When it comes to roles that are essential to keep businesses up and running, accounting is always going to be a top contender. Why? Put simply, accounting–in all its forms–is the pulse of an organization. It informs all stakeholders of the financial state of the business so managers, investors and owners can make intelligent, informed decisions to succeed.

There are several different types of accounting–from cost auditing to public accounting–but two of the most common are managerial (sometimes referred to as management) accounting and financial accounting.

If you’re exploring accounting as a career option, understanding the difference between these two types of accounting is important. This article will help you differentiate between managerial and financial accounting so you can have a better idea of which direction you may want to take in your career.

For any business, having a solid understanding of accounting is crucial for success. Accounting helps businesses track financial performance, ensure legal compliance, gain actionable insights, and make smart strategic decisions. While there are several branches of accounting, two of the main types are managerial accounting and financial accounting.

Both managerial and financial accounting involve working with financial data and producing financial reports. However, there are some key differences between the two when it comes to the focus, purpose, frequency and presentation of reports. Below is an in-depth look at managerial accounting vs financial accounting and how they compare.

Overview of Managerial Accounting

Managerial accounting also known as management accounting, refers to the process of identifying analyzing, interpreting and communicating financial information to managers within an organization. The reports and insights provided by managerial accounting are intended for internal use only.

The goal of managerial accounting is to provide managers with the financial information and insights they need to make sound business decisions. Rather than just looking at dollars and cents, managerial accounting looks at both financial and operational data to determine how business operations are performing. Some key responsibilities include:

- Budgeting and forecasting

- Cost and revenue analysis

- Reviewing operational efficiency

- Assessing capital needs and allocation

- Strategic decision making

- Identifying opportunities for improvement

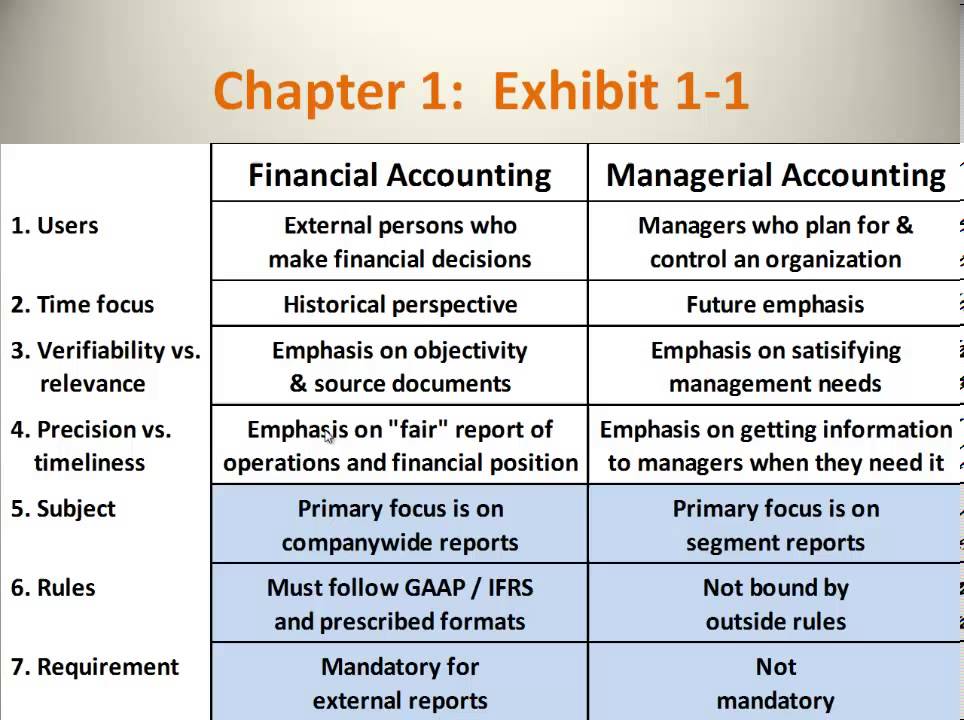

While financial accounting focuses on reporting historical figures, managerial accounting has a forward-looking focus. Reports are tailored to the specific needs of management and aim to help plan, control and evaluate departmental or organizational performance.

