Many or all of the products featured here are from our partners who compensate us. This influences which products we write about and where and how the product appears on a page. However, this does not influence our evaluations. Our opinions are our own. Here is a list of our partners and heres how we make money.

Liquid net worth is a calculation that helps determine the health of your financial safety net. It measures your ability to handle regular and short-term financial needs — and how well you meet your long-term money goals.

Have you heard the saying that someone is house poor? This is because the monthly costs of owning a home can sometimes drain so much household income that theres little money for anything else.

Or maybe youve heard people — even with high incomes — complain that theyre living paycheck to paycheck.

These can be the symptoms of financial challenges brought on by having too little ready cash for the day-to-day costs of living. The money squeeze can also hamper the ability to save for future financial goals, such as vacations, major repairs and retirement.

If you spend most or all of what you earn and find it hard to save, improving your liquid net worth can be an important first step to breaking out of financial insecurity.

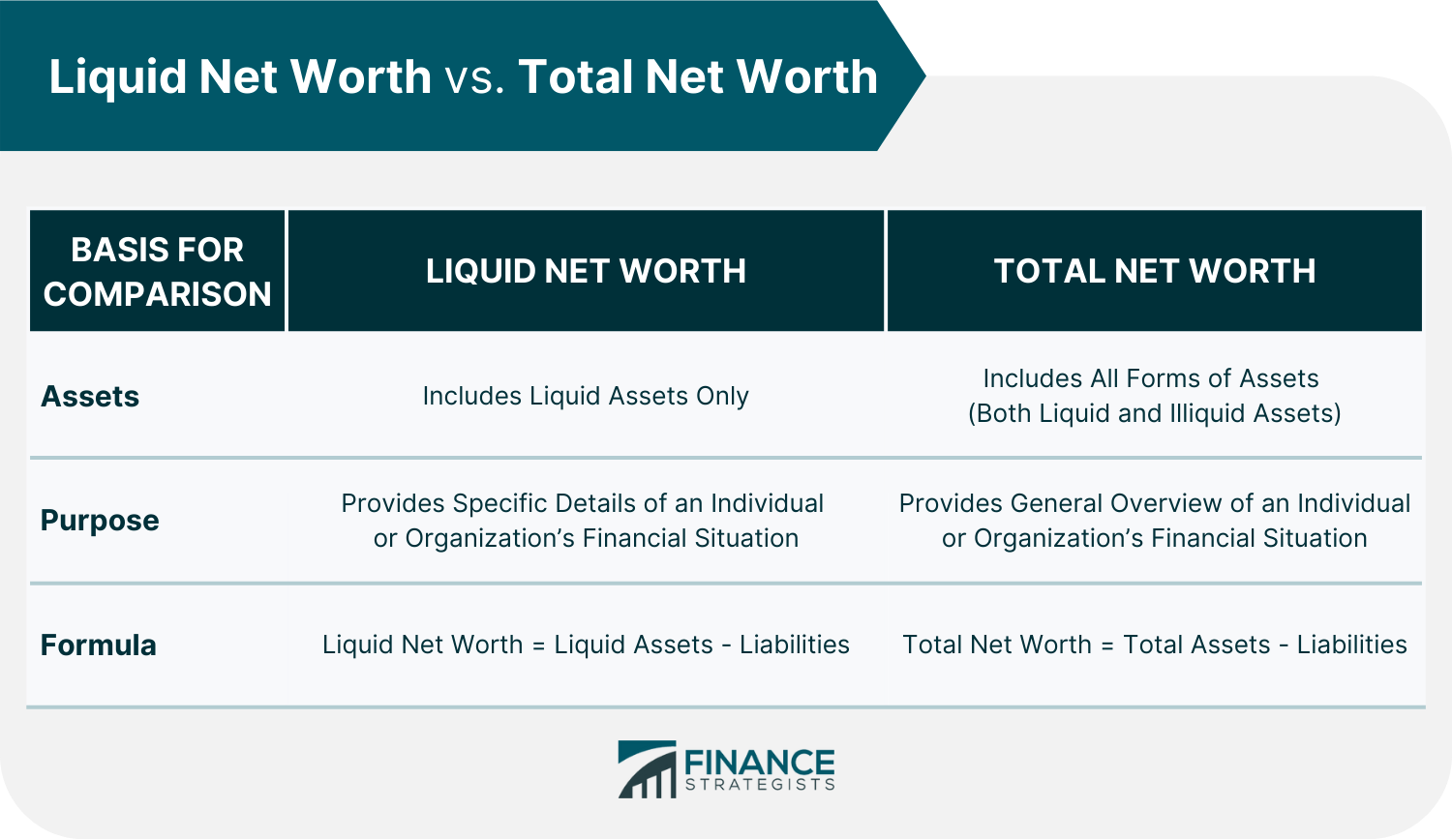

Determining your financial position is an important part of managing your money and planning for the future Two common metrics used to evaluate finances are net worth and liquid net worth While these terms sound similar, they measure very different things. Understanding the differences between net worth and liquid net worth can provide a clearer picture of your financial situation.

