A company may no longer need a fixed asset that it owns, or an asset may have become obsolete or inefficient. In this case, the company may dispose of the asset. Prior to discussing disposals, the concepts of gain and loss need to be clarified.

A gain results when an asset is disposed of in exchange for something of greater value.

Gains are increases in the business’s wealth resulting from peripheral activities unrelated to its main operations. Recall that revenue is earnings a business generates by selling products and/or services to customers in the course of normal business operations. That is, earnings result from the business doing what it was set up to do operationally, such as a dry cleaning business cleaning customers’ clothes. A gain is different in that it results from a transaction outside of the business’s normal operations. Although in terms of debits and credits a gain account is treated similarly to a revenue account, it is maintained in a separate account from revenue. In that way the results of gains are not mixed with operations revenues, which would make it difficult for companies to track operation profits and losses—a key element of gauging a company’s success.

Similarly, losses are decreases in a business’s wealth due to non-operational transactions. Recall that expenses are the costs associated with earning revenues, which is not the case for losses. Although in terms of debits and credits a loss account is treated similarly to an expense account, it is maintained in a separate account so as not to impact the net income amount from operations.

Both gains and losses do appear on the income statement, but they are listed under a category called “other revenue and expenses” or similar heading. This category appears below the net income from operations line so it is clear that these gains and losses are non-operational results.

Recording fixed asset disposals is an important accounting process that must be handled properly. Mistakes here can lead to incorrect financial statements that misstate the true value of a company’s assets.

In this comprehensive guide, we’ll walk through the key steps and best practices to accurately record asset disposals in your books.

Why Recording Disposals Matters

Properly accounting for asset disposals serves several crucial purposes

- Removes disposed assets from your books at the correct net book value

- Captures any gain or loss on disposal for reporting

- Provides an audit trail documenting assets that were sold or scrapped

- Prevents overstatement of assets on financial statements

- Helps calculate accurate depreciation going forward

- Enables correct calculation of taxes on sold assets

In short, recording disposals keeps your fixed asset registry up-to-date This ensures your financial reporting reflects reality

Gather Required Information

Before recording the disposal, compile key information including:

-

Description of disposed asset: Name, ID number, serial number, etc.

-

Disposal date: The date the asset was sold or discarded.

-

Original cost: The acquisition cost of the asset.

-

Accumulated depreciation: Total depreciation expense recognized over the asset’s lifetime.

-

Proceeds from sale: If sold, the amount of cash received.

-

Disposal expenses: Any costs related to selling or discarding the asset.

This data provides the details needed for journal entries. Consult your fixed asset register, invoices, depreciation schedules, and other records to collect information.

Calculate Gain or Loss on Disposal

If the disposed asset was sold, you’ll need to calculate any gain or loss on the sale. Here is the formula:

Gain (Loss) on Disposal = Net Book Value – Proceeds from Sale

Where:

- Net Book Value = Original Cost – Accumulated Depreciation

- Proceeds from Sale = Cash received from selling the asset

If proceeds exceed net book value, there is a gain. If proceeds are less than net book value, there is a loss.

This gain or loss will be recorded separately from disposing of the asset itself.