Overview of Financial Accounting

Financial accounting refers to the process of gathering recording and summarizing financial data to create reports and financial statements that provide information about a company’s financial performance. These reports are intended for use by both internal stakeholders (managers employees) and external stakeholders (investors, regulators, lenders).

The goal of financial accounting is to provide an accurate picture of a company’s financial health and activities over a period of time. This includes details on revenues expenses, assets, liabilities cash flow and profitability. Some key responsibilities include

- Gathering and monitoring financial data

- Ensuring regulatory compliance

- Preparing financial statements

- Evaluating company financial status

- Providing historical performance data

The reports created through financial accounting, like the income statement, balance sheet and statement of cash flows, provide important information to external decision makers. These standardized reports also allow comparison between different companies in the same industry.

Key Differences Between the Two

While both managerial and financial accounting involve working with a company’s financial data, there are some notable differences between the two:

Purpose

-

Financial accounting aims to provide standardized information to external stakeholders.

-

Managerial accounting provides information to internal management to support decision making.

Focus

-

Financial accounting focuses on the past, recording and classifying historical transactions.

-

Managerial accounting has a future orientation, providing data to plan, budget and forecast.

Users

-

Financial accounting reports are distributed externally to investors, regulators, lenders.

-

Managerial accounting reports are used internally by managers and executives.

Level of Detail

-

Financial accounting provides high-level summarized data.

-

Managerial accounting dives into more detail on departmental performance.

Standards

-

Financial accounting follows GAAP standards.

-

Managerial accounting does not have to follow standardized guidelines.

Frequency

-

Financial statements are produced quarterly and annually.

-

Managerial reports can be created more frequently, even daily or weekly.

Regulations

-

Financial accounting must comply with regulations and accounting standards.

-

Managerial accounting does not have to adhere to regulations.

Financial Statements vs. Managerial Reports

The different focus and goals of financial and managerial accounting lead to differences in the format, content and frequency of reports:

Financial Statements

- Income statement

- Balance sheet

- Statement of cash flows

- Statement of stockholders’ equity

- Quarterly and annual filing

Managerial Reports

- Budget reports

- Cost benefit analysis

- Sales reports

- Department performance reviews

- Inventory reports

- Cost reports

- Daily, weekly or monthly reports

While financial statements condense a company’s finances into standardized documents, managerial reports can take many forms and be customized to analyze specific operations based on management needs.

Software Differences

The systems and software used for financial and managerial accounting also tend to differ.

Financial accounting requires software robust enough to handle strict regulatory compliance and the complexity of external reporting. Popular solutions include NetSuite, Sage Intacct, and SAP.

Managerial accounting prioritizes planning, forecasting, analytical and reporting capabilities. Some options like NetSuite and Sage Intacct handle both managerial and financial needs, while others like Adaptive Insights focus specifically on managerial functions.

Roles and Certifications

The different functions of managerial and financial accounting lead to some differences in the professionals who work in each area:

Financial Accounting

- Performed by accountants or financial analysts

- Overseen by a chief financial officer (CFO)

- Requires a CPA certification

Managerial Accounting

- Performed by management accountants

- Overseen by a controller

- Requires a CMA certification

While both roles require an understanding of accounting principles and financial reports, managerial accountants focus more on business analysis and strategic decision-making.

Benefits of Each

Employing both financial and managerial accounting offers several benefits:

Benefits of Financial Accounting

- Standardized reporting facilitates comparison

- Helps secure financing

- Builds credibility and transparency

- Ensures compliance with regulations

- Provides historical performance data

Benefits of Managerial Accounting

- Supports data-driven decision making

- Identifies cost centers and profit drivers

- Enables accurate budgeting and forecasting

- Improves operational efficiency

- Allows adaptation to meet management needs

Using both together provides an accurate picture of where the company has been, where it is now, and where it hopes to be in the future.

