Recording sales transactions properly is critical for any business. Sales journal entries track revenue generated and account for the cost of goods sold.

In this comprehensive guide we’ll walk through the entire process of making sales journal entries using examples. By the end you’ll understand exactly how to record these transactions in your books.

Let’s get started!

What is a Sales Journal Entry?

A sales journal entry records a sale of inventory or services to a customer. The entry typically includes

- Debit to accounts receivable or cash to record revenue

- Credit to sales revenue to increase income

- Credit to cost of goods sold to reduce inventory

Sales entries are important because they:

- Increase revenue in the income statement

- Reduce inventory assets on the balance sheet

- Generate an accounts receivable until cash is received

Below is an example of what a basic sales journal entry looks like:

Debit Accounts Receivable $100 Credit Sales Revenue $80Credit Cost of Goods Sold $20This records a $100 sale with $80 in revenue and $20 of inventory cost. Pretty simple!

Now let’s go through the full process step-by-step.

Step 1: Identify Relevant Account Information

Before recording a sale, you need to gather some key pieces of information:

- Sales invoice – This contains info like the transaction date, customer, items sold, quantities, and prices

- Inventory costs – Needed to calculate cost of goods sold

- Payment terms – Required to know if it’s a cash or credit sale

Having these data points handy will make the journal entry process smooth and accurate.

Step 2: Analyze the Transaction

Next, scrutinize the sales transaction to identify what accounts will be impacted:

- Revenue – Sales revenue will increase by the total sale amount.

- Receivable – If on credit, a receivable will be generated for the sales amount.

- Cash – If a cash sale, cash balance will increase by the sale amount.

- Cost of goods sold – Inventory will decrease by the item costs.

Making a quick T-account sketch can help visualize the accounts involved.

Step 3: Determine Debit and Credit Amounts

Now it’s time to calculate the specific debit and credit amounts for the entry.

- Sales revenue credit – This is the total sale price found on the sales invoice.

- COGS credit – Calculate by totaling the costs of inventory items sold.

- Debit – Will be the sales invoice total. Goes to either accounts receivable or cash.

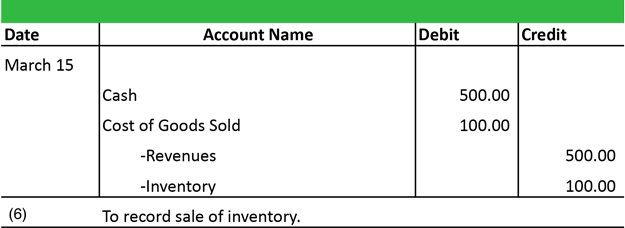

Let’s look at an example:

Sale Invoice Details

- 2 Chairs sold at $50 each = $100 total sale

- Cost of each chair is $20

Journal Entry Calculations

- Sales revenue credit = $100 (total sale)

- COGS credit = 2 x $20 = $40 (cost of inventory sold)

- Debit to accounts receivable = $100

This results in the following sales journal entry:

Debit Accounts Receivable $100Credit Sales Revenue $100 Credit COGS $40The debits and credits tie out at $100 each. Perfect!

Step 4: Record the Sales Journal Entry

We’ve gathered the information, analyzed the accounts, and calculated debits/credits. Now it’s time to officially log the entry into the accounting system.

Follow these steps:

-

Open your accounting software or journal. For manual entry, use a sales journal or general journal.

-

Enter the date of the sale transaction.

-

Record the accounts and amounts calculated in Step 3 using the debit and credit system.

-

Add a description like “Sale of 2 chairs to XYZ Company”.

-

Save the entry. It’s now safely logged!

Congratulations, you’ve successfully recorded a sales transaction. But we’re not done yet…

Step 5: Post to the General Ledger

Posting to the general ledger is the final step to ensure the sales entry permanently impacts your books.

Posting transfers the debit and credit amounts to update:

- Revenue and expense T-accounts in the income statement

- Asset and liability accounts on the balance sheet

This is a crucial step – without it, your financial statements won’t reflect the sale!

What About Cash Sales?

The above example shows a credit sale to accounts receivable. But what if it’s a cash sale instead?

The process is essentially the same, with one key difference:

- Debit cash instead of accounts receivable

Cash is an asset account, so the debit increases it, just like with receivables.

Below is an example cash sale journal entry:

Debit Cash $100 Credit Sales Revenue $100Credit Cost of Goods Sold $ 40 And that’s really all there is to it. The core accounts and amounts stay the same.

What About Sales Discounts?

Sometimes sales are made with discounts, such as:

- 2/10 net 30 – 2% discount if paid in 10 days, full amount due in 30 days

- $25 off for new customers

How do you record sales discounts in the journal entry?

