Understanding cost functions is a vital skill for any business leader, manager, or entrepreneur. A cost function allows you to model the total cost of producing various levels of output for your business. Mastering cost functions enables smarter pricing, production, and strategy decisions.

In this comprehensive guide, we’ll explain what cost functions are, how to find your business’ cost function, and how to apply cost functions to optimize your operations Read on to boost your financial modeling skills!

What is a Cost Function in Business?

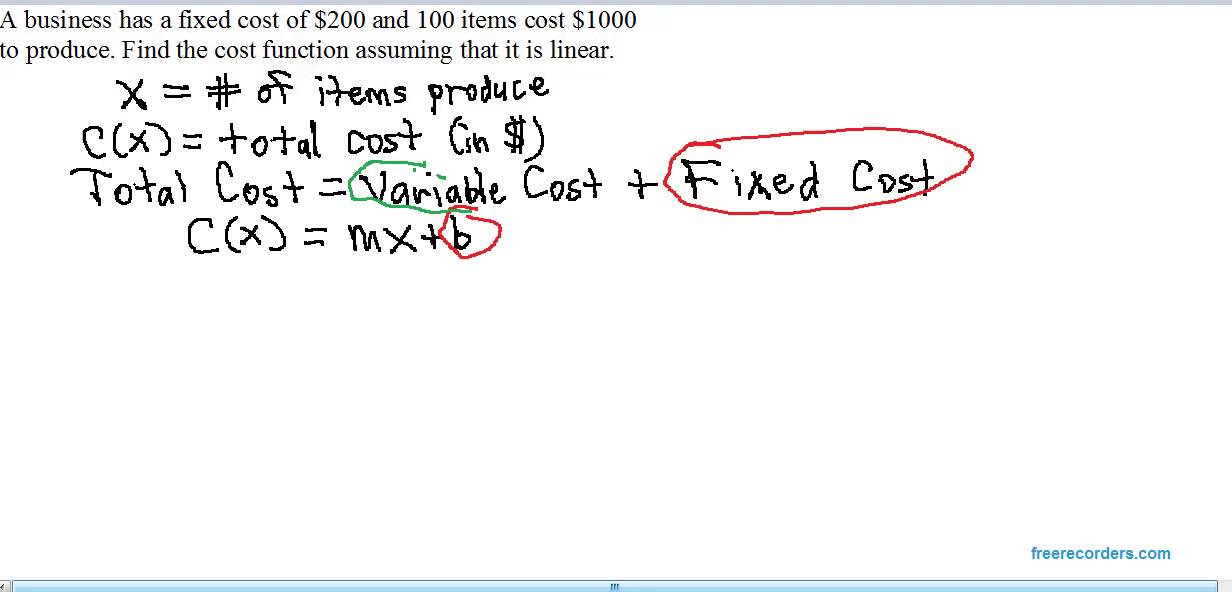

A cost function is an equation that expresses a company’s total cost of production as a variable of the output quantity. In simple terms a cost function shows how total costs change as production increases or decreases.

Cost functions include:

-

Fixed costs – Expenses that don’t vary with production volume, like rent.

-

Variable costs – Expenses that increase with production volume, like materials.

-

Total costs – The sum of all fixed and variable costs.

The three most common cost functions are:

- Linear cost function: TC = (FC) + (VC per unit) x Q

- Quadratic cost function: TC = (FC) + (VC per unit)xQ + (MC per unit2)xQ2

- Cubic cost function: TC = (FC) + (VC per unit)xQ + (MC per unit2)xQ2 + (SC per unit3)xQ3

Where:

- TC = Total Cost

- FC = Fixed Cost

- VC = Variable Cost

- MC = Marginal Cost

- SC = Second-order Cost

- Q = Quantity Produced

Understanding how to find and use these cost functions is pivotal for maximizing profitability.

Why Do Cost Functions Matter?

Cost functions help managers determine the most profitable production quantities and pricing strategies. Key applications include:

Optimal Output Level

The output level that minimizes average cost per unit is optimal for profitability. The cost function reveals what this quantity is.

Pricing Decisions

Knowing your total costs at varying output levels enables smarter pricing. You can set competitive yet profitable prices.

Identifying Economies of Scale

Cost functions reveal when you achieve lower average costs through expanded production (economies of scale).

Budgeting

Cost functions help accurately forecast expenses at different activity levels for better budgeting.

Evaluating Profitability of Growth

Understand how total expenses change as you grow. Avoid overexpanding by modeling cost impacts of growth.

Assessing Process Improvements

Adjust cost functions to represent potential savings from capital investments or process changes.

How to Find Your Company’s Cost Function

Determining your business’ cost function takes some financial legwork, but following this process will get you there:

Step 1: Identify Your Fixed Costs

Tally all expenses that don’t fluctuate with production volume, such as:

- Rent

- Insurance

- Salaries

- Property taxes

- Licenses

Step 2: Identify Your Variable Costs

Tally all variable expenses that increase directly with production:

- Direct material costs

- Packaging costs

- Commissions

- Direct labor

Step 3. Calculate Marginal Costs

Marginal cost is the incremental expense of producing one additional unit. Marginal costs tend to rise as production increases due to factors like overtime, rush orders, strained resources, etc. Understand how your marginal costs trend in relation to output.

