Financial metrics are very important when it comes to analyzing how efficient your business is. Both cash cycle and operating cycle are a great way to measure your businesses financials. Often people think they are the same thing. While they are very similar, they have small differences that make them each very useful.

For any business, managing cash flow efficiently is critical to success. Two important metrics that provide insight into a company’s cash flow are the operating cycle and cash cycle. Though related, these cycles measure different aspects of a company’s finances. Understanding the differences between the operating cycle and cash cycle can help businesses optimize their cash management.

What is the Operating Cycle?

The operating cycle measures the time between when a company acquires inventory to when it receives cash from selling that inventory It represents the time required for a company to convert its cash investments in inventory back into cash from sales The operating cycle has three main phases

-

Procurement Phase – The time between when the company places an order to purchase inventory and when it receives the inventory. This includes purchase order processing time and delivery lead times.

-

Production Phase – For manufacturers, this is the time required to convert raw materials into finished goods ready for sale. For retailers/distributors, it is the time inventory is held until it is sold.

-

Sales Phase – The time from when inventory is sold to when cash is collected from the customer This depends on sales terms and collection processes,

To calculate the operating cycle, you add together the days in each phase:

Operating Cycle = Procurement Days + Production Days + Sales Days

A shorter operating cycle means a company converts inventory back into cash more quickly. This improves liquidity since less cash is tied up in inventory.

Here are some factors that affect the operating cycle length:

-

Industry – Some industries like manufacturing or retail tend to have longer operating cycles than service businesses.

-

Production processes – More complex production can lengthen the production phase.

-

Sales terms – Lenient credit terms for customers extend the sales phase.

-

Inventory management – Leaner inventory levels reduce production/sales phases.

-

Procurement practices – Strategic purchasing can shorten procurement lead times.

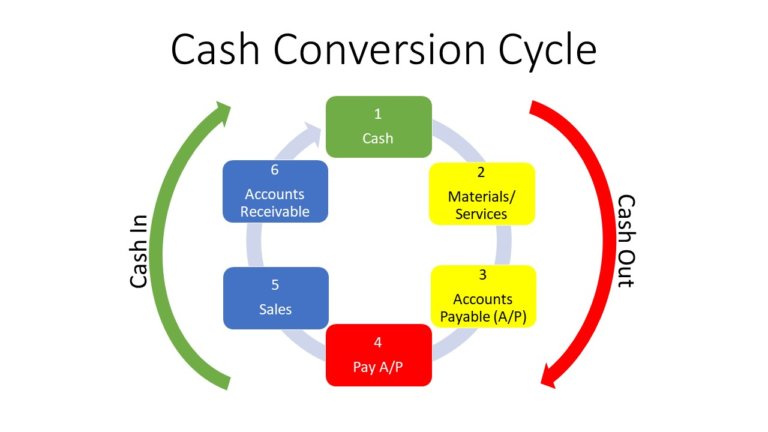

What is the Cash Cycle?

While the operating cycle measures inventory cycles, the cash cycle specifically looks at the time between cash outlays and cash inflows. Also called the cash conversion cycle, it measures how long cash is tied up in production before it returns as cash from sales.

The cash cycle has four main phases:

-

Payables Period – The time between purchasing inventory and paying suppliers. This depends on payment terms from suppliers.

-

Inventory Period – How long inventory is held before it is sold. This includes both raw materials and finished goods.

-

Receivables Period – The time from sale of inventory to collection of cash from customers. Depends on credit terms and collection efficiency.

-

Cash Cycle – Payables period + Inventory period + Receivables period.

A shorter cash cycle means a business has more efficient cash flow management. Cash is tied up for shorter periods between outlay and collection.

Factors impacting the cash cycle include:

-

Supplier terms – Better terms from suppliers extend payables period.

-

Inventory management – Lower inventory needs shortens the inventory period.

-

Credit policies – Stricter credit for customers shortens the receivables period.

-

Collection processes – Improved collections speeds cash inflows.

Key Differences Between the Cycles

While the operating and cash cycles both measure how quickly a company converts outlays back into cash inflows, there are some key differences:

-

Operating cycle focuses on inventory cycles from ordering to final sale. The cash cycle focuses specifically on cash outlay and inflow periods.

-

The operating cycle starts with procurement of inventory. The cash cycle starts with payments to suppliers.

