Material price variance is an important metric that measures the difference between the actual price paid for materials and the standard price that was budgeted. Tracking and evaluating material price variance allows companies to monitor spending and quickly identify any issues with materials procurement. This article will explain what material price variance is how to calculate it and how to use variance analysis to evaluate performance and make improvements.

What is Material Price Variance?

Material price variance measures the difference between the actual price paid for materials and the standard or budgeted price. The materials referred to are direct materials that can be traced directly to products, such as fabric used to make clothes or cocoa used to make chocolate.

The standard price is the estimated or expected price per unit that is set during the budgeting process, before production takes place. The actual price is the real amount per unit that is paid when materials are procured.

A positive material price variance means the actual price was higher than the standard, This is considered unfavorable because it indicates spending was higher than planned A negative variance means the actual price was lower than expected This favorable outcome shows money was saved on materials,

Why Calculate Material Price Variance?

Tracking material price variance is an important component of standard costing and variance analysis. Here are some key reasons companies monitor this metric:

-

Measure performance: The material price variance reveals how closely material costs aligned with the target budget. Significant deviations may indicate an issue with the procurement process.

-

Identify issues promptly: By calculating the variance frequently (e.g. weekly, monthly), problematic trends can be spotted early. Action can be taken before major losses occur.

-

Influence future plans The insights gained from variance analysis can inform future budgeting and performance goals. For example, if material prices are consistently higher than expected, the standard price can be adjusted upwards

-

Assess suppliers: The variance may identify vendors that are overcharging. This could prompt negotiations for better deals or changing suppliers altogether.

-

Evaluate buyers: Large unfavorable variances could indicate that the purchasing department needs to negotiate better prices or find alternative vendors.

How to Calculate Material Price Variance

The general formula to calculate material price variance is:

(Actual Quantity Purchased x Actual Price) – (Actual Quantity Purchased x Standard Price)

The steps to determine the material price variance are:

-

Identify the actual quantity of materials purchased for production. This is the total volume bought, for example, 5,000 yards of fabric.

-

Note the actual price paid per unit of material. For instance, fabric cost $4 per yard.

-

Multiply the actual quantity by the actual price to get the total actual material cost. In the example, this is 5,000 yards x $4 = $20,000.

-

Identify the standard price per unit that was budgeted. For example, $3.50 per yard.

-

Multiply the actual quantity by the standard price to get the total standard material cost. In the example, this is 5,000 yards x $3.50 = $17,500.

-

Take the total actual material cost and subtract the total standard cost to find the variance. In the example:

- Total actual cost = $20,000

- Total standard cost = $17,500

- Variance = $20,000 – $17,500 = $2,500 (unfavorable)

This unfavorable variance of $2,500 indicates the actual spending on materials exceeded the budget by that amount.

Evaluating Material Price Variance

Once the material price variance has been calculated, companies can analyze the results to identify potential causes and develop solutions.

Causes of Unfavorable Variance

An unfavorable material price variance means the business paid more for materials than planned. Some possible reasons include:

- Incorrect standard price: The budgeted rate was too low.

- Increase in market prices: Input costs went up across the industry.

- Ineffective negotiations: The purchasing agent failed to bargain for discounts.

- Order urgency: A rush order meant paying a premium.

- Supplier issues: The vendor raised prices unexpectedly.

Causes of Favorable Variance

A favorable material price variance indicates materials were purchased below budget. Some potential causes:

- Conservative standard price: The estimated rate was too high.

- Decrease in market prices: Input costs fell across the sector.

- Successful negotiations: The buyer bargained for lower prices.

- Volume discounts: Buying in bulk led to cost savings.

- Supplier issues: The vendor reduced prices.

Improvement Strategies

After identifying the root causes, steps can be taken to improve performance:

- Revise standards to be more accurate and realistic.

- Provide negotiation training to the purchasing team.

- Build relationships with vendors to negotiate prices.

- Change suppliers if necessary to reduce costs.

- Alter production schedules to avoid rush orders.

- Automate parts of the procurement process for efficiency.

Material Price Variance Example

Let’s look at an example to illustrate how to calculate and evaluate material price variance:

Kraft Foods budgeted a standard price of $2.00 per pound of cocoa for a production run of 25,000 pounds. However, the purchasing department paid an actual price of $2.25 per pound.

The material price variance is:

- Actual quantity purchased: 25,000 pounds

- Actual price: $2.25 per pound

- Total actual cost = 25,000 x $2.25 = $56,250

- Standard price: $2.00 per pound

- Total standard cost = 25,000 x $2.00 = $50,000

- Variance = $56,250 – $50,000 = $6,250 (unfavorable)

This large unfavorable variance indicates Kraft paid much more for cocoa than planned in the budget. Further analysis found the standard rate was set too conservatively. Also, an unexpected rise in cocoa prices due to poor harvests drove up costs across the entire chocolate industry.

Kraft decided to increase the standard price to $2.20 per pound in next year’s budget to account for likely market price increases. They also plan to negotiate fixed price contracts with suppliers whenever possible.

Key Takeaways

- Material price variance measures the difference between the actual and standard cost of direct materials. A positive variance is unfavorable, while a negative variance is favorable.