Step 4. Plot Total Costs

Use your fixed costs, variable costs, and marginal costs at sample output levels to graph your total cost function. Connect the points to display the cost curve.

Step 5. Determine the Cost Function Equation

Examine the shape of your total cost curve to determine whether it resembles a linear, quadratic, or cubic function. Then solve for the equation that fits your cost data points.

Voila! You now have your business’ cost function equation that models total production costs at any output level.

Tips for Finding Accurate Cost Functions

Follow these tips to develop the most precise cost functions possible:

-

Collect granular cost data – Track detailed production data and cost data over time. More data points lead to more accurate functions.

-

Consider economies of scale – Account for how marginal costs may decrease at higher outputs due to bulk discounts on materials and efficiencies.

-

Include overhead costs – Indirect overhead expenses like utilities and HR should be allocated to production costs.

-

Use multiple output levels – Calculate total costs at different output quantities to establish the cost function’s shape.

-

Model multiple scenarios – Create alternative cost functions for best case, worst case, and moderate efficiency scenarios.

-

Regularly update the functions – Review and adjust your cost functions quarterly as costs change. Outdated functions lead to poor decisions.

How to Use Cost Functions to Maximize Profits

Once you have accurate cost functions, here are some key ways to apply them to boost profitability:

Optimal Output Level

Determine the output level where marginal cost equals marginal revenue, and set production quantities based on this optimum level.

Price Setting

Factor in your total costs when establishing pricing. For maximum profitability, set price where marginal revenue equals marginal cost.

Make vs Buy Decisions

Compare your cost functions against vendors’ prices to determine what’s cheaper to produce in-house versus outsource.

Budgeting

Plug planned production levels into your cost functions to forecast expenses. This leads to more accurate budgets.

Evaluating Operational Changes

Model how proposed process changes could alter your cost function and determine impact on profitability.

Assessing Economies of Scale Benefits

See if increased output lowers average costs enough to justify operational investments to support growth.

Managing Profitability by Department

Develop cost functions by department to identify which areas have costs rising faster than their output.

With the right insight into your cost functions, you can pursue a variety of strategies like these to maximize profitability and gain an edge over your competitors. So tackle the upfront work to find accurate cost functions, and then apply them regularly to drive better decision making.

Key Takeaways on Finding and Applying Cost Functions

-

Cost functions model how total costs change in relation to output quantity. Accurately identifying your cost function is crucial for maximizing profits.

-

Fixed, variable, marginal costs and economies of scale impact the shape of total cost functions. Gather detailed data to build precise functions.

-

Cost functions reveal optimal output levels, support pricing strategies, inform make vs buy decisions, and assist budgeting.

-

Regularly update cost functions. Use them to evaluate operational changes and identify the most lucrative growth opportunities.

Now that you’re armed with expert knowledge on determining and applying cost functions, you have a powerful tool for boosting your business’ financial performance. So embrace your inner math geek and put these cost modeling skills to work driving increased profitability. You’ve got this!

Cost Function Formula Components

The cost function formula is also applicable during the budget making process; thank to its outline which is:

C(x) = F + Vx

C = Total Expenses

X = Number of Units Produced

F = Fixed Costs

V = Variable Costs.

We must remember that fixed costs remain unchanged despite the level of production, and they include machinery costs, rent, or insurance payments. On the other hand, variable costs, which include labor and materials, will change from time to time and have a direct relationship to the level of production.

Cost Function Formula Example

ROG Company manufacture iron sheets and uses the cost function formula frequently when preparing its budget. It is the tool, which determines the company’s ideal product mix. Its fixed related costs amount to $100,000.

The company produces 60,000 feet of iron sheets whereby each foot costs $3.50

Here is how ROG yields the cost function formula calculation

C(x) = F + Vx

Cost = $100,000 + $3.50 (60,000)

With this, ROG can easily make decisions on whether or not it is worth producing 60,000 pieces of iron sheets, more or less, and what kind of profit should it expect?

Cost, Revenue, Profit functions, Break even point

How to create a cost function?

There are three main steps to create a cost function, those are: Find the fixed costs. Find the variable price for each unit. Multiply the variable cost average by the number of produced items, then add the fixed costs. Fixed costs can be done automatically using accounting software.

How do I find the cost function?

Here are the steps you can take to find the cost function: 1. Find fixed costs First, track your fixed costs. If you have an income statement or accounting software, you may be able to find your fixed costs as a budget line. If not, you can calculate your own fixed costs by adding all the items that don’t fluctuate depending on your quantities.

How does management use the cost function equation?

Management uses this model to run different production scenarios and help predict what the total cost would be to produce a product at different levels of output. The cost function equation is expressed as C (x)= FC + V (x), where C equals total production cost, FC is total fixed costs, V is variable cost and x is the number of units.

What is a cost function equation?

The cost function equation is expressed as C (x)= FC + V (x), where C equals total production cost, FC is total fixed costs, V is variable cost and x is the number of units. Understanding a firm’s cost function is helpful in the budgeting process because it helps management understand the cost behavior of a product.