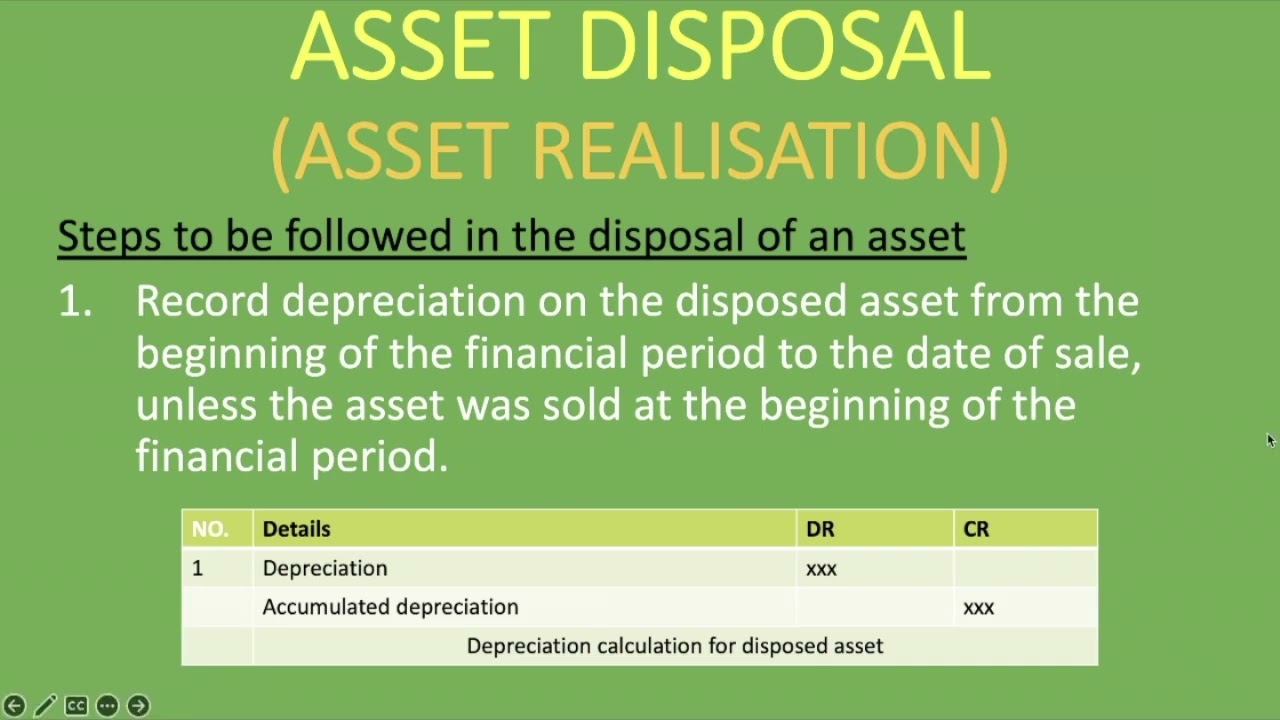

Journal Entry to Dispose of an Asset

The main journal entry to record an asset disposal removes it from your books at its net book value.

Entry to dispose of a sold asset:

| Account | Debit | Credit |

|---|---|---|

| Cash | Proceeds from sale | |

| Accumulated depreciation | Asset’s accumulated depreciation | |

| Gain/loss on disposal | Gain or loss amount | |

| Asset account | Asset’s original cost |

Entry to dispose of a scrapped asset:

| Account | Debit | Credit |

|---|---|---|

| Accumulated depreciation | Asset’s accumulated depreciation | |

| Loss on disposal | Net book value | |

| Asset account | Asset’s original cost |

These entries write off the asset, remove accumulated depreciation, and record any gain or loss.

Record Gain or Loss on Disposal

If the disposed asset was sold, record any gain or loss using this entry:

| Account | Debit | Credit |

|---|---|---|

| Gain/Loss on Disposal | Gain amount | Loss amount |

| Cash | Gain amount |

The gain or loss account appears on the income statement. This ensures the true profitability of the asset disposal is reflected.

Update Fixed Asset Register

Be sure to update your fixed asset register to indicate the asset was disposed. This typically involves:

- Adding disposal date

- Marking asset as retired/disposed

- Recording proceeds received

- Noting gain/loss amount

- Removing future depreciation

Maintaining an updated register ensures you can generate accurate financial reports.

Recalculate Depreciation

Going forward, your depreciation expense will change due to the disposed asset.

Recalculate the total depreciation for the period. Be sure to subtract all depreciation related to the disposed asset.

For future periods, remove the disposed asset from depreciation calculations completely.

Adjust Tax Reporting

For tax purposes, you may need to report the details of assets sold at a gain or loss.

Review tax regulations to determine all compliance requirements. You may need to attach supporting forms regarding the disposal.

Document Supporting Details

Retain documentation on asset disposals for auditing purposes. This includes:

- Invoices showing proceeds received

- Bills of sale

- Documentation of scrapping/disposal

- Calculation of gain/loss

- Journal entries

- Authorization records

Thorough documentation provides the paper trail to validate your recorded amounts.

Review Disposal Process Controls

Take time to review controls around your asset disposal process. Identify any improvements to ensure disposals are recorded timely and accurately going forward.

Example process controls:

- Require disposal forms to record all details

- Mandate manager approval of disposals

- Log all disposed assets in a disposal register

- Perform secondary review of disposal journal entries

- Run depreciation reports to identify disposed assets

Strong controls minimize the risk of errors and fraudulent asset disposals.

Train Employees on Procedures

Provide training to employees involved in asset disposals on your company’s procedures and required documentation.

Educate them on the importance of recording disposals properly and the impacts of mistakes. Clarify their role in the process.

Ongoing training ensures staff turnover doesn’t result in lapses in accounting for disposals.

Leverage Software Tools

Today’s accounting systems provide automation for tracking assets from acquisition to retirement. Built-in controls help reduce disposal errors.

For example, software can automatically:

- Calculate gains/losses upon asset sale

- Generate disposal journal entries

- Remove disposed assets from depreciation

- Flag assets fully depreciated or missing disposal details

Explore solutions that integrate disposal workflows with your broader asset lifecycle. This provides a seamless, linked asset accounting system.

Review Disposals for Ongoing Accuracy

Periodically review recent asset disposals to spot any errors:

- Verify disposal date aligned to sales documentation

- Check gain/loss calculations

- Confirm disposed assets removed from depreciation

- Review application of proceeds and disposal expenses

Regular audits ensure your processes are working and assets retire fully and accurately.

The Bottom Line

Recording assets disposals properly is vital for accurate financial reporting and tax compliance. By following a clear, controlled disposal process and validating results, companies can retire assets seamlessly.

The key is integrating disposal tracking with broader fixed asset systems. This connects the asset lifecycle from acquisition to depreciation to retirement. With training and automation, asset disposals can become a smooth component of your accounting function.

