Job costing is an essential component of construction accounting. With so much to keep track of, it’s easy to let construction projects get out of control—potentially facing expensive surprises further down the line, whether that is due to extra labor, faulty equipment, or simply a loss of potential profits when a project exceeds your original budget.

To maximize your profit and the success of your projects, you need an accurate view of all ongoing work, teams, and individual jobs. Even one small oversight can disrupt the entire project workflow and chip away at your profits. That’s why it’s more important than ever to plan individual jobs effectively, looking at every element in detail through job costing.

In this article, youll learn everything you need to know about construction job costing, from the basics of what it is, to a breakdown of all the costs you need to track, and how job costing software can help to make sure your construction jobs stay profitable.

“Job costing is the heartbeat of construction management, providing the vital signs needed to ensure a projects financial health.” – John Meibers, VP & GM, Deltek ComputerEase

Deciding between job costing and process costing systems can be a challenging task for companies The type of costing method you choose has a direct impact on how you track expenses and may even influence pricing decisions. In this article, we’ll explain the key differences between job costing and process costing to help you determine the best approach for your business

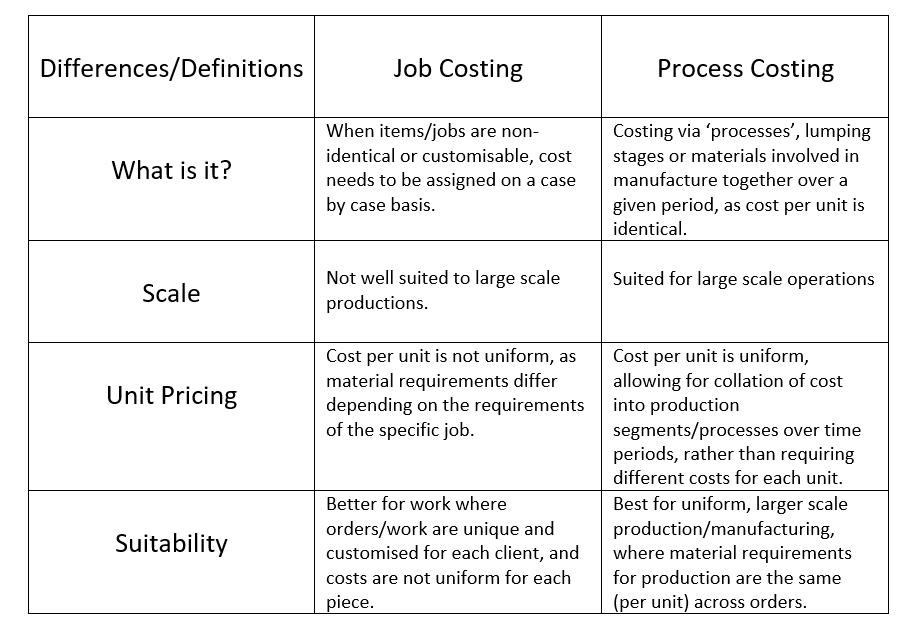

What is Job Costing?

Job costing also known as job order costing is a cost accounting system used for unique, custom, or specialized products. With job costing, costs are compiled for each individual project or ‘job’.

For example a home renovation company would use job costing. They bid on projects like kitchen remodels bathroom remodels, additions, etc. Each project is different based on the homeowner’s needs. The company tracks the costs of materials and labor that are directly tied to each specific job. They can then know their true costs and profit margins on a per project basis.

Other examples of companies that use job costing:

- Construction companies

- Law firms

- Creative agencies

- Automotive repair shops

The key attributes of job costing include:

- Production is customized for each job

- Costs are carefully tracked per individual job

- Used for small production runs or unique products

- More detailed recordkeeping required

- Supports customer billing based on actual costs

What is Process Costing?

Process costing is best for companies mass producing large volumes of identical or very similar products. Instead of tracking costs for each unit, costs are averaged across a batch or production run.

For example, a bakery that produces thousands of loaves of bread would use process costing. While each loaf of bread is not exactly identical, they are substantially similar. The bakery tracks costs for each batch of bread. This includes direct materials like flour, yeast, etc. It also includes direct labor by the production team. Overhead costs like utilities are allocated to each batch.

Other examples of process costing users:

- Food and beverage plants

- Oil refineries

- Chemical manufacturers

The key attributes of process costing include:

- Production is standardized

- Costs are accumulated by department and averaged per unit

- Used for large production volumes

- Simpler recordkeeping

- Supports decision-making but not customer billing

Key Differences Between Job Costing and Process Costing

While both job costing and process costing provide valuable cost information, there are some notable differences between the two methodologies:

1. Uniqueness of Product

Job costing is used for unique, specialized, or custom products. Process costing is used for standardized products produced in high volumes.

2. Size of Production Batch

Job costing is optimal for small batches or individual units. Process costing is better suited for large production runs with thousands or more identical units.

3. Recordkeeping Requirements

Job costing demands more detailed recordkeeping to track costs for each job. Process costing aggregates costs so the accounting is simpler.

