production capacity – Evaluate workforce size, shifts, and machine capacity.

-

Calculate production quantities – Apply the budget formula to determine units to produce by product while considering beginning inventory, sales forecasts and ending inventory targets.

-

Estimate costs – Develop detailed estimates of material, labor, and overhead costs.

-

Prepare production plan – Document the production plans, material requirements, scheduling, and costs.

-

Incorporate into master budget – Integrate production budget data into the overall financial plan.

By following this step-by-step process, manufacturers create a comprehensive, accurate production budget.

Production Budget Example

Let’s look at a simple example to illustrate how to calculate production quantities based on the key inputs.

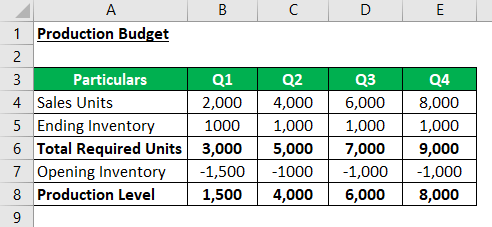

Acme Manufacturing produces gizmos. The beginning inventory is 1,000 units. Acme forecasts sales of 10,000 units for the coming quarter. It wants to end the quarter with 2,000 units of ending inventory as a buffer.

- Beginning inventory: 1,000 units

- Forecast sales: 10,000 units

- Ending inventory target: 2,000 units

Using the formula:

Required production = Forecast sales + Ending inventory – Beginning inventory

Then Acme’s required production for the quarter is:

10,000 units + 2,000 units – 1,000 units = 11,000 units

This example shows how the core budget elements come together to determine the quantities to produce. The budget accounts for existing stock, expected demand, and desired ending inventory. Extending this analysis across all products and resources creates a detailed picture for guiding production.

Key Takeaways

- A production budget is vital for aligning production with sales demand and controlling costs.

- Primary inputs include beginning inventory, sales forecasts, ending inventory targets, capacity, and costs.

- The budget determines the quantity to produce by product while optimizing capacity and inventory.

- Detailed estimates provide plans for procurement, scheduling, staffing, and cost management.

- The integrated budget connects sales, production, and financial planning.

Accurately budgeting production is crucial for any manufacturing operation. Careful planning of inventory, capacity, and costs ensures production aligns with company sales and financial objectives. Following the steps outlined here will help put your company on the path towards production success!

Why do you need a budget for your film?

The budget is one of the foundational documents of any production, alongside the script and the shooting schedule.

Put simply, the budget details all the projected costs of making a film, including talent and crew, equipment, location, wardrobe, construction, transportation and post-production expenses, to name a few.

The first iteration of your budget will likely play a key role in securing funding from investors, who will want to see a general outline of your costs. When details are more secure and funding is in place, youâll need a comprehensive budget to prepare practically for your shoot. But its important to note that even when your project is underway, that detailed version of your budget will be an ever-evolving document that keeps your film on track financially.

Creating a workable budget

While a lot of the information will still be projected at this stage, itâs important to be as realistic as you can about what needs to happen in front of, and behind, the camera. How much material can be shot in a day? How many people will you realistically need?

Underestimating what you need or how long things will take at this stage will likely derail your project further down the line. But overestimating will potentially be off-putting for funders. The aim here is to strike a balance in order to create a workable, realistic budget.

Remember, potential investors will want to see how their investment money will be spent. Its is essential for you to anticipate and understand what your costs will be, and adequately plan for them.

WHAT TO INCLUDE IN A TV COMMERCIAL PRODUCTION BUDGET TEMPLATE

What should a production budget include?

Creating a production budget can be valuable for a company’s financial future, but it can involve a significant amount of research and preparation. If you work on a financial or management team, knowing what to include in a production budget can help you accurately predict the number of units to produce and avoid wasting labor and materials.

How is a production budget prepared?

The production budget is typically prepared based on sales forecasts and desired inventory levels. It takes into account the following key elements: Expected Sales: The sales forecast shows the anticipated volume of goods or services that the business anticipates selling over the allocated time period.

What is the difference between a sales budget and a production budget?

The sales budget is the foundation for the production budget, with adjustments for the starting and ending inventory. Production budgets, similar to sales budgets, are developed on a unit basis. A production budget depends on 3 factors: The production budget also depends on a company’s inventory policy.

How do manufacturing companies use production budgets?

Manufacturing companies use production budgets to specify the number of product units to be manufactured. The production budget is determined based on sales forecasts. It is adjusted based on the company’s inventory policy in terms of planned inventory levels.