What is Net Worth?

Your net worth is the total value of everything you own minus the debts you owe. To calculate your net worth:

-

Add up the value of your assets – things like cash, investments, retirement accounts, real estate, cars, etc.

-

Add up the value of your liabilities – debts like mortgages, student loans, credit card balances, etc.

-

Subtract your liabilities from your assets.

The result is your net worth. A positive net worth means your assets are worth more than your liabilities. A negative net worth means your debts exceed the value of your assets.

Net worth provides a big picture overview of your finances. It encompasses all your assets, not just money or things that can quickly be turned into cash. This makes it a helpful metric for long-term financial planning.

What is Liquid Net Worth?

Liquid net worth focuses specifically on assets that are cash or can quickly become cash. Liquid assets include:

- Cash – money in checking and savings accounts

- Money market funds

- Certificates of deposit (CDs)

- Stocks and bonds

- Mutual funds

To determine your liquid net worth:

- Add up the value of only your liquid assets

- Subtract the total value of your liabilities

The result is your liquid net worth. It excludes illiquid assets like real estate retirement accounts collectibles, and consumer durables.

Liquid net worth helps assess your short-term financial flexibility. It provides an idea of how much money you could access quickly if needed. This makes it useful for evaluating your near-term cash flow and ability to handle unexpected expenses.

Key Differences Between Net Worth and Liquid Net Worth

While net worth and liquid net worth both provide insight into your finances, there are some key differences:

Assets Included

- Net worth includes all assets – liquid and illiquid

- Liquid net worth includes only liquid assets readily convertible to cash

This means real estate, retirement accounts, cars, and other illiquid assets are excluded from liquid net worth but included in net worth.

Time Horizon

- Net worth provides a big picture, long-term view

- Liquid net worth focuses on short-term finances

Net worth encompasses assets you’ve accumulated over your lifetime. Liquid net worth indicates how much cash you could access quickly if needed today.

Usefulness

- Net worth helps with long-term financial planning

- Liquid net worth assesses short-term cash flow

Net worth gives insight into your overall financial position and wealth building. Liquid net worth indicates your ability to cover near-term expenses and financial obligations.

Flexibility

- Net worth changes slowly over time

- Liquid net worth can change quickly

Illiquid assets like real estate appreciate gradually. But liquid assets like stocks can change in value daily. So liquid net worth is more variable.

Real World Examples Comparing Net Worth and Liquid Net Worth

Here are some examples that illustrate the differences between net worth and liquid net worth:

Example 1:

John has $100,000 in retirement accounts, owns a house worth $300,000, and has $20,000 in a brokerage account. His only debt is a $200,000 mortgage on his house.

- Net worth:

- Assets = $100,000 + $300,000 + $20,000 = $420,000

- Liabilities = $200,000 (mortgage)

- Net worth = $420,000 – $200,000 = $220,000

- Liquid net worth:

- Liquid assets = $20,000

- Liabilities = $200,000

- Liquid net worth = $20,000 – $200,000 = -$180,000

Even though John has a positive net worth, his liquid net worth is negative because his assets are tied up in illiquid real estate and retirement accounts.

Example 2:

Mary has $15,000 in checking, $10,000 in savings, $50,000 in stocks, and a paid-off car worth $15,000. She has $25,000 in student loan debt.

- Net worth:

- Assets = $15,000 + $10,000 + $50,000 + $15,000 = $90,000

- Liabilities = $25,000

- Net worth = $90,000 – $25,000 = $65,000

- Liquid net worth:

- Liquid assets = $15,000 + $10,000 + $50,000 = $75,000

- Liabilities = $25,000

- Liquid net worth = $75,000 – $25,000 = $50,000

Mary has the majority of her net worth tied up in liquid assets, so her liquid net worth is close to her overall net worth.

When Liquid Net Worth Diverges from Net Worth

There are certain situations that can cause someone’s liquid net worth to diverge significantly from their net worth:

-

Owning illiquid assets like real estate: As seen in John’s example above, extensive real estate holdings relative to liquid assets can result in low or negative liquid net worth despite positive overall net worth.

-

Self-employed with business assets: Business owners may have lots of illiquid assets like property, equipment, and inventory tied up in their business. Their personal liquid net worth could be disproportionately low compared to net worth.

-

Age and stage of life: Younger people tend to have lower net worth but higher liquidity. Retirees often have higher net worth with assets tied up in home equity and retirement savings.

-

Income and cash flow: Individuals with high net worth but low cash flow can experience liquidity issues if they overextend themselves or don’t budget properly.

When to Use Net Worth vs Liquid Net Worth

Both net worth and liquid net worth provide valuable but different glimpses into your financial picture. Some situations where each metric is useful:

Use net worth for:

- Long-term financial planning and wealth building

- Getting a big picture overview of your finances

- Tracking financial progress over decades

- Retirement planning

- Estate planning

Use liquid net worth for:

- Evaluating ability to pay expenses and manage cash flow

- Assessing ability to handle unexpected costs

- Short-term savings goals like emergency fund

- Near-term purchasing decisions – buying a house, car, major appliance, etc.

