The general ledger and trial balance are two of the most fundamental reports that form the bedrock of the accounting system But the specific purposes and uses of each one are often confused.

Understanding the key differences between the general ledger and trial balance is critical for proper financial management and reporting. Let’s examine how these foundational accounting tools differ across several dimensions.

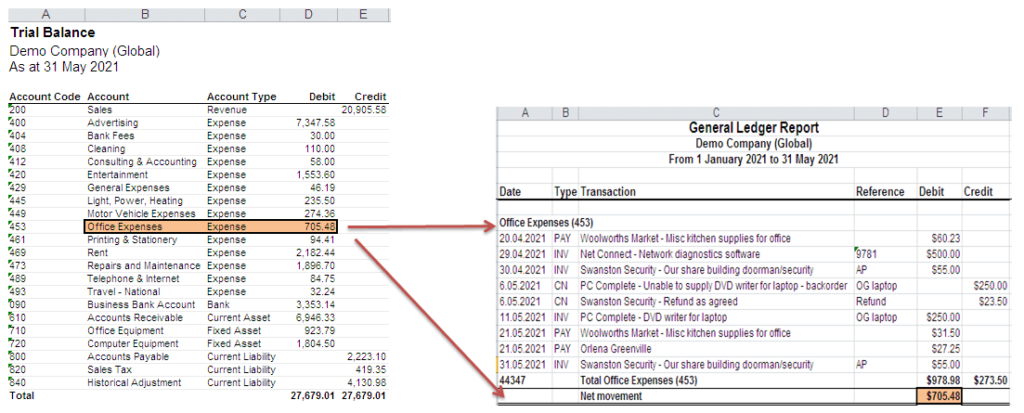

Overview of the General Ledger

The general ledger contains detailed entries for every transaction that occurs within a business. It provides a comprehensive record of all debits and credits made to individual accounts over a set time period.

Some key attributes of the general ledger

- Chronological listing of all journal entries

- Used to aggregate activities by account type

- Tracks detailed transactions across multiple sub-ledgers

- Maintains debit and credit balances for all accounts

- Primary data source for financial statements

- Can contain thousands of entries

- Updated continuously in real-time

- Managed through accounting/ERP software

The general ledger accumulates transaction data from sources like the sales ledger, purchase ledger, cash ledger, and payroll ledger. It also incorporates journal entries for adjustments, accruals, deferrals, and closing entries.

Overview of the Trial Balance

The trial balance is a summary report generated from general ledger account balances at the end of a period. It lists each account name and ending balance in debit and credit columns.

Key attributes of the trial balance include:

- Extracted directly from the general ledger

- Snapshot of balances in all ledger accounts

- Produced at end of accounting cycle or fiscal year

- Used to validate that debits equal credits

- Signals no journal entry errors if balances match

- Foundation for drafting financial statements

- Typically 1-2 pages long

- Reflects activity over a set time interval

- Unadjusted vs. adjusted versions

The trial balance ensures entries have been properly journalized and posted to the ledger without error. If debits and credits match, it confirms the books are in balance prior to financial reporting.

The Key Differences Between the Ledger and Trial Balance

Now that we’ve defined the general ledger and trial balance independently, let’s directly compare them across several dimensions:

1. Data Volume

- General ledger contains large volumes of granular transaction details

- Trial balance shows only the net debit or credit balance per account

2. Frequency of Use

- General ledger is accessed constantly for transaction tracking

- Trial balance is generated periodically at end of reporting cycle

3. Purpose

- General ledger is the permanent detailed transaction record

- Trial balance validates account balances are in equilibrium

4. Account Information

- General ledger has extensive metadata like sub-accounts

- Trial balance contains only account names and balances

5. Span of Coverage

- General ledger accumulates transactions for any time interval

- Trial balance shows activity for a discrete reporting period

6. Adjustments

- General ledger incorporates all adjusting entries

- Trial balance reflects adjustments only at time generated

7. Auditing Use

- Auditors verify source data against general ledger entries

- Auditors check total equality of the trial balance

8. Reporting Basis

- General ledger managed on cash or accrual basis

- Trial balance reflects accounting basis used

9. Underlying Detail

- General ledger stores granular transaction line items

- Trial balance rolls up to total account balances

10. Volume of Data

- General ledger contains every journal entry

- Trial balance fits on 1-2 pages for most entities

| Factor | General Ledger | Trial Balance |

|---|---|---|

| Data volume | Very large | Condensed |

| Frequency of use | Constant | Periodic |

| Purpose | Permanent detailed transaction record | Validate account balances in equilibrium |

| Account information | Extensive metadata and sub-accounts | Only names and balances |

| Time span | Any interval | Discrete reporting period |

| Adjustments | Includes all | Only at time generated |

| Auditing use | Verify detailed transactions | Check total balance equality |

| Reporting basis | Cash or accrual methods | Reflects basis used |

| Underlying detail | Granular line items | Rolled up totals by account |

| Data volume | Every transaction | Summary totals on 1-2 pages |

Walkthrough of the Ledger and Trial Balance Process

Let’s walk through a simplified example to better understand how the general ledger and trial balance interact in practice:

-

Company XYZ records 100 transactions in the general ledger during August.