Example Comparing the Two

Here is an example that illustrates the key differences between financial and managerial accounting:

Lucid Motors is a startup automotive company. As they look to ramp up production, the accounting department prepares the following reports:

Financial Accounting

- Income statement summarizing company revenues and expenses for the year

- Balance sheet presenting total assets and liabilities

- Cash flow statement showing cash inflows and outflows

These reports follow GAAP standards and are distributed to external shareholders through the company’s annual report.

Managerial Accounting

- Cost report analyzing manufacturing costs for their new model

- Budget forecast projecting costs and revenue for the next year

- Sales report breaking down units sold by geographic region

- Inventory report tracking raw materials and parts on hand

These reports were created for internal use to help management make decisions about pricing, inventory management, HR allocation and more. The CFO and controllers used insights from these reports to create a presentation for the executive team planning future growth.

This example highlights how financial accounting focuses on retrospective overall company data for external use, while managerial accounting provides granular internal data to support strategy and operations.

In Summary

Managerial accounting and financial accounting serve different purposes for different audiences, but both are crucial for business success. While managerial accounting looks inward to provide key insights to managers, financial accounting looks outward to provide transparent reports to shareholders and regulators.

Understanding the key differences between financial and managerial accounting allows businesses to implement the right accounting processes, software solutions and personnel to cover all their accounting bases. Taking a comprehensive approach ensures that both historical finances and forward-looking insights are leveraged to support growth and profitability.

How Are Managerial and Financial Accounting Careers Different?

Even though managerial and financial accounting positions are similar in that they both deal with complex numbers, there are multiple differences in their day-to-day functions, the type of information they review and report on and with whom they communicate.

Keep reading to explore how they are different by reading what each specialization prioritizes and accomplishes. Envision yourself doing some of the tasks described for this type of accounting to begin to form an opinion on which one feels right for your personal goals. Lastly, do not overlook the higher education and certification or licensure requirements as those often help professionals choose which specialization they want to pursue.

What to Know About Managerial Accounting

Managerial accounting is a type of accounting that focuses on meeting the needs of internal stakeholders at a business. Responsibilities can include completing internal-facing tasks and creating the reports necessary to operate a business, such as monitoring and reporting on costs, sales, spending, budgets and internal financial trends. People in this type of accounting are focused on the future, and will often run “what-if” scenarios for company leadership to help them make decisions to ensure the business stays profitable. On a day-to-day basis, people in managerial accounting will follow internal rules and best practices to accomplish tasks.

What to Know About Financial Accounting

Financial accounting is a type of accounting that is focused on communicating the financial information of a company to external stakeholders, such as the IRS, creditors, investors or the U.S. Securities and Exchange Commission. They work internally to meet the needs of clients, customers, or other outside entities that do not work directly with the company but can affect or be affected by the business or projects. Typical responsibilities in this type of accounting can include gathering and maintaining historical data to create reports such as income statements, cash flow statements and balance sheets.

Unlike managerial accounting–which follows internally created rules and processes–financial accounting activities and processes must follow the Generally Accepted Accounting Principles (GAAP). According to the U.S. Securities and Exchange Commission, GAAP are the accounting standards, conventions and rules companies use to measure their financial results including net income and how companies record assets and liabilities.

Explore more differences between these two accounting specializations in the chart below.

What do Earning Potential and Job Growth Look Like in Managerial and Financial Accounting?

Despite having many differences, management and financial accounting positions are both slated to have steady growth over the next 8-10 years. The Bureau of Labor Statistics (BLS) estimates that jobs for all accountants and auditors will grow by 7% by 2030. According to the BLS, globalization, a growing economy and a complex tax and regulatory environment, are expected to continue to lead to strong demand for accountants and auditors.

As the overall demand for the accounting industry grows, so will the need to fill the various roles available under both managerial or financial accounting. Since there are a variety of positions you can choose to pursue under each type of accounting, we chose to share some of the top jobs in each category and their median advertised salaries so you can make informed decisions about your career.