Many or all of the products featured here are from our partners who compensate us. This influences which products we write about and where and how the product appears on a page. However, this does not influence our evaluations. Our opinions are our own. Here is a list of our partners and heres how we make money.

The investing information provided on this page is for educational purposes only. NerdWallet, Inc. does not offer advisory or brokerage services, nor does it recommend or advise investors to buy or sell particular stocks, securities or other investments.

As you start learning about where and how to invest and begin researching brokerage accounts, its easy to overlook one thing: brokerage and investment fees.Advertisement

Opening a brokerage account is an exciting first step towards building your investment portfolio. As you start trading stocks, bonds, mutual funds, and other securities you’ll inevitably encounter various brokerage fees. While these costs may seem small they can seriously eat into your long-term returns if left unchecked.

In this comprehensive guide, I’ll explain the most common brokerage fees, how they work, and some smart strategies to reduce your investing costs My goal is to empower you to make informed decisions, so you can keep more of your hard-earned money working for you

What Are Brokerage Fees?

In short, brokerage fees are charges levied by your broker for various services related to your investment account.

Here are some examples of common brokerage fees:

-

Commissions Also called trading fees. This is a charge paid when you buy or sell a stock exchange-traded fund (ETF) option contract, or other security. Commissions are usually quoted per trade.

-

Account maintenance fees: An annual or monthly fee just for having an account open. This covers costs for statement processing, account reporting, and customer service.

-

Transfer fees: A fee to move your account from one broker to another. Brokers often charge $50-$100 for this service.

-

Inactive account fees: Charges levied if you don’t execute a certain number of trades within a certain timeframe. Typically $10-$30 per quarter.

-

Margin interest: Interest charged for borrowing money from your broker to purchase securities. The rate varies based on market factors.

-

Miscellaneous fees: Things like wire transfer charges, paper statement fees, overnight check delivery fees, and more. These vary widely between brokers.

As you can see, brokerages have all kinds of ways to generate revenue from your account. While some fees are unavoidable, the key is minimizing expenses wherever possible. Even small fees can seriously eat into your long-term investment gains.

Commissions and Trading Costs

For stock traders, commissions are typically the biggest brokerage fee. In the past, commissions were quite expensive, often $5-$10 or more per trade. This created a barrier for smaller investors.

Fortunately, trading technology has improved drastically over the past decades. The rise of electronic trading and automation has driven commission costs down significantly.

Here’s a quick history lesson:

-

1975: The NYSE deregulates fixed commission rates, allowing discounts for larger traders. Rates remained expensive for small investors.

-

Mid 1990s: Online brokers like E*TRADE, Ameritrade, and Charles Schwab enter the scene, competing heavily on price. Commissions decline to around $20 per trade.

-

Early 2000s: Advances in technology drive commissions below $10 at leading online brokers.

-

2019: Major brokers drop commissions to $0 on stocks and ETFs, initiating the zero-commission trading revolution.

Today, most large brokerages offer commission-free stock and ETF trading. This levels the playing field for all investors, not just high rollers.

However, some niche brokers still charge commissions, usually $5-$10 per trade. For active traders, these fees can really add up. Be sure to calculate the total commission costs based on your expected trade volume before choosing a broker.

Mutual Fund Fees and Expenses

Beyond trading fees, mutual funds and ETFs carry built-in operating costs through their expense ratios. This covers things like portfolio management, administrative costs, marketing, and shareholder services.

Expense ratios are charged annually as a percentage of your assets. For example, a fund with a 0.50% expense ratio charged to a $10,000 investment would cost $50 per year.

While this may seem small, it really adds up over decades of compound growth. Let’s take a look at the impact of expense ratios on a hypothetical $100,000 investment over 30 years, assuming a 6% annual return:

- 0.10% expense ratio: Ending portfolio value = $324,340

- 0.50% expense ratio: Ending portfolio value = $295,595

- 1.00% expense ratio: Ending portfolio value = $267,275

As you can see, the portfolio with the lowest fees grew over $28,000 larger! This highlights why minimizing fund expenses can be so impactful long-term.