Discarding a Fixed Asset (Loss)

Compare the book value to what was received for the asset. The truck’s book value is $7,000, but nothing is received for it if it is discarded. If truck is discarded at this point there is a $7,000 loss. Both account balances above must be set to zero to reflect the fact that the company no longer owns the truck. In addition, the loss must be recorded.

To record the transaction, debit Accumulated Depreciation for its $28,000 credit balance and credit Truck for its $35,000 debit balance. Debit Loss on Disposal of Truck for the difference.

| Date | Account | Debit | Credit |

| 12/31 | Loss on Disposal of Truck | 7,000 | ▲ Loss is an expense account that is increasing. |

| Accumulated Depreciation | 28,000 | ▼ Accumulated Dep. is a contra asset account that is decreasing. | |

| Truck | 35,000 | ▼ Truck is an asset account that is decreasing. |

SearchSearch this book

selected template will load here

This action is not available. 4: Assets in More DetailPrinciples of Financial Accounting (Jonick){ }{ “4.01:_Inventory” : “property get [Map MindTouch.Deki.Logic.ExtensionProcessorQueryProvider+<>c__DisplayClass230_0.

( ewcommand{vecs}[1]{overset { scriptstyle rightharpoonup} {mathbf{#1}} } )

( ewcommand{vecd}[1]{overset{-!-!rightharpoonup}{vphantom{a}smash {#1}}} )

( ewcommand{id}{mathrm{id}}) ( ewcommand{Span}{mathrm{span}})

( ewcommand{kernel}{mathrm{null},}) ( ewcommand{range}{mathrm{range},})

( ewcommand{RealPart}{mathrm{Re}}) ( ewcommand{ImaginaryPart}{mathrm{Im}})

( ewcommand{Argument}{mathrm{Arg}}) ( ewcommand{ orm}[1]{| #1 |})

( ewcommand{inner}[2]{langle #1, #2 rangle})

( ewcommand{ orm}[1]{| #1 |})

( ewcommand{inner}[2]{langle #1, #2 rangle})

( ewcommand{Span}{mathrm{span}}) ( ewcommand{AA}{unicode[.8,0]{x212B}})

( ewcommand{vectorA}[1]{vec{#1}} % arrow)

( ewcommand{vectorAt}[1]{vec{text{#1}}} % arrow)

( ewcommand{vectorB}[1]{overset { scriptstyle rightharpoonup} {mathbf{#1}} } )

( ewcommand{vectE}[1]{overset{-!-!rightharpoonup}{vphantom{a}smash{mathbf {#1}}}} )

( ewcommand{vecs}[1]{overset { scriptstyle rightharpoonup} {mathbf{#1}} } )

( ewcommand{vecd}[1]{overset{-!-!rightharpoonup}{vphantom{a}smash {#1}}} )

A company may no longer need a fixed asset that it owns, or an asset may have become obsolete or inefficient. In this case, the company may dispose of the asset. Prior to discussing disposals, the concepts of gain and loss need to be clarified.

A gain results when an asset is disposed of in exchange for something of greater value.

Gains are increases in the business’s wealth resulting from peripheral activities unrelated to its main operations. Recall that revenue is earnings a business generates by selling products and/or services to customers in the course of normal business operations. That is, earnings result from the business doing what it was set up to do operationally, such as a dry cleaning business cleaning customers’ clothes. A gain is different in that it results from a transaction outside of the business’s normal operations. Although in terms of debits and credits a gain account is treated similarly to a revenue account, it is maintained in a separate account from revenue. In that way the results of gains are not mixed with operations revenues, which would make it difficult for companies to track operation profits and losses—a key element of gauging a company’s success.

Similarly, losses are decreases in a business’s wealth due to non-operational transactions. Recall that expenses are the costs associated with earning revenues, which is not the case for losses. Although in terms of debits and credits a loss account is treated similarly to an expense account, it is maintained in a separate account so as not to impact the net income amount from operations.

Both gains and losses do appear on the income statement, but they are listed under a category called “other revenue and expenses” or similar heading. This category appears below the net income from operations line so it is clear that these gains and losses are non-operational results.

Disposals of Fixed Assets and how to record in T accounts?

How do you record a disposal of an asset?

To record the disposal of an asset, an accountant will use a journal entry or a t account. Then update that transaction to the company’s financial records. The asset is removed from the balance sheet, and the corresponding value is adjusted, reflecting the loss or gain. 3. Depreciation Adjustment

How do you dispose of an asset?

There are many ways to dispose of an asset, but a crucial step is properly assigning disposal value. The disposal value is a numeric amount that equates to how much the asset is worth at the date of its deposition. The disposal value varies on the type of asset and the depreciation method used.

What happens if a business is disposed of assets?

A disposal can occur when the asset is scrapped and written off, sold for a profit to give a gain on disposal, or sold for a loss to give a loss on disposal. To illustrate suppose a business has long term assets that originally cost 9,000 which have been depreciated by 6,000 to the date of disposal.

How do you record a disposal?

The next component of the journal entry involves recording any cash received from the disposal. This is done by debiting the cash account. The amount recorded should be the actual cash received from the sale or disposal of the asset. If the machinery was sold for $25,000, the cash account would be debited by this amount.