-

The operating cycle ends when inventory is sold. The cash cycle ends when cash is collected from customers.

-

The operating cycle measures efficiency of inventory operations. The cash cycle measures how well cash flows are managed.

-

Improving the operating cycle can help shorten the cash cycle. But a short operating cycle does not directly correlate to an efficient cash cycle.

Why Measure the Operating and Cash Cycles?

Tracking these cycles provides visibility into different aspects of a company’s working capital management:

-

The operating cycle shows how efficiently a company is converting inventory investment into sales. This impacts profitability.

-

The cash cycle shows how well a company manages cash outlays versus inflows. This impacts liquidity.

Shortening these cycles provides benefits:

-

Frees up cash – Less cash tied up in inventory or waiting for customer payments means more cash availability.

-

Reduces costs – Lower inventory needs cuts warehouse, storage and maintenance costs.

-

Supports growth – More available cash allows reinvestment and growth initiatives.

-

Increases agility – Flexibility to respond to market changes due to healthy cash flow.

Tips for Optimizing the Cycles

Here are some tips businesses can use to shorten their operating and cash cycles:

-

Negotiate better supplier terms – Extending payables stretches out cash outlays.

-

Offer discounts for early payment – Encourage customers to pay invoices faster.

-

Adopt just-in-time inventory – Reduce inventory on hand through lean supply chain management.

-

Improve forecasting accuracy – Better align inventory levels to projected demand.

-

Implement strict credit policies – Enforce shorter payment terms for customers.

-

Accelerate invoicing and collections – Get invoices out faster and follow up on past due accounts.

-

Leverage technology – Use solutions to automate supply chain, inventory and cash flow management.

The operating cycle and cash cycle offer useful metrics for businesses to optimize working capital and cash flow. Though overlapping in some areas, they have distinct differences in what they measure. Understanding these differences allows companies to identify specific opportunities to improve their inventory and cash management processes. Analyzing both cycles together provides a more complete view of overall working capital efficiency. By shortening these cycles, companies free up significant cash resources while also reducing costs and improving agility to support growth.

What do they consist of?

Both the operating and cash cycle both consist of Days Inventory Outstanding and Days Sales Outstanding. Days Inventory Outstanding (DIO) is a metric that tells you the average days that a company holds inventory before turning it into sales. A high or low DIO can say a lot about a business. Days Sales Outstanding (DSO) is the measurement for the average number of days it takes a company to collect payment from a sale. If your DSO is trending one way or another is a sign something has changed. Where they differ is on the cash cycle. The cash cycle has another measurement on it called Days Payable outstanding. Days Payable Outstanding (DPO) is a metric that indicates the average amount of time in days that a company takes to pay its bills and invoices. This could include things like suppliers or financiers. This also shows how well a company can manage its funds.

What is an Operating Cycle?

So, what is an operating cycle? The operating cycle is the amount of time it takes for a company to acquire inventory, sell the inventory, and receive payment from the customers in exchange for the inventory sold. The length of the operating cycle depends on the industry. Overall, an operating cycle can give a good picture of whether a company is able to pay off any liabilities. When a business owner understands the operating cycle better, they can make better decisions for the company.

The operating cycle is calculated by adding together your DIO and DS.

Operating Cycle vs. Cash Conversion Cycle | Financial Statement Analysis

What is the difference between operating cycle and cash conversion cycle?

The net operating cycle (NOC) is sometimes mistaken for the operational cycle (OC) (NOC). The cash conversion cycle, often known as the cash cycle, illustrates how long it takes a corporation to collect cash from the sale of inventory. To distinguish between the two:

What is operating cycle in accounting?

This raw material conversion to cash is called the operating or working capital cycle. How to Calculate using Formula? In terms of time, it is the time taken after the purchases of raw material till its translation into cash. The total of inventory holding period and receivable collection period of a firm is the operating cycle time of that firm.

What is the difference between operating cycle and cash flow?

A company’s operating cycle offers insight into its operating efficiencies, while a company’s cash cycle offers insight into how well they’re managing its cash flow. A company’s cash flow is essentially the movement of money into and out of the business.

How to calculate operating cycle & cash operating cycle?

Here, The Operating Cycle = Inventory Holding Period + Receivable Collection Period = 40 + 40 = 80 Days. Cash Operating Cycle = 80 Days – 20 Days (Supplier’s Credit) = 60 Days.