A balance sheet provides a snapshot of a company’s financial position at a specific point in time It summarizes what a business owns and owes The balance sheet equation is

Assets = Liabilities + Equity

On the asset side, balance sheets list assets from most liquid to least liquid. Liquidity refers to how quickly an asset can be converted into cash.

Cash itself is considered the most liquid asset. Inventory and accounts receivable take time to monetize, so they are less liquid. Fixed assets like property and equipment are long-term illiquid assets.

Why does liquidity determine asset order on balance sheets? Because asset liquidity provides vital insights into the company’s financial health and flexibility

This article will explain:

- What comprises business assets

- Why liquidity dictates balance sheet order

- The standard asset classifications

- Examples of various asset types

Follow along for a comprehensive overview of the correct order of assets on a balance sheet and why it matters.

What Are Business Assets?

Assets represent economic resources that provide future value to a company. More specifically, business assets consist of:

-

Tangible assets – Physical property owned e.g. equipment, real estate, inventory, cash

-

Intangible assets – Non-physical assets e.g. trademarks, patents, copyrights, goodwill

-

Financial assets – Claims on debt or equity e.g. accounts receivable, bonds, stocks

All assets share common traits of being:

-

Owned – The company has legal rights to the asset

-

Valuable – It provides economic benefit now or in the future

-

Quantifiable – Its monetary value can be measured

If something does not meet all three criteria, it is not considered an asset. Understanding the breadth of potential assets provides context before we dive into balance sheet order.

Why Liquidity Determines Balance Sheet Order

On a balance sheet, assets are always listed in order of liquidity from high to low. This enables anyone reviewing the financials to immediately grasp which assets can readily be converted into cash if needed.

Liquidity refers to an asset’s nearness to cash form. The most liquid assets are already cash or can quickly become cash within a few days or weeks. Less liquid assets take longer to monetize – often months or years.

Liquidity is important because it provides flexibility. Highly liquid assets give a company options to pay debts, invest capital, or fund operations even with limited cash reserves.

Think of liquidity as a measure of how nimbly management can access value from its assets. Higher liquidity means greater agility and lower risk.

Overview of Asset Classifications

While the exact order differs slightly between various accounting standards, assets on a balance sheet always flow from most to least liquid. Here is an overview of the standard asset classifications:

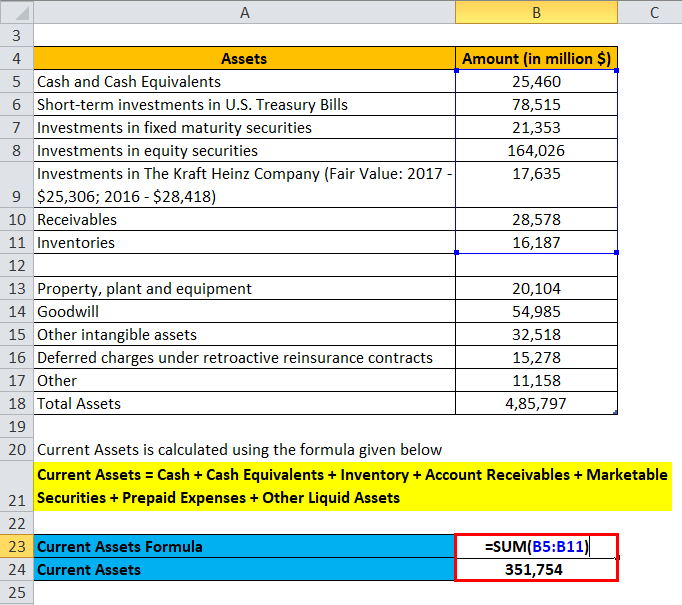

Current Assets

- Cash and cash equivalents

- Marketable securities

- Accounts receivable

- Inventory

- Prepaid expenses

Long-Term Investments

- Bonds

- Stocks

- Other securities

Property, Plant and Equipment (Fixed Assets)

- Land

- Buildings

- Machinery

- Equipment

- Furniture

Intangible Assets

- Goodwill

- Trademarks

- Patents

- Copyrights

Other Assets

- Long-term prepaid assets

Next, let’s look at examples of specific assets within each classification along with their relative liquidity.

Examples of Current Assets

Current assets are those reasonably expected to be realized in cash or consumed within one year. They are the most liquid asset class.

Cash and Cash Equivalents

This includes physical cash, funds in checking and savings accounts, as well as other instruments like money market holdings and short-term investments that can quickly become cash.

Cash is perfectly liquid by definition. The other current assets have varying degrees of liquidity but should materialize within 12 months.

Marketable Securities

These include stock and bond investments that can be readily traded on public exchanges. The liquidity depends on the type of security. Listed equities can often be sold in a few days. Government bonds may take a bit longer but still qualify as current assets in most cases.

Accounts Receivable

These are amounts owed to the company by customers for goods or services delivered on credit. Accounts receivable liquidity aligns with a company’s credit terms, which often range from 30-90 days.

