To prepare an income statement, small businesses must analyze and report their revenues, operating expenses, and the resulting gross profit or losses for a specific reporting period. The income statement, also called a profit and loss statement, is one of the major financial statements issued by businesses, along with the balance sheet and cash flow statement.

If you have found yourself struggling to find the time to create your own profit and loss report, or P&L, from scratch, a free invoice statement template is the perfect solution.

FreshBooks provides free template income statements that are pre-formatted for your needs. All you need to do is fill in the empty fields with the numbers you’ve calculated. No stress, just results.

An income statement, also known as a profit and loss (P&L) statement, is one of the most important financial statements for a business. It provides a summary of a company’s revenues, expenses, and profits over a specified period of time – usually a month, quarter, or full year.

Knowing how to prepare an accurate income statement is crucial for any business owner or financial manager. It allows you to track your company’s financial performance, identify areas for improvement, and make informed business decisions.

In this comprehensive guide, we will walk you through the entire process of preparing an income statement, from choosing the right reporting period to calculating net income Whether you’re new to financial reporting or just need a refresher, read on for tips, examples, and resources to master income statement preparation

Why Income Statements Matter

Before we dive into the nitty-gritty details, let’s review why income statements are so invaluable for businesses:

-

Track financial performance Income statements allow you to monitor trends in revenue, expenses, and profitability over time Detecting positive or negative trends helps forecast future performance.

-

Identify strengths and weaknesses. The income statement highlights which business activities are generating the most revenues and which are racking up expenses. This helps pinpoint strengths to leverage and problem areas to improve.

-

Inform business decisions. With insights from income statements over recent periods, managers can make better-informed decisions about pricing, budgets, investments, staffing, and more.

-

Assess growth opportunities. Income statements help businesses identify the most profitable business segments, customer demographics, and new opportunity areas to focus growth initiatives.

-

Secure financing. Lenders and investors often require income statements to evaluate a company’s financial health and repayment abilities before approving financing.

In short, the income statement provides vital intelligence for operating, managing, and growing a successful company. Now let’s look at how to put one together.

Steps to Prepare an Income Statement

Follow these seven key steps to prepare a complete and accurate income statement for your business:

1. Choose the Reporting Period

Income statements cover a specific window of time. Most companies prepare income statements on a monthly, quarterly, and annual basis. Consider which periods are most relevant for your business goals in choosing a reporting frequency.

Some tips for selecting reporting periods:

-

Monthly – Best for closely monitoring current performance and making tactical adjustments.

-

Quarterly – Allows analysis of performance across seasons and business cycles.

-

Annually – Gives the big picture of full-year performance and helps identify long-term trends.

2. Calculate Total Revenue

Add up all the revenue your company earned from sales, services, interest, or other sources during the reporting period. Common revenue line items include:

- Sales revenue

- Service revenue

- Interest revenue

- Rental revenue

- Licensing/royalty revenue

Tally the totals for each revenue stream for the reporting period.

3. Determine Cost of Goods Sold

Cost of goods sold (COGS) reflects the direct costs of manufacturing or purchasing products sold during the period. This includes:

- Raw material costs

- Packaging costs

- Direct labor costs

Total the costs directly tied to the products sold to determine COGS.

4. Calculate Gross Profit

Subtract COGS from total revenue to determine your gross profit for the period:

Gross Profit = Total Revenue – COGS

This represents the amount left over after deducting production costs from sales. It’s a useful measure of profitability.

5. List Operating Expenses

Add up all the overhead, payroll, administration, marketing and other expenses that keep your business running during the reporting window. Common expense line items include:

- Salaries

- Rent

- Utilities

- Marketing

- Insurance

- Office expenses

- Depreciation

Tally all operating expenses incurred during the period.

6. Determine Operating Income

Subtract total operating expenses from gross profit to calculate your company’s operating income (sometimes called earnings before interest and taxes or EBIT):

Operating Income = Gross Profit – Total Operating Expenses

This reveals the profitability of your company’s core business operations.

7. Deduct Interest, Taxes, and Other Expenses

Finally, account for interest paid on debt, tax expenses, and any other less common expenses that occurred during the reporting period:

- Interest expenses

- Income tax expenses

- Other expenses (e.g. legal settlements)

Subtract these from operating income to determine pre-tax net income.

