We saved more than $1 million on our spend in the first year and just recently identified an opportunity to save about $10,000 every month on recurring expenses with Planergy.

Job costing, also known as job order costing, and process costing are cost accounting systems designed to help businesses keep track of all the costs they have to pay to produce a product or deliver a service.

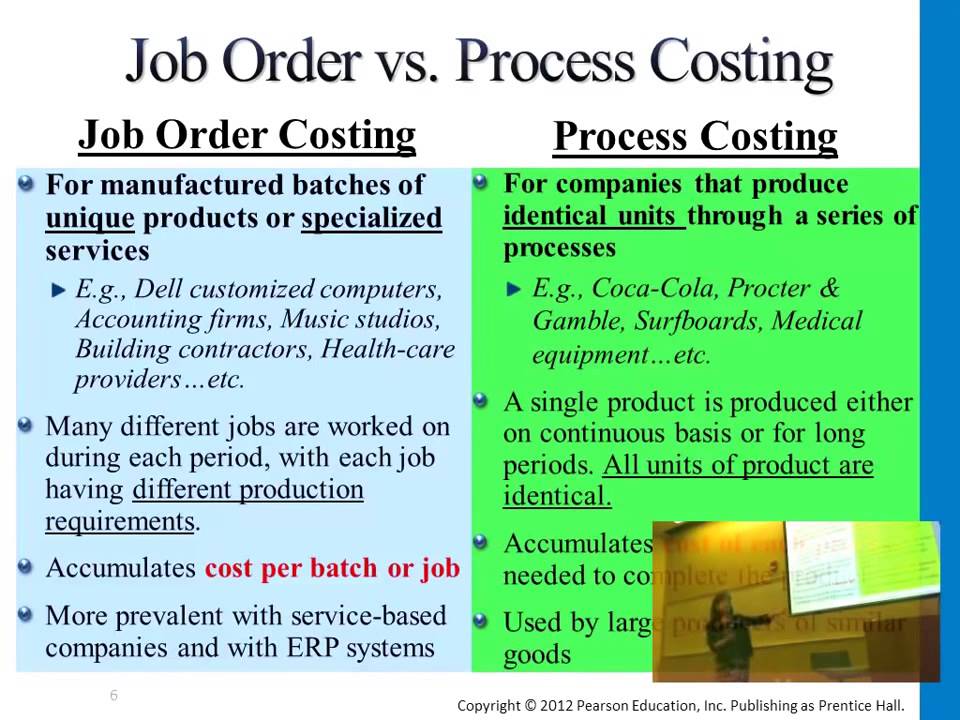

In manufacturing, there are two main methods for tracking production costs – job order costing and process costing. Understanding the difference is key for managers to choose the right system.

This in-depth guide examines job order and process costing It covers

- Definitions and examples

- How costs are tracked

- Production volume differences

- Recording details

- Usage in pricing

- When to use each method

- Hybrid approaches

Mastering these concepts allows organizations to deploy the costing approach best suited to their operations

Overview of Job Order Costing

With job order costing, manufacturers accumulate costs for each unique job or batch. Jobs can range from a one-off custom order to a small production run.

Costs are carefully traced to each job. Labor time sheets record employee time spent on specific jobs. Material and component usage is documented per job. Overhead costs may be allocated to jobs based on factors like direct labor hours.

Job order costing provides detailed insight into costs for customized orders. It is commonly used in:

- Construction

- Engineering services

- Custom furniture building

- Printing services

Each job is unique, so accurate cost capture is crucial for pricing and performance analysis.

Overview of Process Costing

Process costing aggregates costs across mass-produced goods. Large volumes of identical units are created through continuous manufacturing methods.

Rather than track costs by job, expenses are compiled by department or cost center. The production process is broken into stages. Costs at each stage are divided by the output volume to derive a per unit cost.

Process costing suits high-volume industries like:

- Petroleum refining

- Chemical processing

- Food production

- Consumer electronics

The goal is to calculate an average cost per standard unit. Individual units are indistinguishable from each other.

Tracking Costs in Each Method

Job order and process costing track direct material, direct labor, and overhead costs differently:

- Direct material: In job order costing, materials are traced to specific jobs. Process costing allocates an average material cost per unit produced.

- Direct labor: For job order costing, employees log hours to jobs. Process costing averages labor cost across units.

- Overhead: Job costing may allocate overhead using rates per labor hour. Process costing averages total overhead across production volume.

Job costing provides very detailed cost data per job. Process costing gives a higher-level view of average costs per department.

Production Volume Differences

Job costing and process costing suit different production scales and batches:

- Job costing handles small batches and custom orders. Production volume per job ranges from one unit to several dozen. Each job is unique.

- Process costing is designed for long production runs of thousands to millions of identical units. High throughput justifies the cost of dedicated equipment.

