Net working capital is an important financial metric that measures a company’s liquidity and short-term financial health It indicates whether a business has enough current assets to cover its current liabilities and fund its day-to-day operations.

Calculating net working capital is straightforward once you understand the formula and what goes into it. This comprehensive guide will walk you through the step-by-step process of determining a company’s net working capital.

What is Net Working Capital?

Net working capital (NWC) refers to a company’s current assets minus its current liabilities. It is essentially the liquid capital available to fund the company’s regular business operations and growth.

Positive net working capital means the company’s current assets exceed its liabilities, indicating good short-term financial health. Negative net working capital occurs when liabilities are greater than assets, suggesting potential liquidity issues.

Net working capital differs from working capital in that it excludes cash and debt from the calculation. The goal is to measure operational liquidity by looking at the most liquid assets versus short-term obligations.

Why Net Working Capital Matters

Net working capital provides insight into a company’s:

-

Liquidity – Does it have enough resources to pay current debts? Can it respond to unexpected needs or opportunities?

-

Operational efficiency – How effectively is it managing inventory, credit, and debt?

-

Short-term financial health – Does it have the assets to continue daily operations and grow?

Positive net working capital means a company can support its ongoing activities and has reserves to handle financial stress. Negative net working capital suggests looming troubles in paying bills and demands.

Lenders and investors often look at net working capital to assess risk and management effectiveness. It offers an early warning of potential insolvency issues.

How to Calculate Net Working Capital

Net working capital uses accounts from the balance sheet. There are two main formulas:

1. Current Assets – Current Liabilities

This includes all current accounts on the balance sheet.

Net Working Capital = Current Assets – Current Liabilities

2. Operating Current Assets – Operating Current Liabilities

This excludes cash and short-term debt for a pure operational view.

Net Working Capital = (Current Assets – Cash) – (Current Liabilities – Short-Term Debt)

Or more simply:

Net Working Capital = Accounts Receivable + Inventory – Accounts Payable

Let’s look at the steps to calculate net working capital both ways.

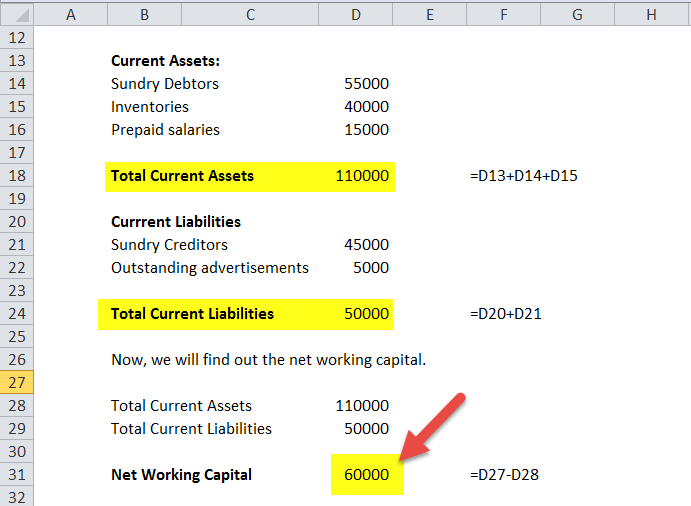

Step 1: Determine Current Assets

Current assets are balances that can be converted into cash within a year. Common accounts are:

- Cash and cash equivalents

- Marketable securities

- Accounts receivable

- Inventory

- Prepaid expenses

- Other liquid assets

Add up all current asset accounts on the balance sheet. This is total current assets.

Step 2: Determine Current Liabilities

Current liabilities are obligations due within one year. Typical accounts are:

- Accounts payable

- Short-term debt

- Current portion of long-term debt

- Accrued expenses

- Dividends payable

- Unearned revenue

- Other payables

Total all current liability accounts on the balance sheet. This gives total current liabilities.

Step 3: Subtract Current Liabilities from Current Assets

Take total current assets and subtract total current liabilities. The difference is the net working capital amount.

Net Working Capital = Total Current Assets – Total Current Liabilities

A positive result means current assets exceed liabilities. A negative amount indicates liabilities are greater than assets.

Step 4: Exclude Cash and Debt for Operational Net Working Capital

To exclude financing activities, subtract cash from current assets. Then subtract short-term debt accounts from current liabilities.

The new formula is:

Net Working Capital = (Current Assets – Cash) – (Current Liabilities – Short-Term Debt)

This gives a pure operational view based on accounts receivable, inventory, and accounts payable.

Real World Example

Let’s look at a quick example to see net working capital in action.