- Tracking this metric allows companies to identify issues promptly and take corrective action. It is a key aspect of variance analysis and standard costing.

- The variance is calculated by taking the total actual material cost and subtracting the total standard cost based on actual usage and planned rates.

- The results should be analyzed to determine the potential causes and develop strategies for improvement.

- Calculating, evaluating, and responding to material price variances can help optimize spending and improve operational performance.

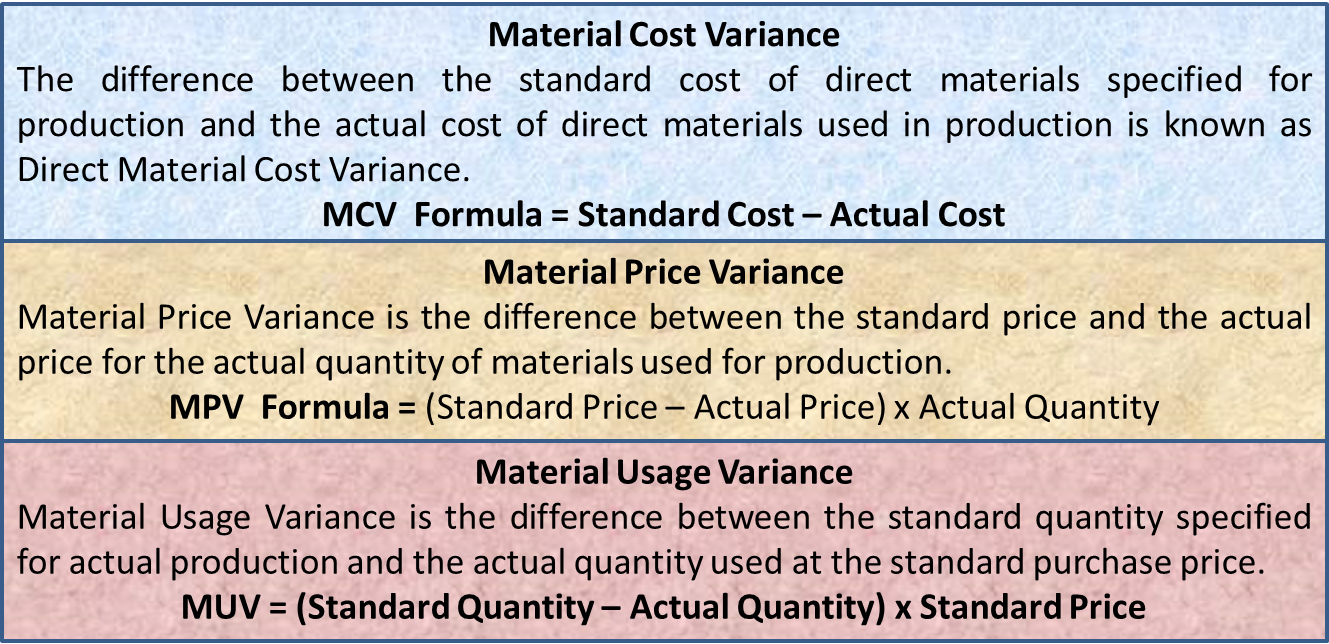

What is the Materials Price Variance?

The materials price variance is the difference between the actual and budgeted cost to acquire materials, multiplied by the total number of units purchased. The variance is used to spot instances in which a business may be overpaying for raw materials and components. However, it is only useful if the budgeted cost in the calculation has a reasonable basis.

Understanding the Materials Price Variance

The key part of the materials price variance calculation is the standard price, which is decided upon by the engineering and purchasing departments, based on estimates of usage, probable scrap levels, required quality, likely purchasing quantities, and several other factors. Politics can enter into the standard-setting decision, which means that standards may be set so high that it is quite easy to acquire materials at prices less than the standard, resulting in a favorable variance. Thus, the decision-making process that goes into the creation of a standard price plays a large role in the amount of materials price variance that a company reports.

Material Price Variance | Explained with Examples

How do you calculate material price variance?

You can calculate material price variance with this formula: Material price variance = quantity of materials used x (budgeted price per unit of materials − actual price per unit of materials) Related: What Is Basic Accounting? Here’s a process you can use to calculate material price variance: 1. Determine the quantity of product used

How do you calculate direct materials quantity variance?

The direct materials quantity variance compares the actual quantity of materials used to the standard materials that were expected to be used to make the actual units produced. The variance is calculated using this formula: Direct Materials Quantity Variance = (Actual Quantity Used × Standard Price ) − (Standard Quantity × Standard Price)

What is materials price variance?

Materials price variance represents the difference between the standard cost of the actual quantity purchased and the actual cost of these materials. Although materials price variance may not be controllable, it provides management with important information for planning and decision-making purposes.

How do you calculate direct materials price variation?

Direct Materials Price Variance = (Actual Price per Unit of Materials − Standard Price per Unit of Materials) × Actual Quantity of Materials Used With either of these formulas, the actual quantity used refers to the actual amount of materials used to create one unit of product. The standard price is the expected price paid for materials per unit.