What you need to know about these financial statements Part of the Series How to Value a Company Introduction to Company Valuation

A company’s balance sheet provides a snapshot of its financial position at a specific point in time It summarizes what the business owns and owes, One key component shown on a balance sheet is the company’s capital

Capital on a balance sheet refers to the funds invested into the business by its owners, shareholders, or partners It represents their stake in the company and claims on its assets and profits Understanding what capital is, where it comes from, and how it impacts your business can provide valuable insights into the company’s finances.

What Makes Up Capital on a Balance Sheet?

Capital, also known as equity, encompasses several accounts that quantify the owners’ investments, contributions, and claims to the company Key elements include

-

Paid-in capital – Amounts invested into the business by owners through purchasing shares or contributing cash and assets. This includes:

- Common stock at par value

- Preferred stock

- Paid-in capital in excess of par

- Partners’ capital contributions

-

Additional paid-in capital – Funds invested in the company above and beyond the par value of shares issued. This account tracks premiums paid by shareholders purchasing stock.

-

Retained earnings – The company’s accumulated net income since inception that has been retained rather than distributed to owners as dividends. This represents profits reinvested into growing the business.

-

Treasury stock – Previously outstanding shares of the company’s stock that were repurchased. This decreases the amount of capital.

-

Drawing accounts – Amounts withdrawn by owners for personal use, reducing the capital.

The sum of these accounts gives you the total equity the owners have in the business.

Understanding Where Capital Comes From

When a business first launches, the initial capital typically comes directly from the owners putting their own money into the company. The founders might contribute cash to fund startup costs like rent, equipment, and inventory.

Ongoing sources of additional capital include:

-

Owner investments – Owners can inject more of their own money over time when the company needs funds to grow and expand.

-

Retained earnings – Rather than distributing all profits to owners, some gets retained in the business as capital for funding growth plans.

-

Sale of stock – Selling shares of company stock to outside investors raises funds that get added to capital.

-

Loans – In some cases debt can be converted into capital via debt-to-equity swaps. The lender trades the loan for shares of stock.

-

Crowdfunding – Platforms like Kickstarter and Indiegogo allow startups to raise capital by selling equity stakes to many small investors.

Understanding where your business’s capital comes from helps you strategize how to fund growth going forward.

Why Capital Matters for Your Company

Tracking the capital invested in your business is crucial for several reasons:

-

Measures owner stakes – The balance of capital accounts quantifies how much each owner or shareholder has contributed and their share of ownership.

-

Indicates funding ability – The size and types of capital reveal how much funding you have to work with for growth plans.

-

Drives company value – The total capital helps determine the market value of the overall business. Capital plays a key role in valuation.

-

Impacts financing – Your capital structure and sources impact your ability to secure loans, investors, and other outside financing.

-

Shows retained profits – Retained earnings reveal how much net income the company has earned and retained historically.

Monitoring your business capital enables smarter strategic decisions about funding, valuations, ownership stakes, profits distribution and more.

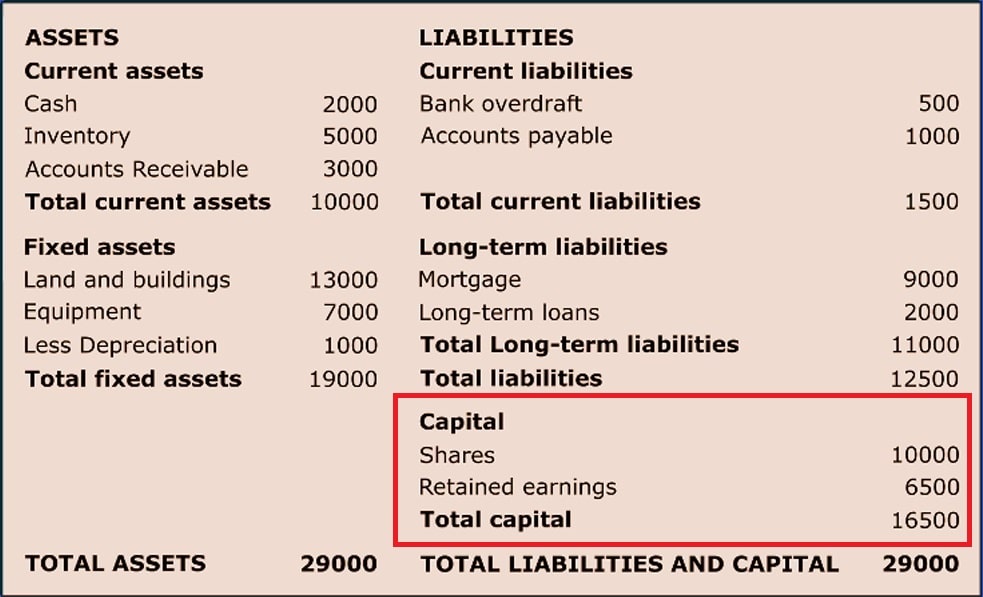

Example of Capital on a Balance Sheet

Let’s look at an example to see capital accounts in action on a balance sheet:

XYZ Company Balance Sheet

| Assets | |

|---|---|

| Cash | $100,000 |

| Accounts Receivable | $50,000 |

| Inventory | $75,000 |

| Total Assets | $225,000 |

| Liabilities | |

| Accounts Payable | $60,000 |

| Total Liabilities | $60,000 |

| Capital | |

| Common Stock | $100,000 |

| Retained Earnings | $65,000 |

| Total Capital | $165,000 |

| Total Liabilities & Capital | $225,000 |

This balance sheet shows the company has $100,000 worth of stock issued, representing the capital originally contributed by the founders. The $65,000 in retained earnings are profits that have accumulated over time and remain invested in the business.

