When tax time comes around, Americans are often required to become better acquainted with certain tax terms — even if they are not accountants. Thankfully, most of us leave the majority of the tax prep work to the tax experts. However, when it comes to the different ways in which your taxable income can be described, things can get confusing. For this reason, its a good idea to get a better understanding of the difference between your gross income and adjusted gross income and how it impacts your personal financial planning.

As tax season approaches, many taxpayers start gathering documents and crunching numbers to file their tax returns Two key figures that feature prominently on tax returns are gross income and adjusted gross income (AGI). While they may sound similar, gross income and AGI are different Understanding the difference between these two amounts is crucial for filing an accurate tax return and determining your tax liability.

In this article, I will explain in simple terms what gross income and AGI are, how they are calculated, and why the distinction matters. Whether you prepare your own tax return or use a tax professional, having a solid grasp of these fundamental tax concepts will help you file properly and maximize your tax deductions

What is Gross Income?

Gross income refers to all the income you receive over the year from any and all sources, before any deductions or adjustments are made. According to the IRS, gross income encompasses:

- Wages, salaries, bonuses, commissions

- Tips

- Interest income

- Dividends

- Alimony received

- Business income

- Gains from sale of property or investments

- Rental income

- Retirement plan distributions

- Unemployment compensation

- Social security benefits

- Gambling or lottery winnings

- Awards and prizes

- Jury duty fees

- Hobby income

- Forgiveness of debt

- Other miscellaneous income

In simple terms, any money you receive from any source in a given tax year makes up your total gross income, with a few exceptions. For instance, child support payments, gifts, and inheritances are not considered gross income.

Gross income acts as the starting point for calculating your taxable income and how much tax you owe. But you do not pay income tax on the full amount of your gross income. Certain adjustments and deductions are permitted to reduce your gross income. The resulting number is your adjusted gross income or AGI.

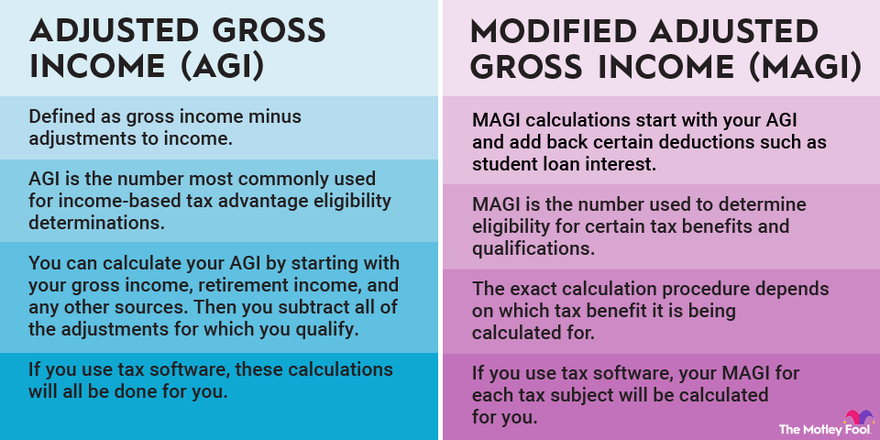

What is Adjusted Gross Income (AGI)?

Adjusted gross income is your gross income reduced by certain adjustments called “above-the-line” deductions. In other words, it is your gross income minus adjustments allowed by the tax code. The most common above-the-line deductions include:

- Contributions to traditional IRAs

- Student loan interest

- Educator expenses

- Certain business expenses of reservists, artists, and fee-basis government officials

- Health savings account deductions

- Moving expenses

- Self-employment tax

- Self-employed SEP, SIMPLE, and qualified plans

- Self-employed health insurance deduction

- Penalty on early withdrawal of savings

- Alimony paid

These above-the-line deductions are subtracted from your gross income to arrive at your AGI. Some taxpayers may not be eligible for any above-the-line deductions, in which case their gross income and AGI would be the same. Either way, AGI will always be lower than or equal to your gross income.

Unlike gross income, AGI is not just a number you calculate, it actually appears on line 11 of your Form 1040. AGI is crucially important because it determines your eligibility for certain tax deductions, credits, and income phaseouts further down your return.

How Gross Income and AGI Are Used on Your Tax Return

Now that we understand what gross income and AGI represent, let’s see how they work on your tax return:

-

Add up all items that count as gross income from your W-2, 1099s, and other income sources. This gives your total gross income for the year.

-

Identify any above-the-line deductions you can claim and subtract them from your gross income. The resulting number gives your AGI.

-

On your Form 1040, report gross income on line 1. Report AGI on line 11.

-

AGI is then used to determine if you qualify for certain deductions like the student loan interest deduction, as well as tax credits like the child tax credit and education credits.

-

AGI may also impact how much of certain deductions you can claim. For instance, you can only deduct qualified medical expenses that exceed 7.5% of your AGI.

-

Taxable income is calculated by subtracting the greater of your standard deduction or itemized deductions from your AGI.

-

Your final tax liability depends on your taxable income and tax bracket.