4. Customer Billing

Job costing supports customer billing based on actual costs of customized work. Process costing does not facilitate billing since it averages costs over batches.

5. Cost Reduction Opportunities

Job costing provides less potential for cost reduction since each job varies. Process costing offers more potential for refinements and savings over time.

6. Work in Progress

For job costing, work in progress inventory balances fluctuate job to job. Process costing has consistent beginning and ending balances each period.

7. Cost Transfers

In job costing, costs cannot be transferred between jobs. With process costing, costs can be allocated between processes.

8. Nature of Product

Job costing allows for total customization and individuality in end products. Process costing leads to standardized products that lack uniqueness.

9. Type of Industry

Job costing suits customer-driven industries that produce customized orders. Process costing is optimal for mass production such as manufacturing.

10. Handling of Losses

Losses are more difficult to isolate in job costing. Process costing makes it easier to separate out abnormal losses.

Real World Examples

Below we’ll examine examples of companies using job costing vs process costing:

Job Costing Example

ABC Contracting is a home builder that constructs custom houses for clients. Each house is a unique job based on the customer’s design. ABC tracks material costs like lumber, pipes, and flooring for each house. They track labor hours for framers, plumbers, and other trades working on each job site. At the end of a job, they can derive the total cost to build that home. Overhead costs like insurance and supervision are allocated to each house based on labor hours.

Process Costing Example

XYZ Brewery produces beer in large batches. While each batch may vary slightly in ingredients, the end product is substantially similar. XYZ tracks the costs of raw materials like barley, hops, and yeast for each batch. The labor hours in the brewing, fermenting, and packaging process are tracked at the department level. Overhead costs like warehouse rent are spread across each production batch. Rather than tracking costs for each bottle or case, XYZ looks at total costs for the batch run.

Implementing a Costing System

When setting up a job costing or process costing system, first separate out direct vs overhead costs:

-

Direct costs: Easily traceable to a product or service (e.g. materials, commissioned labor).

-

Overhead costs: Difficult to directly allocate to products (e.g. rent, utilities).

For overhead costs, develop an allocation method such as labor hours or machine hours. This allows you to spread overhead consistently across jobs or production runs.

Create a budget for anticipated direct and overhead costs. Compare actual costs to the budget monthly to identify variances. Tweak your costing system over time to become more accurate in projecting true costs.

Which Method is Right For Your Business?

When deciding between job vs process costing, consider:

- What do you produce? Unique items or standardized products?

- What volumes do you produce? Small batches or mass quantities?

- How important is precise project cost data for billing?

- How complex is your manufacturing/production process?

Of course, you may need elements of both systems. For example, a furniture maker using job costing for custom work can use process costing for their standard product line.

Implementing an effective costing system takes time and discipline. But the visibility it provides into your true costs and profitability makes it a worthwhile investment. With quality data, you can price appropriately and make sound production decisions.

So analyze your business carefully, set up processes to collect reliable cost information, and choose the costing method(s) that best fit your operations. This will provide the foundation for smart management going forward.

Measure Your Business Success With Job Costing

Take the first crucial step towards becoming a construction accounting expert through Construction Accounting University.

How to Calculate Job Costing

How do you calculate construction job costing? It comes down to a simple job costing process based on a calculation of all individual costs. Your total construction job cost is the sum of all materials, labor, equipment, subcontractor costs, and overheads. Each category also has its own job costing formula to allow you to determine the overall cost of the job accurately.

In addition to actual labor costs for regular and overtime employees you need to account for employer-based payroll taxes (burden) as well as cost for providing benefits to employees (fringes).

Its also important to calculate indirect labor costs for in-house workers, such as project managers, account managers, or those in charge of purchasing equipment. Usually, these employees are paid an annual salary, so you’ll need to work out their hourly or daily rate, inclusive of other costs like insurance and tax.

While the total fee of each overhead cost isn’t directly associated with the job, some percentage of each amount will contribute to each job. As a result, many businesses add a percentage to every job to account for overhead costs. For the most accurate job costing, you’ll need to make sure that all of the overhead is accounted for.

Job Order Costing vs Process Costing

What is the difference between job and process costing?

As job and process costing is used in different industries, there cannot be any comparison between them. Although the methods are different, the main difference can be that job costing requires a higher degree of supervision, but process costing does not need so. There are also situations where a company can have both.

What is job costing?

Job costing is more likely to be used for billings to customers, since it details the exact costs consumed by projects commissioned by customers. This is the case when the seller is billing based on cost, as is the case with a arrangement.

What is the difference between Job Order cost production and process costing?

In job order cost production, the costs can be directly traced to the job, and the job cost sheet contains the total expenses for that job. Process costing is optimal when the costs cannot be traced directly to the job. For example, it would be impossible for David and William to trace the exact amount of eggs in each chocolate chip cookie.

Does the process of production change based on the costing method?

The process of production does not change because of the costing method. The costing method is chosen based on the production process. In job order cost production, the costs can be directly traced to the job, and the job cost sheet contains the total expenses for that job.