Inventory

This includes raw materials, work-in-progress goods, and finished products owned by the company. Inventory liquidity varies based on how quickly products sell, but usually within 3-12 months.

Prepaid Expenses

Prepaid expenses represent amounts paid in advance for services not yet received, like insurance, advertising, or office supplies. Their liquidity period matches the underlying service term.

Overview of Long-Term Investments

Long-term investments include assets intended to be held for over a year, most commonly stocks and bonds. These take longer to monetize so they are considered less liquid than current assets.

Equity investments in non-subsidiary companies are accounted for by cost or fair market value depending on influence. Debt investments like bonds are reported at amortized cost or fair value.

Market conditions impact the liquidity. But these assets generally take weeks or months to divest, compared to current asset liquidity measured in days.

Examples of Fixed Assets

Also known as property, plant and equipment (PP&E), fixed assets represent the tangible physical infrastructure used to generate business results. This includes:

Land

Land purchased for facilities or future development. Difficult to convert directly to cash and has an indefinite useful life.

Buildings

Structures used for business operations like offices, production facilities, and warehouses. Fairly illiquid and depreciated over a useful life of 25-50 years.

Machinery and Equipment

Major equipment like manufacturing machines, production tools, vehicles, computers, furniture, etc. Depreciated over 2-20 years depending on the asset. Challenging to liquefy quickly.

Fixed assets require active attempts to sell, such as hiring a real estate broker or auctioneer, in order to convert to cash. This makes them far less liquid than current assets.

Overview of Intangible Assets

Intangible assets lack physical substance but provide long-term value to a company. Major categories include:

Goodwill

An premium paid over the fair value of acquired company assets during a merger or acquisition. It represents the value of brand recognition, loyal customers, etc. One of the most illiquid assets, as goodwill is only monetized when selling the entire business.

Trademarks

Exclusive rights to use a logo, brand name or other intellectual property. While trademarks themselves aren’t liquid, the exclusivity adds value to products/services which facilitates revenue.

Patents

A right to exclusively produce and sell an invention or process. Like trademarks, patents enhance business value more than having direct resale value.

Copyrights

Legal protections granted to original creative works like books, songs, films, software, etc. Copyrights can be sold or licensed but generally do not directly convert to cash.

Intangible assets help generate economic benefits but lack quick liquidity apart from selling the entire company. They have higher usefulness to the current owner versus potential buyers.

Other Assets and Special Cases

The “Other Assets” section on balance sheets functions as a catch-all for anything not fitting the major classifications. Examples include:

-

Long-term prepaid expenses – Prepaid amounts not expiring within 12 months, like a multi-year insurance policy.

-

Deferred tax assets – Credits from overpayment or operating losses than can be used to reduce future tax bills.

-

Promissory notes – Formal IOUs from borrowers promising repayment on a certain date.

-

Restricted cash – Cash set aside solely for specific legal or contractual purposes.

There are also some special cases worth noting:

-

Investments in subsidiaries – Majority-owned subsidiaries are included under Investments since their full assets are not consolidated.

-

Currency derivatives – Instruments used to hedge against currency exchange fluctuations. Can be current or long-term.

-

Deferred revenue – Payment received before goods/services are delivered. Although not technically an asset, it is sometimes included under Other Assets.

Why Proper Asset Order Matters

Adhering to the standard order of assets from most to least liquid provides consistency and clarity on financial statements. This enables efficient analysis and comparisons for internal and external stakeholders.

Audit standards prohibit arbitrary reordering of assets on balance sheets. Proper ordering must be followed to comply with GAAP and IFRS rules.

For companies, asset liquidity ranks among the most important financial health indicators. It gauges the ability to pay bills, seize opportunities, and withstand hard times. As the saying goes: “cash is king.”

Key Takeaways

- Assets are

Single Member LLC Asset Protection Myths (Charging Order Protection FACTS)

FAQ

In what order will you list assets?

Which is the correct order for the assets section?

What is the most appropriate order of current assets?

How are assets arranged?

What is the correct order of assets on a balance sheet?

On a balance sheet, the correct order of assets is from highest liquidity to lowest. Because cash assets convert easily, cash is first on the list. The least liquefied balance sheet assets are investments. The correct order of assets on a balance sheet is: What is the importance of liquidity?

What is the correct order to present current assets?

Companies frequently report income tax as the last item before net income on the income statement. Study with Quizlet and memorize flashcards containing terms like The correct order to present current assets is a. Cash, accounts receivable, prepaid items, inventories. Cash, accounts receivable, inventories, prepaid items. c.

Why should I list my company’s assets in the correct order?

Listing your company’s assets in the correct order can be important so you have an accurate balance sheet. Order of assets helps both companies and investors define asset liquidity, current liability coverage and financial stability.

Why is Order of assets important?

Order of assets helps both companies and investors define asset liquidity, current liability coverage and financial stability. Understanding the correct order of assets for your balance sheet can help you accurately report the financial status of your business.