Accounts receivable is the balance owed to a company resulting from selling goods or services on credit. It’s a current asset on the balance sheet that represents future cash inflows. To analyze accounts receivable efficiency, companies use ratios like accounts receivable turnover and days sales outstanding. These require calculating average net accounts receivable, a key metric derived from the balances over time.

Follow this step-by-step guide to accurately determine your business’s average net accounts receivable.

Step 1: Identify Accounts Receivable at the Beginning and End of the Period

The first step is identifying the accounts receivable balance at the beginning and end of the time period you are analyzing. This is usually the beginning and end of a fiscal year or quarter.

Locate these balances on your balance sheet. Accounts receivable is typically its own line item under current assets. Review balance sheets from the relevant periods to find the balances.

For example, if analyzing fiscal year 2022, you need accounts receivable as of December 31, 2021 and December 31, 2022.

Step 2: Subtract Any Allowances for Doubtful Accounts

Accounts receivable is reported on a gross basis, meaning it includes the full amounts owed without deducting uncollectible accounts. To get net accounts receivable subtract contra accounts like allowance for doubtful accounts or allowance for expected credit losses.

These contra accounts estimate uncollectible receivables based on historical nonpayment rates. Determine the allowances at the beginning and end of your period and deduct them from gross accounts receivable to derive net balances.

Step 3: Calculate the Average

With beginning and ending net accounts receivable identified, average them to find the mean balance for the period.

Add the starting and ending balances together then divide by 2

Average Net Accounts Receivable = (Beginning Net AR + Ending Net AR) / 2

This formula provides the average level of net accounts receivable maintained over your period of analysis.

Step 4: Adjust for Any Unusual Fluctuations

Examine the trend in accounts receivable over the full period. Look for any timing quirks or anomalies that distorted the average.

For example, if accounts receivable spiked mid-year due to a temporary system issue slowing collections, the balances around that blip may skew the average higher.

In such cases, you may want to calculate the average based on the more stable balances before and after the anomaly. This presents a more accurate picture of typical accounts receivable.

Use judgment to determine if any temporary spikes or dips merit adjusting the average balances used. The goal is measuring sustainable performance rather than distortions from temporary factors.

Step 5: Use the Average to Calculate Efficiency Ratios

With average net accounts receivable determined, incorporate it into key efficiency ratios to assess accounts receivable management:

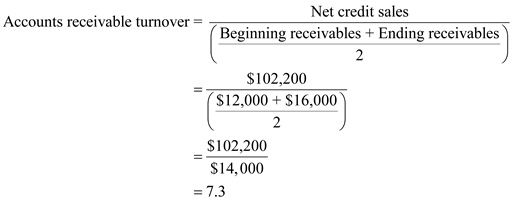

Accounts Receivable Turnover: This ratio measures how many times a company collects its average AR balance over a period.

Higher is better, as it shows faster AR collection. The formula is:

Accounts Receivable Turnover = Net Credit Sales / Average Net Accounts Receivable

Days Sales Outstanding: This shows the average number of days needed to collect AR balances. Lower is better, as it indicates shorter collection periods. The formula is:

Days Sales Outstanding = Average Net Accounts Receivable / (Net Credit Sales / 365 )

Comparing these ratios over time and to industry benchmarks reveals improvement or deterioration in managing accounts receivable. Trending the average AR balance itself also provides insights on working capital efficiency.

Step 6: Analyze the Results

With your ratios calculated, analyze the results to identify opportunities. Look at your accounts receivable turnover and days sales outstanding ratios over the last few years.

If the turnover is decreasing and days outstanding increasing, this indicates collection periods are lengthening. The company is taking longer to collect what it is owed. Dig deeper into reasons why and develop initiatives to reverse the trend.

Also compare your ratios to industry averages. Significantly lagging competitors signals accounts receivable management needs improvement. Use benchmarking to set goals around days outstanding and turnover.

Step 7: Implement Tactics to Improve Efficiency

Based on your analysis, implement changes to enhance accounts receivable efficiency. Here are some example tactics:

- Review credit policies to ensure proper vetting of customers

- Offer discounts for early payment

- Streamline invoicing procedures to avoid delays

- Invest in collector training on best practices

- Adopt collections software to automate follow-ups

- Outsource past due accounts to collection agencies

Continuously monitoring average accounts receivable and related ratios allows you to measure progress. Over time, an optimized approach can significantly improve working capital management.

Key Takeaways on Calculating Average Net Accounts Receivable

- Finding the average helps analyze performance by smoothing fluctuations over a period.

- Net accounts receivable excludes contra accounts like allowances for bad debts.

- Adjust averages to remove effects of temporary distortions or anomalies.

- Use the average net AR balance to calculate turnover and days outstanding.

- Compare ratios over time and to industry to identify collection issues.

- Implement process improvements and technology to enhance collections.

Carefully determining average net accounts receivable provides key insights into the effectiveness of your credit and collections processes. Assess trends, benchmark performance, and leverage the results to optimize working capital. With an efficient approach, you can shorten collection periods while also minimizing bad debt expenses.

Average of Consecutive Month-End Balances for Three Months

This calculation is based on the ending receivable balances in the past three months. It suffers from the same problems as using the balances at the end of the last two months, but probably also covers the full range of dates over which the typical company has receivables outstanding. Thus, this alternative tends to combine a realistic measurement time period and a relatively simple calculation.

Average of Consecutive Month-End Balances for Two Months

Perhaps the most common calculation for average accounts receivable is to sum the ending receivable balances for the past two months and divide by two. This approach may yield a somewhat high average receivable, since many companies issue a large number of invoices at month-end, but it at least covers the period over which receivables are currently outstanding.

Accounts Receivable Turnover Ratio

How do you calculate average net receivables?

To calculate average net receivables, add together the net receivables for the current period and the immediately preceding period, and then divide the sum by two. The formula is: (Net receivables for current period + Net receivables for preceding period) ÷ 2 = Average net receivables

How do I calculate net credit sales & average accounts receivable?

Net credit sales = Annual credit sales – (Sales returns + Sales allowances) You can find the numbers you need to plug into the formula on your annual income statement or balance sheet. Average accounts receivable is used to calculate the average amount of your outstanding invoices paid over a specific period of time.

How do you calculate account receivable turnover?

Divide by the average net accounts: Once you know your net credit sales, divide the amount by the average net accounts receivable to find your account receivable turnover.

How do you calculate accounts receivable ratio?

Accounts receivable ratio = $400,000 / $35,000 = 11.43 To determine the average number of days it took to get invoices paid, you must divide the number of days per year, 365, by the accounts receivable turnover ratio of 11.4.