Below certain volume thresholds, the overhead of process costing outweighs the benefits. Job costing better suits small batch and custom manufacturing.

Cost Accounting Details

The level of accounting detail also differs:

- Job costing traces costs to the discrete job or lot level. Extensive records are maintained per job. This facilitates customer billing.

- Process costing accumulates costs by department. No costs are tracked at the individual unit level. Only a company-wide income statement can be produced.

The right approach depends on the production process and customer requirements. Job costing provides billable data for customer invoices. Process costing gives high-level departmental data to analyze efficiencies.

Usage in Pricing

These different cost views impact pricing methods:

- Job costing supports billable job cost data. This facilitates cost-plus pricing where the customer is quoted cost per job plus a markup percentage.

- Process costing derives an average cost per unit. Markups are based on this estimated unit cost. Limited visibility into per-job costs prevents cost-plus pricing.

Job costing allows passing actual costs to customers. Process costing relies on price lists based on average costs.

When to Use Each Method

In general:

- Use job order costing for:

- Custom manufacturing with unique jobs

- Small batches

- Products built to customer specifications

- Situations requiring detailed per-job cost accounting

- Use process costing for:

- Mass production of identical goods

- Continuous processing without breaks between batches

- High-volume output of thousands to millions of units

- When average per-unit costs are sufficient

Evaluate production methods, volumes, batch sizes, and cost information needs to determine the best fit.

Hybrid Approach

In some cases, a hybrid approach combines aspects of job order and process costing:

- The manufacturing process involves mass production with process costing.

- Finished goods are customized before shipment to customers.

- The customization work uses job order costing to track specific customization costs.

- Total cost per unit = process costs + job customization costs.

This method works well for mass-produced goods like vehicles with dealer custom add-ons. The base manufacturing cost is calculated via process costing. The custom work done by dealers uses job order costing.

Putting It All Together

- Job costing traces direct costs to unique jobs and batches. It provides very detailed cost accounting but requires extensive record keeping.

- Process costing averages costs across a high volume of identical units. It provides less detailed data but requires less record keeping.

Matching the method to production volumes and cost data needs ensures efficient cost tracking. Analyzing cost behavior also drives better pricing decisions and cost management.

Understanding the differences between job order costing and process costing allows organizations to deploy the best approach based on their manufacturing methods, volumes, and cost accounting requirements.

What is Job Costing?

With the job costing approach, your business completes work on a project basis. The total cost for each job is different.

This is the case for plumbers, mechanics, freelancers, movers, and anyone who works in a trade or provides customers an estimate before doing any work.

If you hire movers to move your items from one home to another – either local or long distance – the moving company will estimate the labor costs, equipment, and anything else they need for the project, along with a profit margin, then provide you with an estimate.

Each job is different, depending on the size of the home, whether or not the items are packed ahead of time or to be packed in advance of the move, and the distance between homes.

Each job is a project that has its own distinct entity.

- No job is the same. Each job will have to be done differently to successfully complete it.

- Based on client requirements or needs.

- The difference in work in progress exists in each period.

Setting Up a Costing System

Before you can set up an effective job or processing costing system, you have to separate direct costs from indirect, or overhead costs.

Overhead costs are the most difficult to assign to products, and many businesses struggle to analyze these costs. Overhead costs cannot be directly traced to products or services, which makes them harder to track and manage. Utility costs and insurance premiums are examples.

Direct costs, on the other hand, can easily be traced to specific products or services. If you manufacture face masks, you can calculate the amount of each fabric (raw materials) you use in each mask for direct materials and the direct labor costs it takes to run the machines. Because of this, labor and material costs are considered direct costs.

Blockquote: “The costing system you use determines how expenses are tracked, and may even play a role in how you price your products and services.”

Job Order Costing vs Process Costing – Accounting

What is the difference between Job costing and process costing?

Job costing is used for very small production runs (or even single-unit jobs), and process costing is used for large production runs. Much more record keeping is required for job costing, since time and materials must be charged to specific jobs. Process costing aggregates costs, and so requires less record keeping.

What is job order costing?

Job order costing is a way to track the production of small and unique batches of products ordered by customers. In a job order costing system, you can track the price of each individual project and ensure that your company earns enough profit on each order to sustain your operations.

Which costing method is chosen based on the production process?

The costing method is chosen based on the production process. In job order cost production, the costs can be directly traced to the job, and the job cost sheet contains the total expenses for that job. Process costing is optimal when the costs cannot be traced directly to the job.

Which company uses process costing?

For example, General Mills uses process costing for its cereal, pasta, baking products, and pet foods. Job order systems are custom orders because the cost of the direct material and direct labor are traced directly to the job being produced. For example, Boeing uses job order costing to manufacture planes.