As a business owner or accounting professional, you’ve likely encountered the term “charge off” when reviewing financial statements and accounts receivable aging reports. But what exactly does this accounting term mean and what are the implications? Let’s clear up the mystery around charge offs in accounting!

Charge Off Defined

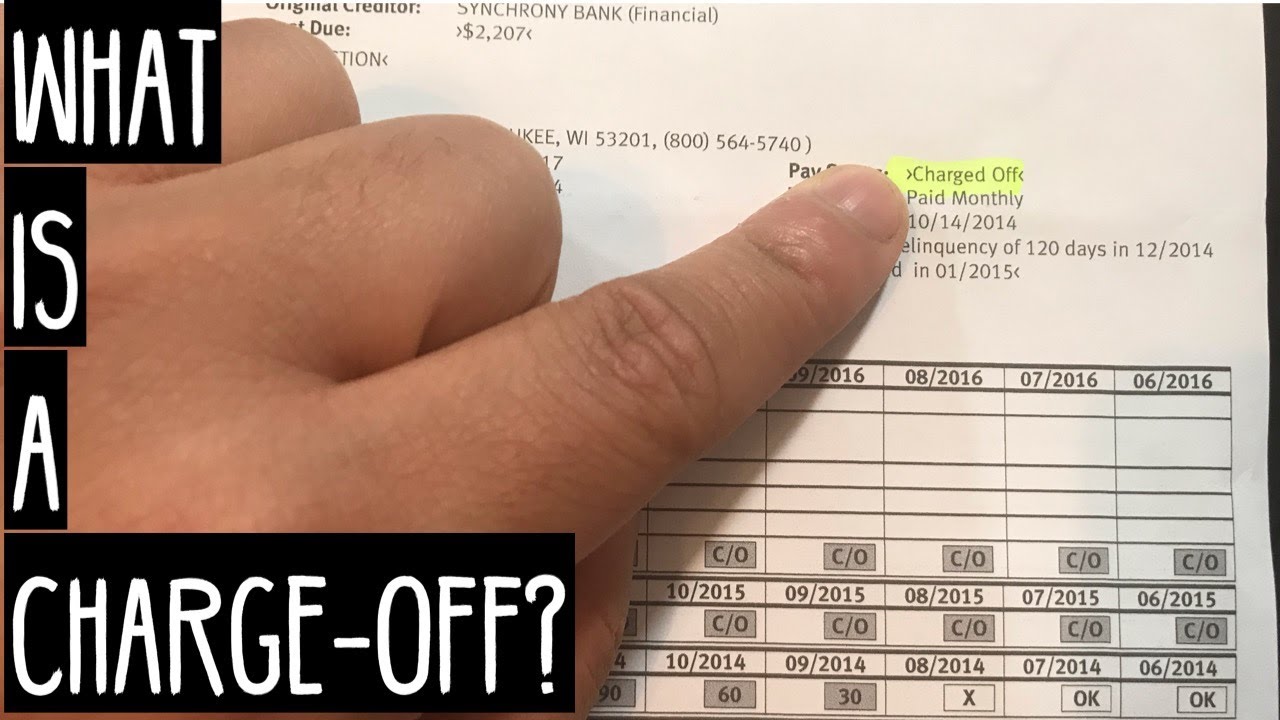

A charge off refers to a debt that is deemed uncollectible by a creditor or lender and written off as a loss on their financial books. It typically happens after many months of non-payment when the creditor has exhausted efforts to recover the debt.

Common examples include:

- Credit card debt past due for 180+ days

- Personal loans or auto loans delinquent for 6 months

- Utility bills overdue for several billing cycles

Even though the creditor charges off the debt, the borrower is still legally obligated to pay. A charge off is an accounting procedure for the lender – it does not absolve the underlying debt obligation.

When Are Debts Charged Off?

Charge off policies differ but often follow these general timelines:

- Credit card debt – charged off around 180 days past due

- Installment loans – charged off around 120-180 days delinquent

- Mortgages – charged off after 90-120 days in default

- Utility bills – charged off after 2-3 months of nonpayment

The creditor will attempt to collect during the delinquency period through calls, letters, late fees, sending accounts to collections, etc. Once efforts are exhausted and the account reaches the charge off stage, it is essentially “given up on” in accounting terms

Charge Off vs. Default

Charge off is often confused with default but they are distinct credit events

-

Charge off – an accounting procedure where the lender writes off the uncollectible account balance. The debt still legally exists.

-

Default – the debtor has breached the loan agreement by missing payments. Legal default occurs after 90+ days overdue.

An account is typically charged off after being in default for an extended period. Default may lead to charge off, but charge off does not require legal default.

How Charge Offs Work

When an account is severely delinquent, creditors follow these general steps:

- Classify account as non-performing asset (NPA) once payments are 30 days past due

- Report missed payments to credit bureaus, damaging borrower’s credit score

- After 90+ days past due, declare the account in default

- Around 120 to 180 days late, charge off the balance as uncollectible

- Take tax deduction for the bad debt charge off loss [explain briefly]

- Attempt to collect on the charged off amount using debt collectors

- Sell the charged off account to a debt buyer at a discount

- Charge off stays on credit report for 7 years

While no more internal recovery efforts are made after the charge off, external collectors will persist in trying to recover something. The charge off balance continues to legally owe until the borrower pays, settles, or files bankruptcy.

Tax Treatment of Charge Offs

Charge offs for unpaid business accounts receivable are deductible for tax purposes in the year the debt became worthless. Non-business bad debts are also deductible as short-term capital losses.