When a discount is provided, you debit accounts receivable for the discounted amount. This is because that is the actual amount owed by the customer.

You would also credit sales discounts for the discount amount. This accounts for the lost revenue separately.

Below is an example:

Sale Info

- Total sales price: $1,000

- Payment terms: 2/10 net 30

- Customer takes the 2% discount

Journal Entry

Debit Accounts Receivable $980 Credit Sales Revenue $980Credit Sales Discounts $ 20 Credit COGS $500This records the net receivable, discounted revenue, and inventory cost correctly.

Sales Returns and Allowances

It’s also common for customers to return purchased inventory for various reasons, like:

- Defective or damaged goods

- Wrong items shipped

- Buyer’s remorse

These sales returns must also be recorded with journal entries.

When inventory is returned by a customer, you need to debit sales returns and:

- Credit accounts receivable – If they originally bought on credit

- Debit cash – If they originally paid with cash

You’ll also credit inventory to account for the returned stock.

Here’s an example journal entry for a credit sale return:

Debit Sales Returns $100 Credit Accounts Receivable $100 Credit Inventory $60This handles sales returns properly by reducing receivables and increasing inventory.

Summing Up Sales Journal Entries

Here are the key steps to master sales journal entries:

- Gather key details from the sales invoice and inventory costs

- Analyze the accounts impacted – revenue, A/R, cash, COGS

- Calculate debit and credit amounts

- Record the journal entry

- Post to the general ledger

Adjust for cash sales, discounts, and returns accordingly.

And that’s really all there is to it! Proper sales journal entry recording is vital for accurate financial statements.

Implement these steps now to start properly logging your company’s sales transactions. Your accounting books will thank you!

What is the Sales Journal Entry?

A sales journal entry records the revenue generated by the sale of goods or services. This journal entry needs to record three events, which are the recordation of a sale, the recordation of a reduction in the inventory that has been sold to the customer, and the recordation of a sales tax liability. The content of the entry differs, depending on whether the customer paid with cash or was extended credit. In the case of a cash sale, the entry is:

- [debit] Cash. Cash is increased, since the customer pays in cash at the point of sale.

- [debit] Cost of goods sold. An expense is incurred for the cost of goods sold, since goods or services have been transferred to the customer.

- [credit] Revenue. The revenue account is increased to record the sale.

- [credit]. Inventory. The inventory asset account is reduced to reflect the reduction of inventory caused by the sale, when goods are transferred to the customer.

- [credit] Sales tax liability. If a sales tax liability is created by the sale transaction, it is recorded at this time, and will later be eliminated when the sales tax is remitted to the government.

The layout of the journal entry for a cash sale is as follows:

If a customer was instead extended credit (to be paid later), the entry changes to the following:

- [debit] Accounts receivable. A receivable is created that will later be collected from the customer. This replaces the increase in cash noted in the preceding journal entry.

- [debit] Cost of goods sold. Same explanation as noted above.

- [credit] Revenue. Same explanation as noted above.

- [credit] Inventory. Same explanation as noted above.

- [credit] Sales tax liability. Same explanation as noted above.

The layout of the journal entry for a sale on credit is as follows:

Example of the Sales Journal Entry

As an example of a sales journal entry, a company completes a sale on credit for $1,000, with an associated 5% sales tax. The goods sold have a cost of $650. The sales journal entry is:

- [debit] Accounts receivable for $1,050

- [debit] Cost of goods sold for $650

- [credit] Revenue for $1,000

- [credit] Inventory for $650

- [credit] Sales tax liability for $50

Recording Transactions into a Sales Journal

How do I create a sales journal entry?

Sales journal entries should also reflect changes to accounts such as Cost of Goods Sold, Inventory, and Sales Tax Payable accounts. To create a sales journal entry, you must debit and credit the appropriate accounts. Your end debit balance should equal your end credit balance. As a refresher, debits and credits affect accounts in different ways.

What is a sales journal entry?

A sales journal entry is a bookkeeping record of any sale made to a customer. You use accounting entries to show that your customer paid you money and your revenue increased. These types of entries also show a record of an item leaving your inventory by moving your costs from the inventory account to the cost of goods sold account.

What should a sales journal entry look like?

Your credit sales journal entry should debit your Accounts Receivable account, which is the amount the customer has charged to their credit. And, you will credit your Sales Tax Payable and Revenue accounts. This is how the sales journal entry would look:

What is a sales journal double entry?

At the end of each accounting period (usually monthly), the sales journal double entry is used to update the general ledger accounts. As the business is using an accounts receivable control account in the general ledger, the postings are part of the double entry bookkeeping system.