Together, the $100,000 of paid-in capital and $65,000 of retained earnings make up the total owners’ equity of $165,000. This capital helps cover the company’s assets and exceeds its liabilities.

Tips for Managing Your Business’s Capital

Here are some tips to help you optimize your balance sheet capital:

-

Review capital accounts regularly to ensure accurate tracking of owner investments and equity stakes.

-

Build up a strong retained earnings pool to fund expansion plans with reinvested profits.

-

Evaluate whether to distribute dividends vs. retain profits based on growth objectives.

-

Pursue financing strategies aligned with your capital structure and ownership model.

-

Analyze returns on capital invested and make adjustments if parts of the business underperform.

-

Maintain detailed records of capital contributions and withdrawals by each owner.

-

Avoid withdrawing excessive equity that depletes needed business capital.

Proactively managing your capital is key to keeping your balance sheet and funding sources aligned with strategic growth plans.

The Takeaway

Capital is a vital component of the balance sheet, representing the owners’ financial stakes and the funds invested in the company. Tracking paid-in capital, retained earnings, equity shares, and owner contributions provides visibility into the finances supporting your business. Paying close attention to the sources and uses of capital will enable smarter decision making as you operate and expand the company. Just remember that capital matters for your small business success.

Liabilities

A liability is any money that a company owes to outside parties, from bills it has to pay to suppliers to interest on bonds issued to creditors to rent, utilities and salaries. Current liabilities are due within one year and are listed in order of their due date. Long-term liabilities, on the other hand, are due at any point after one year.

Current liabilities accounts might include:

- Current portion of long-term debt is the portion of a long-term debt due within the next 12 months. For example, if a company has a 10 years left on a loan to pay for its warehouse, 1 year is a current liability and 9 years is a long-term liability.

- Interest payable is accumulated interest owed, often due as part of a past-due obligation such as late remittance on property taxes.

- Wages payable is salaries, wages, and benefits to employees, often for the most recent pay period.

- Customer prepayments is money received by a customer before the service has been provided or product delivered. The company has an obligation to (a) provide that good or service or (b) return the customers money.

- Dividends payable is dividends that have been authorized for payment but have not yet been issued.

- Earned and unearned premiums is similar to prepayments in that a company has received money upfront, has not yet executed on their portion of an agreement, and must return unearned cash if they fail to execute.

- Accounts payable is often the most common current liability. Accounts payable is debt obligations on invoices processed as part of the operation of a business that are often due within 30 days of receipt.

- Long-term debt includes any interest and principal on bonds issued

- Pension fund liability refers to the money a company is required to pay into its employees retirement accounts

- Deferred tax liability is the amount of taxes that accrued but will not be paid for another year. Besides timing, this figure reconciles differences between requirements for financial reporting and the way tax is assessed, such as depreciation calculations.

Some liabilities are considered off the balance sheet, meaning they do not appear on the balance sheet.

Components of a Balance Sheet

Accounts within this segment are listed from top to bottom in order of their liquidity. This is the ease with which they can be converted into cash. They are divided into current assets, which can be converted to cash in one year or less; and non-current or long-term assets, which cannot.

Here is the general order of accounts within current assets:

- Cash and cash equivalents are the most liquid assets and can include Treasury bills and short-term certificates of deposit, as well as hard currency.

- Marketable securities are equity and debt securities for which there is a liquid market.

- Accounts receivable (AR) refer to money that customers owe the company. This may include an allowance for doubtful accounts as some customers may not pay what they owe.

- Inventory refers to any goods available for sale, valued at the lower of the cost or market price.

- Prepaid expenses represent the value that has already been paid for, such as insurance, advertising contracts, or rent.

Long-term assets include the following:

- Long-term investments are securities that will not or cannot be liquidated in the next year.

- Fixed assets include land, machinery, equipment, buildings, and other durable, generally capital-intensive assets.

- Intangible assets include non-physical (but still valuable) assets such as intellectual property and goodwill. These assets are generally only listed on the balance sheet if they are acquired, rather than developed in-house. Their value may thus be wildly understated (by not including a globally recognized logo, for example) or just as wildly overstated.

The BALANCE SHEET for BEGINNERS (Full Example)

What is capital on a balance sheet?

Capital on a balance sheet refers to any financial assets a company has. This is not limited to cash—rather, it includes cash equivalents as well, such as stocks and investments. Capital can also include a company’s facilities and equipment. There are four main types of capital:

Where is capital shown in a financial statement?

Within a company’s financial statements, capital is typically shown in the balance sheet. The balance sheet is a financial statement that shows a company’s assets, liabilities, and shareholders’ equity. Shareholders’ equity represents the amount of capital that the company has raised from its owners or shareholders.

Which side of a balance sheet outlines a company’s assets and liabilities?

The left side of the balance sheet outlines all of a company’s assets. On the right side, the balance sheet outlines the company’s liabilities and shareholders’ equity. T he assets and liabilities are separated into two categories: current asset/liabilities and non-current (long-term) assets/liabilities.

Why is capital important in a balance sheet?

Calculating capital is key to understanding your company’s financial status, and it is one of the most important elements of a balance sheet. Capital is used to make financial decisions and investments, so if you are in charge of completing company balance sheets, it is imperative that you do so accurately.