The tax rules include:

- Must properly document that reasonable collection efforts were made

- Business bad debts deductible in full

- Non-business bad debts deductible as short-term capital losses

- Debt must be truly worthless with minimal chance of future recovery

- Lender can take deduction or tax benefit from the loss

How Charge Offs Affect Credit & Future Lending

Unfortunately, charge offs severely damage your credit standing for many years:

- Charge offs drop credit scores by up to 150 points

- High volume of charge offs indicates financial irresponsibility

- Charge off status remains for 7 years on your credit report

- Future lenders will view you as very high risk

- Difficulty getting approved for loans or at favorable rates

- Accepted only for subprime loans with predatory terms

This credit damage makes it much more expensive to access financing in the future. Paying or settling charge offs won’t fully remove the negative history either. You’ll have to wait out the 7 years for the charge off to drop off your report.

Best Practices for Avoiding Charge Offs

As a lender, be proactive with delinquent accounts to prevent charge offs:

- Contact borrowers immediately upon missed payments

- Offer flexible repayment plans and loan modifications

- Work with borrowers facing financial hardship

- Consider partial debt forgiveness if necessary

- Allow borrowers to prioritize paying secured debt first

- Sell severely delinquent accounts to debt buyers promptly

As a borrower, take steps to avoid charge offs on your accounts:

- Pay at least the minimum due every month

- Contact lenders quickly if struggling to pay

- Prioritize paying secured debt like mortgages first

- Ask about hardship plans or payment reductions

- Seek credit counseling if overwhelmed by debt

- Build an emergency fund covering a few months expenses

Avoiding charge offs requires diligence from both lenders and borrowers. Acting early upon delinquencies is key.

Options After a Charge Off

If you have accounts that were charged off, here are some options to resolve them:

Pay in full – Ideally, pay off the charge off balance completely. This will change its status to “paid charge off.”

Settle for less – Offer a lump sum payment less than the full amount in exchange for the lender closing the account. Get this settlement agreement in writing.

Payment plan – Work out an affordable monthly payment schedule to eventually pay it off over time.

Bankruptcy – In severe cases with multiple charge offs, file for bankruptcy to discharge unaffordable debt under court protection.

Wait it out – After 7 years from the date of the initial delinquency, the charge off will drop off your credit report. The account balance will still legally owe.

Ideally, try to find a way to pay off charge offs or settle them on good terms. Leaving them unpaid hurts your credit and still leaves you legally exposed to collection efforts.

Protecting Your Rights

Keep the following rights in mind if dealing with charge offs:

- You have the right to request debt validation before paying collections

- Collectors must honor a request to stop contacting you

- You may dispute inaccurate information on your credit reports

- Debt collectors cannot harass, threaten, or abuse you

- Time-barred debt is too old to sue over in court

Don’t let unlawful collection tactics pressure you into repaying expired debt or inaccurate charge offs. Seek help from a credit counseling agency or lawyer if in doubt.

Key Takeaways

- Charge off is an accounting procedure for lenders to write off bad debt

- Consumers still owe the debt even after it’s charged off

- Severely delinquent accounts get charged off around 120-180 days late

- Charge offs damage credit scores for 7 years

- Avoid charge offs by staying on top of finances and minimum payments

- Carefully weigh options like payment plans, settlements, or bankruptcy

How a Charge-Off Works

If a company is willing to take a one-time charge against a particular accounting period, referred to as a charge-off, this likely means that an extraordinary event has occurred and, although it affects present earnings, it is unlikely to occur again in the foreseeable future. A charge such as this may also be referred to as a one-off, meaning that it is likely to only occur in this instance.

A charge-off of this nature can include the purchase of a large asset, such as a new facility or large piece of equipment, that is unlikely to be replaced for some time. Charge-offs can also include charges related to an uncommon event, such as repairs required after a fire that the company has been deemed responsible for paying or the payment of insurance deductibles for covered damages caused by a natural disaster.

What Is a Charge-Off?

In corporate finance, a charge-off can be one of several different things. A charge-off can refer to an item on a companys income statement that is either an uncollectible accounts receivable (non-payment of a bill owed to the company) or otherwise related to a debt owed to the company that is deemed uncollectible. In this case, a charge-off item is written off of the balance sheet in part or in full.

More commonly, a charge-off is a one-time extraordinary expense incurred by a company that negatively affects earnings and results in a write-down of some of the firms assets. The write-down arises due to impairments of assets.

- A charge-off can refer to an item on a companys income statement that is either an uncollectible accounts receivable or otherwise related to a debt owed to the company that is deemed uncollectible.

- More commonly, a charge-off is a one-time extraordinary expense incurred by a company that negatively affects earnings and results in a write-down of some of the firms assets.

- Companies will usually provide an earnings per share (EPS) figure with and without this charge to help demonstrate to stakeholders the irregular nature of the expense.

What does Charge Off mean on my Credit Report? Does Charged Off mean I don’t have to pay?

What is a charge-off in accounting?

A charge-off shares some similarities with another accounting term known as a write-off. A write-off refers to reducing the value of an asset to account for a loss, such as unpaid debt. The company removes, or writes off, the asset’s potential return on investment from the balance sheet.

What does a charge-off mean on a credit report?

A charge-off is a negative entry on your credit report indicating a creditor has written off a debt as a loss because it doesn’t believe you will repay the debt. Despite the charge-off, you’re still responsible for paying back the debt.

What is a debt charge-off?

A debt charge-off occurs when a creditor stops trying to collect an unpaid debt after the borrower has failed to make payments for several months. Although a charge-off means your lender will end attempts to reach you, it won’t legally absolve you from paying your debts.

When can a creditor use a charge-off?

A creditor or lender may use a charge-off when the borrower has become substantially delinquent after a period of time. Having a charge-off can mean serious repercussions on your credit history and future borrowing ability. A charge-off is when a company writes off debt as a loss.