8. Calculate Net Income

If your company has any tax credits or deferred taxes for the reporting period, make these adjustments to arrive at the final net income number.

Net Income = Pre-Tax Income – Tax Expenses + Tax Credits

This final profit number represents your company’s total earnings or losses for the reporting period after accounting for all revenues and expenses.

Income Statement Formats

Income statements can be presented in two different formats – single-step and multi-step.

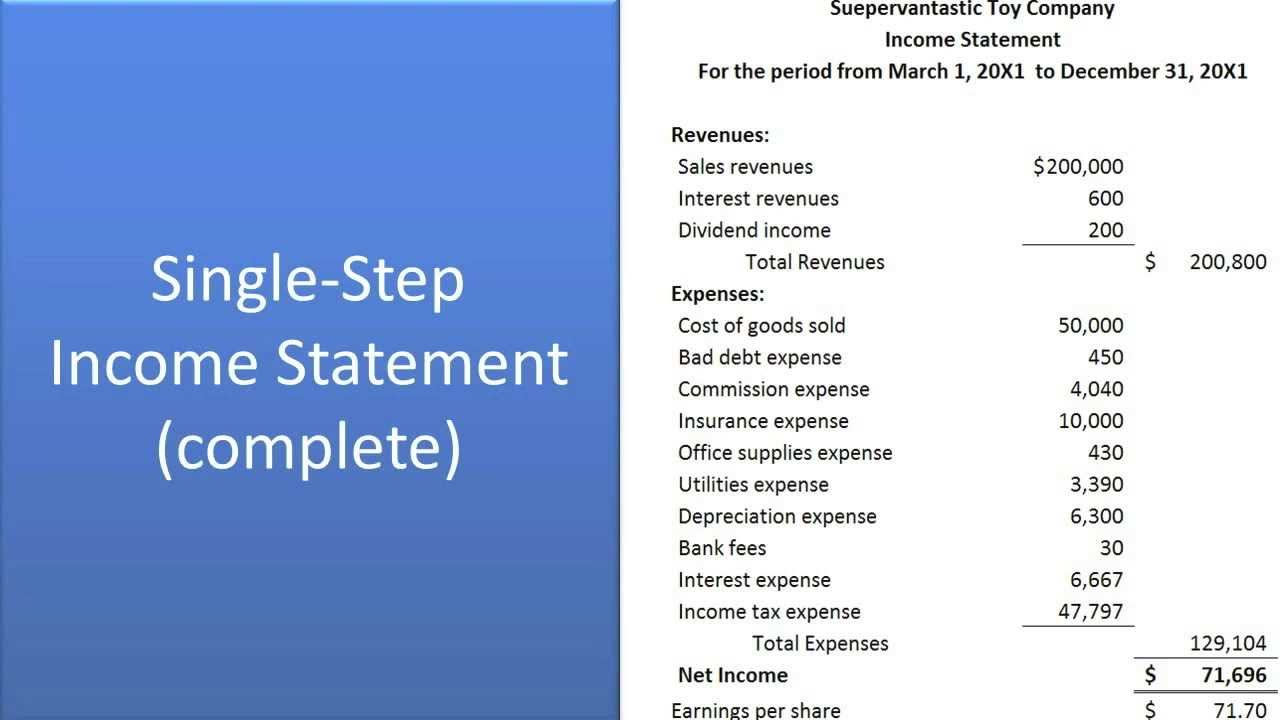

Single-Step Income Statement

This simpler format groups all revenues together and all expenses together to directly calculate net income in one step:

Single-Step Income Statement

| Revenues | $500,000 |

|---|---|

| Expenses | ($350,000) |

| Net Income | $150,000 |

Multi-Step Income Statement

This more complex format breaks out earnings into subtotals at each stage. It provides more detail on a company’s operating versus non-operating profitability.