Company A has:

- Cash: $5,000

- Accounts Receivable: $10,000

- Inventory: $20,000

- Other Current Assets: $5,000

- Accounts Payable: $7,000

- Accrued Expenses: $4,000

- Short-Term Debt: $5,000

- Other Current Liabilities: $1,000

Current Assets:

Cash: $5,000

Accounts Receivable: $10,000

Inventory: $20,000

Other Current Assets: $5,000

Total Current Assets: $40,000

Current Liabilities:

Accounts Payable: $7,000

Accrued Expenses: $4,000

Short-Term Debt: $5,000

Other Current Liabilities: $1,000

Total Current Liabilities: $17,000

Net Working Capital = Current Assets – Current Liabilities

Net Working Capital = $40,000 – $17,000 = $23,000

This positive net working capital of $23,000 indicates good short-term financial health.

Excluding cash and debt:

Net Working Capital = (Current Assets – Cash) – (Current Liabilities – Short-Term Debt)

Net Working Capital = ($40,000 – $5,000) – ($17,000 – $5,000) = $23,000

The net working capital amount remains $23,000, showing operational liquidity.

Limitations of Net Working Capital

While useful, some limitations exist:

- Values change frequently

- Doesn’t account for asset quality

- Assets may lose value

- Missing liabilities can distort figures

- High working capital could mean excess inventory or underuse of credit

- Difficult to compare across industries

Net working capital is most effective when:

- Used consistently over time

- Combined with other metrics like revenue trends and profitability

- Evaluated based on the company and industry lifecycle stage

Net Working Capital Improves Decision Making

Calculating net working capital provides vital insights into a company’s short-term financial position and ability to fund growth. Monitoring it over time helps identify developing issues and opportunities.

With this easy-to-use guide, you can now determine a company’s net working capital. Use this important metric to assess financial health and make smart management decisions.

Why Is Working Capital Important?

Working capital is important because it is necessary for businesses to remain solvent. In theory, a business could become bankrupt even if it is profitable. After all, a business cannot rely on paper profits to pay its bills—those bills need to be paid in cash readily in hand. Say a company has accumulated $1 million in cash due to its previous years’ retained earnings. If the company were to invest all $1 million at once, it could find itself with insufficient current assets to pay for its current liabilities.

Working Capital Formula

To calculate working capital, subtract a companys current liabilities from its current assets. Both figures can be found in the publicly disclosed financial statements for public companies, though this information may not be readily available for private companies.

Working Capital = Current Assets – Current Liabilities

Working capital is often stated as a dollar figure. For example, say a company has $100,000 of current assets and $30,000 of current liabilities. The company is therefore said to have $70,000 of working capital. This means the company has $70,000 at its disposal in the short term if it needs to raise money for a specific reason.

When a working capital calculation is positive, this means the companys current assets are greater than its current liabilities. The company has more than enough resources to cover its short-term debt, and there is residual cash should all current assets be liquidated to pay this debt.

When a working capital calculation is negative, this means the companys current assets are not enough to pay for all of its current liabilities. The company has more short-term debt than it has short-term resources. Negative working capital is an indicator of poor short-term health, low liquidity, and potential problems paying its debt obligations as they become due.

It is worth noting that negative working capital is not always a bad thing; it can be good or bad, depending on the specific business and its stage in its lifecycle; however, prolonged negative working capital can be problematic.

Net Working Capital

FAQ

What is the formula for calculating net working capital?

What is the formula for net net working capital?

How to calculate NWC ratio?

How do you calculate net working capital (NWC)?

The formula to calculate net working capital (NWC) subtracts operating current liabilities from operating current assets. A positive NWC value implies the company can pay off its short-term obligations by liquidating its current assets, while a negative NWC signals potential near-term insolvency risk.

What is working capital & how does it work?

What Is Working Capital? Working capital, also known as net working capital (NWC), is the difference between a company’s current assets —such as cash, accounts receivable/customers’ unpaid bills, and inventories of raw materials and finished goods—and its current liabilities, such as accounts payable and debts.

How is working capital calculated?

Working capital is calculated by taking a company’s current assets and deducting current liabilities. For instance, if a company has current assets of $100,000 and current liabilities of $80,000, then its working capital would be $20,000. Common examples of current assets include cash, accounts receivable, and inventory.

What is the net working capital formula?

Understanding the intricacies of its formula, components, and limitations provides valuable insights into a firm’s liquidity and operational efficiency. NWC = Current Assets – Current Liabilities The Net Working Capital formula involves deducting current liabilities from current assets.