When selecting funds, make sure to research the expense ratios and choose passively managed index funds when possible. Actively managed funds tend to have drastically higher expense ratios, often around 1% or more.

401(k) Administration Fees

For those contributing to a 401(k) or other employer-sponsored retirement plan, be aware of administration costs charged to participants.

Plan administration fees typically cover:

- Recordkeeping

- Compliance services

- Trustee services

- Accounting

- Legal expenses

- Communications and education

- Investment selection/monitoring

Often these fees are bundled into a single “investment management” or “administration” fee listed on your statement. Total plan costs are usually in the 0.30% – 1.50% range annually.

Ideally, your employer covers these fees so you don’t pay anything extra. However, about half of plans pass on some or all of the administration costs to employees.

If your plan is charging you over 1% annually in administration fees, consider lobbying your employer for lower-cost alternatives. Another option is to contribute only enough to get the company match, then fund an IRA for additional retirement savings. This avoids excessive 401(k) fees.

How Brokerages Make Money

At the end of the day, brokerages are businesses seeking to maximize profits. Beyond the fees we’ve covered, brokers generate revenue through:

-

Interest on cash balances: Brokerages invest your idle cash and keep some of the interest. Make sure to keep only necessary minimum balances to avoid missed investment gains.

-

Payment for order flow (PFOF): Brokers receive compensation for routing customer orders through specific market makers. This can create conflicts of interest.

-

Margin lending: Brokers profit from lending money to clients for leveraged trading. The interest rate is usually 1-2% above current fed rates.

-

Securities lending: Brokers can lend your invested securities to other institutions for short periods. A portion of the lending income may be shared with your account.

-

Sweep accounts: Idle cash is swept into an FDIC-insured bank account or money market fund. The brokerage profits from net interest/yields earned on aggregate sweeps.

The moral is that brokers have incentives to generate more revenue from your account. Stay vigilant for unnecessary charges or mediocre default options that benefit the broker over your bottom line.

Strategies to Reduce Investment Fees

Now that you understand the various brokerage fees, here are some tips to minimize expenses:

-

Choose a low-cost broker: Look for a reputable broker that offers $0 stock/ETF trades, no account minimums or maintenance fees, and great customer service.

-

Use commission-free ETFs: Most brokers offer specific ETFs that can be traded without any commission. Build your portfolio using these funds whenever possible.

-

Opt for index funds: Passively managed index funds have significantly lower expense ratios than actively managed funds. This saves you money every year.

-

Consolidate accounts: Having all your investments at one broker allows you to more easily qualify for lower asset tiers, reducing management expenses.

-

Turn off margin: Don’t pay unnecessary margin interest by keeping a cash-only account. Margin can also encourage risky overtrading behavior.

-

Set up electronic statements: Avoid $1-$2 paper statement fees and get real-time online access instead.

-

Sign up for a dividend reinvestment plan (DRIP): This lets you reinvest dividends without paying commissions on the purchases.

-

Negotiate lower fees: Don’t be afraid to call your broker and negotiate lower fees if you’re a high-value customer. Oftentimes they’ll reduce or remove certain fees to retain your business.

The Bottom Line

While the various brokerage fees may seem perplexing at first, a little research goes a long way. Focus on minimizing expenses through a low-cost broker, index funds, commission-free trading, and more.

Over the decades, small reductions in your fees could add tens of thousands to your bottom line. It’s worth the effort to keep more money compounding in your favor.

At the end of the day, the key is understanding exactly what you’re paying for as an investor. Armed with knowledge, you can make informed choices to keep your hard-earned capital working harder for you. Here’s to many years of successful investing ahead!

Investment fee calculator

Use the investment fee calculator below to see how investment and brokerage fees could eat into your returns over time.