Multi-Step Income Statement

| Sales Revenue | $1,000,000 |

|---|---|

| Cost of Goods Sold | ($500,000) |

| Gross Profit | $500,000 |

| Operating Expenses | ($200,000) |

| Operating Income | $300,000 |

| Other Expenses | ($50,000) |

| Pre-Tax Income | $250,000 |

| Income Taxes | ($75,000) |

| Net Income | $175,000 |

Choose the format that provides the ideal level of detail for your business’s needs.

Income Statement Tips

Keep these tips in mind as you prepare income statements:

-

Maintain organized records of all revenue and expense transactions over the period to compile data more easily.

-

Use accounting software to quickly populate and format income statement line items.

-

Analyze percentages and metrics like gross margin and EBITDA in addition to absolute dollar amounts.

-

Compare multiple periods side-by-side to identify performance trends.

-

Tie income statement data to other reports like balance sheets and cash flow statements to get a complete financial picture.

-

Have your income statement reviewed by a qualified accountant before finalizing and distributing.

Sample Income Statement

Here is an example of what a single-step income statement may look like:

ACME Company Inc.

Income Statement

| For the year ended December 31, 2022 |

|-|-|

| Sales Revenue | $1,500,000 |

| Service Revenue | $500,000 |

| Total Revenue | $2,000,000 |

| Cost of Goods Sold | $750,000 |

| Gross Profit | $1,250,000 |

| Operating Expenses | |

| Salaries | $500,000 |

| Rent | $60,000 |

| Utilities | $40,000 |

| Marketing | $100,000 |

| Other Expenses | $200,000 |

| Total Operating Expenses | $900,000 |

| Operating Income | $350,000 |

| Interest Expense | $25,000 |

| Other Expenses | $10,000 |

| Pre-Tax Income | $315,000 |

| Income Taxes | $100,000 |

| Net Income | $215,000 |

This sample income statement illustrates what a completed single-step income statement may look like for a simple business. Use it as a template to prepare your own company’s income statement.

Automate Your Income Statement

While it’s possible to manually calculate all income statement figures line-by-line, accounting software can save huge time and effort.

Programs like QuickBooks Online seamlessly pull revenue and expense data from your books to populate perfectly formatted income statements in seconds. They can produce monthly, quarterly, and annual income statements on demand for deeper insight into financial performance trends over time.

Investing in bookkeeping software is an easy call for any growth-focused business. Automating income statement and other financial report generation lets you focus on strategy vs. manual number-crunching.

Understand Your Income Statement and Profitability

Now that you’re armed with a step-by-step guide to preparing income statements, you have the knowledge to produce accurate financial reporting for your business.

Regularly generating and analyzing income statements provides visibility into the profit

Generate a Trial Balance Report

To create an income statement for your business, you’ll need to print out a standard trial balance report. You can quickly generate the trial balance through your cloud-based accounting software. Trial balance reports are internal documents that list the end balance of each account in the general ledger for a specific reporting period.

Creating balance sheets is a crucial part of creating a profit and loss, as it’s how a company gathers data for its account balances. It will give you all the end balance figures you need to create an income statement.

Calculate Your Income

Subtract the selling and administrative expenses total from the gross margin. Doing this will give you the amount of pre-tax operating income. Enter the amount at the bottom of the income statement.

How to Prepare an Income Statement (Step by Step)

How do you write a basic income statement?

For a basic income statement, the main things you will write out would be revenue, and expenses, and subtracting the total two to get your net income. But an extended income statement will start to include your COGS and gross profit and operating expenses. Subtract the cost of goods sold from sales revenue to find your gross profit.

What is included in an income statement?

An income statement includes all instances of money flowing into or out of a company (revenue and expenses) as well as instances of the company making or losing money without cash changing hands, such as the value of business assets rising or falling.

How do you write sales revenue on an income statement?

Write “Sales Revenue” below the income statement header. Sales revenue includes all revenue earned from the sale of goods and services, regardless of whether or not the cash has been collected. List sales revenue for the period you selected. For example, say that you sold 10,000 units of inventory for $5 USD a piece.

How do you prepare an income statement?

Thus, preparing an income statement involves compiling a list of revenue, expenses, losses and gains. Once these items are consolidated, they’re organized into categories and added to calculate net income over the period the statement covers. When compiling an income statement, including the correct items and categories is crucial.