-

On August 31, the accountant generates an unadjusted trial balance from the ledger.

-

The total debits equal total credits, confirming the ledger is in balance.

-

In September, the accountant records accrual, deferral, and other adjusting entries in the general ledger to comply with GAAP.

-

On September 10, an adjusted trial balance is created including those adjustments. Again, it balances.

-

The accountant uses the adjusted trial balance totals to prepare XYZ’s financial statements for the month ending August 31.

This example shows how the general ledger provides the detailed backdrop for summary trial balance reports used in financial statement preparation.

While they sound similar in name, the general ledger and trial balance serve very different purposes in the accounting workflow. The general ledger is the data repository, while the trial balance is an output used to validate ledger integrity.

Best Practices and Controls for Ledgers and Trial Balances

Maintaining accurate general ledgers and balanced trial balances is essential for reliable financial reporting. Consider these best practices for each:

For General Ledgers:

-

Enforce proper authorization and documentation for all journal entries

-

Integrate control accounts and subsidiary ledgers

-

Perform account reconciliations and verify ledger balances

-

Institute approval workflows for non-routine adjustments

-

Protect ledger access to authorized accounting staff only

-

Back up ledger data daily and store offsite

-

Leverage automation and accounting systems to minimize manual errors

For Trial Balances:

-

Generate both unadjusted and adjusted trial balances

-

Ensure debits and credits match by examining balances

-

Produce separate trial balances for reporting entities and segments

-

Have different accountants prepare and review for segregation

-

Investigate any account discrepancies immediately

-

Document evidence of preparation and manager approval

-

Check totals against prior periods for reasonableness

-

Use trial balances to substantiate financial statement figures

Adhering to these controls preserves the integrity of both the general ledger and resulting trial balances. Reliable account records also facilitate audits and operational decisions based on financial position and performance.

How Technology Is Transforming Ledgers and Trial Balances

Today’s accounting platforms and ERP systems enable the automated creation of general ledgers and trial balances. Benefits include:

- Reduced manual work and human error risks

- Seamless data flows between transaction processing and reporting

- Customizable dashboards for real-time visibility into balances

- Automatic trial balance generation with balancing validations

- Simplified audit preparation and analytics

- Enhanced controls through system workflows and data access restrictions

- Scalability across multiple entities, subsidiaries, and global locations

- Automated reconciliation of sub-ledger data to the general ledger

By harnessing technology to streamline production and analysis of general ledgers and trial balances, finance teams can focus on higher value initiatives while still maintaining accuracy.

Key Takeaways on the Ledger vs. Trial Balance

-

The general ledger chronologically stores granular transactions while the trial balance shows summarized account balances at a point in time.

-

General ledgers are accessed constantly while trial balances are generated periodically after closing.

-

Ledgers contain detailed metadata, adjustments, and sub-accounts while trial balances list only names and debit/credit totals.

-

Ledgers span any time interval and trial balances cover discrete reporting periods.

-

Ledgers are the data source while trial balances validate their integrity before financial statement generation.

-

New systems automate the creation and reconciliation of general ledgers and trial balances, saving time while reducing risk.

Understanding the unique role and utility of the general ledger vs. trial balance allows accounting teams to properly maintain transaction records, verify their accuracy, and derive reliable conclusions based on the data.

What is a General Ledger?

A general ledger is the master set of accounts that summarize all transactions occurring within an entity. The general ledger is comprised of all the individual accounts needed to record the assets, liabilities, equity, revenue, expense, gain, and loss transactions of a business.

What is a Trial Balance?

The trial balance is a report run at the end of an accounting period, listing the ending balance in each general ledger account. The report is primarily used to ensure that the total of all debits equals the total of all credits, which means that there are no unbalanced journal entries in the accounting system that would make it impossible to generate accurate financial statements. The initial trial balance that is run at the end of an accounting period is called the unadjusted trial balance. This report is nearly always adjusted with a variety of adjusting entries that are used to bring a company’s accounting records into compliance with the applicable accounting framework (such as GAAP); this is called the adjusted trial balance.

What is a general ledger

What is the difference between general ledger and trial balance?

Time Period: General Ledger records transactions during the accounting year of the organization for any period, whereas the trial balance is generally prepared on the final day of the accounting year. For investor use: Trial Balance is widely used by an investor for a study if they want to put money in company shares.

What is a trial balance?

This is an internal document used for accounting and auditing. There are three types of trial balance, including: Unadjusted trial balance: This is the listing of general ledger account balances at the end of the reporting period. Adjusted trial balance: This is the internal document that summarizes the current balances of the general ledger.

What is an unadjusted trial balance?

Unadjusted trial balance: This is the listing of general ledger account balances at the end of the reporting period. Adjusted trial balance: This is the internal document that summarizes the current balances of the general ledger. Post-closing trial balance: This is the final trial balance that’s prepared before a new accounting period starts.

What is a general ledger in accounting?

A general ledger is the master set of that summarize all occurring within an entity. The general ledger is comprised of all the individual accounts needed to record the , , , , , , and transactions of a business. What is a Trial Balance? The is a report run at the end of an accounting period, listing the ending balance in each account.