As you can see, AGI serves as the basis for calculating many other parts of your 1040. That’s why correctly distinguishing gross income from AGI is so important.

Why the Difference Matters

Some taxpayers assume gross income and AGI are interchangeable terms referring to the same amount. While it’s an easy mistake to make, not understanding the difference can potentially cost you. Here are some key reasons why distinguishing between gross income and AGI matters:

-

Claiming above-the-line deductions helps lower your AGI, which may make you eligible for more tax breaks.

-

A lower AGI allows you to deduct a greater portion of itemized deductions like medical expenses.

-

Education credits and certain other tax credits begin phasing out at higher AGIs. Minimizing your AGI may help maximize these credits.

-

High income taxpayers also face AGI-based phaseouts on tax breaks like the child tax credit.

-

Certain retirement account contributions like Roth IRAs have income limits based on AGI. A lower AGI increases your contribution room.

-

Various tax cut-offs like the net investment income tax and Medicare surtax are also tied to AGI levels.

As you can see, being mindful of deductions that reduce AGI can lead to significant tax savings. When preparing your return, be sure to claim any above-the-line deductions you qualify for and double check that your gross income and AGI are calculated correctly.

Examples of Gross Income vs AGI

To better demonstrate the relationship between gross income and AGI, let’s look at a few examples:

Example 1:

- Jennifer has $60,000 in wages.

- She contributes $5,000 to her company 401(k).

- She has $2,000 in bank account interest.

- Jennifer’s gross income = $60,000 (wages) + $2,000 (interest) = $62,000

- Her only above-the-line deduction is the $5,000 401(k) contribution.

- Jennifer’s AGI = $62,000 (gross income) – $5,000 (401k contribution) = $57,000

Example 2:

- Mark has $100,000 in freelance income.

- He deducts $15,000 of business expenses.

- He has no other income or above-the-line deductions.

- Mark’s gross income = $100,000

- His only above-the-line deduction is the $15,000 of business expenses.

- Mark’s AGI = $100,000 – $15,000 = $85,000

Example 3:

- Sara has $45,000 in wages.

- She deducts $3,000 for student loan interest.

- She has no other income.

- Sara’s gross income = $45,000

- Her only above-the-line deduction is the $3,000 student loan interest.

- Sara’s AGI = $45,000 – $3,000 = $42,000

I hope these examples help clarify how gross income, adjustments, and AGI work together on your tax return. Please feel free to drop any other questions in the comments!

Common Questions about Gross Income and AGI

Here are some quick answers to frequently asked questions on this topic:

Can your AGI be higher than gross income?

No, AGI will always be lower than or equal to your gross income. It is your gross income reduced by deductions.

What if I have no adjustments to gross income?

Your AGI would simply equal your gross income. Having no adjustments is common for many W-2 employees.

Is AGI the same as taxable income?

No. AGI comes before you deduct the standard or itemized deductions. Taxable income is AGI minus deductions.

Can I deduct healthcare expenses from gross income?

No. You can only deduct medical expenses to the extent they exceed 7.5% of your AGI, so they come after AGI.

Does gross income include capital gains?

Yes. Gross income includes all your capital gains, not just the taxable portion.

Is gross income the same as earned income?

No. Earned income refers specifically to wages, salaries, and net self-employment income. Gross income includes other unearned sources too.

I hope these quick FAQs covered some of the common questions surrounding gross income and AGI! Please ask any other questions you may have in the comments.

In Conclusion

Calculating gross income and adjusted gross income are important first steps in completing your Form 1040 accurately, determining your eligibility for deductions and credits, and assessing your overall tax liability.

While they may sound alike, gross income and AGI are two distinct figures:

-

Gross income includes all income from all sources before deductions.

-

AGI is gross income

What is adjusted gross income?

Your adjusted gross income (AGI) is equal to your gross income minus any eligible adjustments that you may qualify for. These adjustments to your gross income are specific expenses the IRS allows you to take that reduce your gross income to arrive at your AGI. Some of these adjustments to income include contributions to your traditional IRA, student loan interest and alimony payments.2 If youre doing your own taxes, you can determine your AGI with an online calculator from a source you trust or there are DIY tax programs that can also help you to determine this figure and guide you through preparing and filing both your federal and state tax returns.

Your AGI is an important calculation not only because it influences your tax bracket, but it may determine your eligibility to claim additional deductions and credits that may be available to you when you file your tax returns. Moreover, there are some states that may use your AGI as a base for calculating your state taxable income.

How to calculate annual gross income?

You can approximate your annual gross income using the following calculations.

- To convert your hourly income to annual income, multiply your hourly rate by 2,000

- To convert your weekly income to annual income, multiply by 50

To see how this works, lets consider an example.

If Tom earns $30 an hour at his job, what would his annual gross income be? Using the chart above as a guide, multiply $30/hour by 2,000 to get to $60,000 as an approximation.

To calculate specifically, at $30/hour, assuming Tom is full time (40 hours a week), he will earn $1,200 week. Assuming he works 51 of the 52 weeks per year, that equals $61,200.