» Looking to pay less in broker fees? See NerdWallets picks for the best brokers

Expense ratios

Expense ratios are charged by mutual funds, index funds and ETFs. They’re shown as a percentage of your investment and charged as an annual fee: A fund that has an expense ratio of 0.10%, for example, means that you pay $1 per year for every $1,000 invested.

The expense ratio is designed to cover operating costs, including management and administrative costs. Funds that are actively managed — employing a professional to buy and sell its investments — typically carry higher expenses than index funds and ETFs, which are passively managed and track a stock market index, like the S&P 500. The goal of a manager is to try to beat the market; in reality, they rarely do.

» Learn more: Investing in ETFs and index funds

The expense ratio on an actively managed mutual fund might be 1% or more; on an index fund, it could be less than 0.25%. That’s a big difference, so you should pay careful attention to expense ratios when selecting your funds, and opt for low-cost index funds and ETFs when available.

The expense ratio also includes the 12B-1 fee, an annual marketing and distribution fee, if applicable. Remember the mention above, about how mutual fund companies can pay a broker to offer their funds with no transaction fee? If that cost is passed on to the investor, it will be as part of the 12B-1 fee. 12B-1 fees are part of the total expense ratio, not in addition to it, but it’s still important to know what you’re paying.

Where to find details: On the fund’s page on your broker’s website, in the expenses or fee table in the fund’s prospectus, or on an independent research website like Morningstar.com. Here’s an example of a prospectus fee table, from the Fidelity Freedom 2055 target-date fund:

Brokerage Fees: What You Need to Know

FAQ

What is a good brokerage fee?

|

Brokerage fee

|

Typical cost

|

|

Annual fees

|

$50 to $75 per year

|

|

Inactivity fees

|

May be assessed on a monthly, quarterly or yearly basis, totaling $50 to $200 a year or more

|

|

Research and data subscriptions

|

$1 to $30 per month

|

|

Trading platform fees

|

$50 to more than $200 per month

|

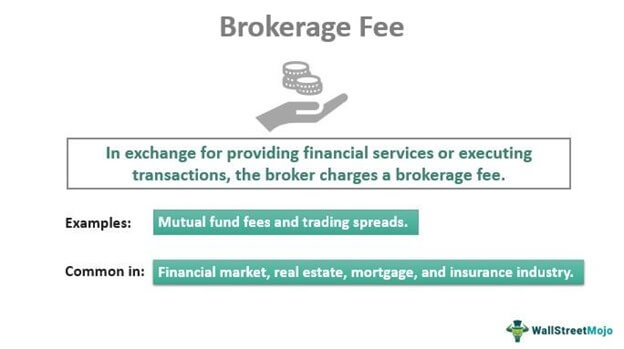

What is a brokerage fee?

Brokerage fees, also known as broker fees, are based on a percentage of the transaction, as a flat fee, or as a hybrid of the two. Brokerage fees vary according to the industry and type of broker. In the real estate industry, a brokerage fee is typically a flat fee or a standard percentage charged to the buyer, the seller, or both.

Are brokerage fees a cost of investing?

Commissions are the best-known type of brokerage fee you might encounter, but they certainly aren’t the only cost of investing you should keep in mind. Here are some of the charges a broker may have. Virtually all brokers have eliminated commissions for online stock trades, but there are still investment commissions to keep in mind.

Should you pay brokerage fees?

Some even charge maintenance and inactivity fees, but generally, you can avoid paying these brokerage fees with the right broker. Finding the right broker can make a huge difference in the long-term; fees can seriously eat into your investment returns.

How much does a real estate broker charge?

Brokerage fees vary according to the industry and type of broker. In the real estate industry, a brokerage fee is typically a flat fee or a standard percentage charged to the buyer, the seller, or both. Mortgage brokers help potential borrowers find and secure mortgage loans; their associated fees are between 1% and 2% of the loan amount.