- Budgeting monthly spending

How to Improve Net Worth and Liquid Net Worth

Building wealth and financial stability requires growing your net worth over the long run and maintaining adequate liquidity. Here are some tips:

Increase net worth:

- Contribute to retirement accounts

- Pay down debts

- Invest extra money in brokerage accounts

- Build home equity through mortgage payments

- Negotiate job promotions and raises

Improve liquidity:

- Build up emergency fund

- Hold some investments in liquid assets like stocks

- Maintain low credit card balances

- Reduce excess spending to boost cash reserves

- Consider credit line for access to funds if needed

Balancing illiquid and liquid assets is key. The ideal situation is having a steadily increasing net worth while maintaining enough liquidity to cover short-term needs.

Consulting a Financial Advisor

An experienced financial advisor can help you assess your net worth and liquidity. They can also create a customized plan to build wealth while ensuring you have access to cash when needed. Some key benefits of working with an advisor include:

- Determining your optimal asset allocation based on age, income, goals

- Tax-efficient investing and retirement withdrawal strategies

- Debt pay down prioritization

- Budgeting to balance saving and spending

- Advice on major purchase decisions

With professional guidance, you can feel confident you are taking the right steps to strengthen your finances for the short and long term.

Net Worth vs Liquid Net Worth – The Bottom Line

Net worth provides a 30,000 foot view of your lifetime financial situation. Liquid net worth zooms in on your immediate ability to access cash. These two metrics offer complementary lenses into your finances. Tracking both your net worth and liquid net worth over time can provide tremendous insight into your financial health and wealth building progress. With this comprehensive picture, you can pursue the optimal saving, investing, and spending strategies for your situation.

Exactly what are liquid assets?

Liquid assets are holdings that are in cash or can be converted into cash within a very short time. For example, if you have money in a checking, savings or money market account, you can withdraw it at any time without penalty or loss of value.

On the other hand, some things are “illiquid.” For example, if you have to hold an asset for an extended time, perhaps 30 days or more, before it can be issued as cash, it is not a liquid asset. And if the quick sale of an investment would significantly decrease its value, it is not considered liquid.

Stocks and bonds are usually considered liquid because you can sell these investments and have a cash settlement generally within two business days. However, if a stock is not actively traded or has a volatile market price that might cause a significant loss in the event of a quick sale, it is likely not meeting the standards of a liquid asset. In addition, a high quantity of shares of an individual stock might also not be regarded as liquid because selling a large block all at once might impact its value.

Real estate, antiques, jewelry, collectibles and many other hard assets are generally illiquid because quick-turn sales might not be possible.

So liquid assets are easy to sell and access — and arent subject to a sudden loss in value if converted to cash.

How to calculate your liquid net worth

Lets look at the following financial profile as an example.

Perhaps your assets include:

- A house worth $300,000.

- A car worth $30,000.

- You also have a 401(k) and an IRA worth a combined total of $250,000.

- There is $6,000 in your checking account.

- You have $10,000 in a savings account.

- And $100,000 in mutual funds in a brokerage account.

As for your financial liabilities, you owe:

- $100,000 on the home.

- $5,000 on the car.

- $5,000 in student loans.

- And $2,000 on credit cards.

Heres how your liquid net worth would be calculated:

Your liquid assets total $116,000 (the total of the checking, savings and brokerage accounts).

Your liabilities total $112,000 (the loans on the house, car, student loans and credit cards).

The liquid assets of $116,000 minus liabilities of $112,000 equals $4,000 liquid net worth.

Remember, for liquid net worth, we excluded the house, car and retirement accounts. Thats because you likely cant sell your home and vehicle quickly for cash, and generally, there is a penalty for withdrawing retirement assets before age 59 and a half.

The checking and savings accounts are held in cash, and the brokerage account holdings can be converted to cash within two to three days by selling the mutual funds, so they are considered liquid.

Net Worth vs Liquid Net Worth Meaning & Why They’re Important

What constitutes liquid net worth?

Liquid Net Worth Defined. Liquid net worth is the amount of money you’ve got in cash or cash equivalents after you deducted your liabilities from your liquid assets. It’s quite similar to net worth, but the only difference is that it doesn’t account for non-liquid assets such as real estate or retirement accounts.

How to calculate your net worth?

How to calculate net worth. The formula isn’t complicated. As noted, you simply add up all of your assets. Then you add up all of your debts. Then you subtract your debts from the assets. Voila! You have your net worth. Busch recommends including your home equity in your net worth.

What is your true net worth?

Your net worth isn’t about your income—your income doesn’t even factor into your net worth. Instead net worth includes savings, investments, and debts. Think about it this way: If you make $30,000 per year, but you have an investment portfolio worth $3.5 million, you’re going to be more concerned about your total net worth because the