If you’re currently in business, you need a good way to manage costs. While using accounting software is the best method for managing costs, even if you’re still recording transactions in a manual ledger or using a spreadsheet application, you can learn to manage business costs properly.

Managing your costs is doubly important if you own a manufacturing business, since you’ll need to manage both product and period costs. Product costs, also known as direct costs or inventoriable costs, are directly related to production output and are used to calculate the cost of goods sold.

On the other hand, period costs are considered indirect costs or overhead costs, and while they play an important role in your business, they are not directly tied to production levels.

Both product costs and period costs directly affect your balance sheet and income statement, but they are handled in different ways. Product costs are always considered variable costs, as they rise and fall according to production levels.

Product and period costs are two types of business expenses that are categorized and accounted for differently. It’s important for companies to understand the key differences between product and period costs in order to properly record them in their bookkeeping and financial statements. This article answers some of the most frequently asked questions about product costs vs period costs.

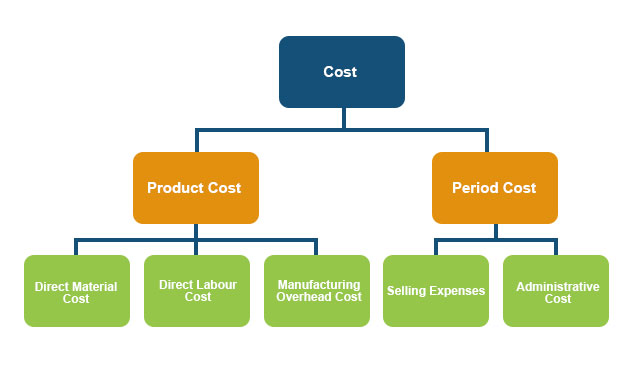

What are product costs?

Product costs are expenses directly related to manufacturing or purchasing goods that will be sold. They are also known as inventoriable costs since they are capitalized into inventory until the inventory is sold. The three components of product costs are:

- Direct materials – Raw materials that go into creating a product, like fabric used to make clothes.

- Direct labor – Wages paid to employees who work directly on producing the product, like factory workers.

- Manufacturing overhead – Indirect production costs like rent, utilities, equipment maintenance, and supervision.

Product costs attach to the units produced and become expenses only when those units are sold. On the financial statements product costs start in the inventory asset account and are shifted to cost of goods sold when inventory is sold.

What are period costs?

Period costs are expenses related to business operations during an accounting period rather than production. Common examples include:

- Selling expenses – Marketing, advertising, sales commissions

- General and administrative expenses – Office salaries, utilities, insurance, accounting fees

- Other expenses – Rent, interest, legal fees

Unlike product costs, period costs cannot be tied to production. They are recorded as expenses in the period they are incurred rather than inventory. On the financial statements, period costs are recorded just in the expense accounts, not inventory.

Why is it important to distinguish between product and period costs?

Properly categorizing costs is crucial for accurate financial reporting, Putting a period cost into inventory overstates assets on the balance sheet, Expensing a product cost immediately understates net income on the income statement Distinguishing product vs period costs also helps businesses understand their cost structure and make better decisions

How can you tell if a cost is a product cost or period cost?

There are two tests to distinguish product vs period costs:

Traceability test – If a cost is directly traceable to a physical unit of product, it is a product cost. For example, fabric used to make dresses can be traced to each dress produced.

Allocability test – If a cost cannot be traced but can be allocated to products based on a reasonable metric, it is also a product cost. For example, rent for a factory cannot be traced but can be allocated to each unit produced.

Any cost that fails both tests is a period cost. For instance, marketing expenses cannot be traced or reasonably allocated to individual units produced.

How are product costs reported on financial statements?

Product costs become expenses on the income statement when inventory is sold as cost of goods sold. Until inventory is sold, product costs appear on the balance sheet in the inventory asset account. The inventory asset is decreased through cost of goods sold expense as units are sold.

For example:

- A manufacturer spends $100,000 on materials, labor, and overhead to produce 10,000 units of inventory. Each unit has $10 of product costs attached to it.

- The $100,000 product cost is recorded in the inventory asset account. No expense yet.

- 5,000 units are sold for $50,000. Cost of goods sold is $50,000 (5,000 units x $10 product cost per unit).

- Inventory is now 5,000 units at $50,000. The asset is decreased as product costs expense on the income statement.

When are period costs reported on financial statements?

Period costs are recorded as expenses on the income statement in the period they are incurred. For example, if a company spends $20,000 on advertising in May, the $20,000 advertising expense is recorded in May even if no sales happen yet. Period costs do not flow through inventory like product costs.

Can period costs become assets?

Typically no, but prepaid period costs are an exception. For example, if a 12-month insurance policy is paid upfront, the prepayment is initially recorded as a prepaid insurance asset. As each month passes, 1/12th of the cost is reclassified from the asset to insurance expense on the income statement.

Are all manufacturing costs product costs?

Not always. Some manufacturing overhead costs may be period costs if they cannot be reasonably allocated to production. For example, the salary of a factory supervisor is usually considered a product cost. But the salary of a company VP who oversees several factories may be a period cost since allocating it to units at specific factories is difficult.

When does cost of goods sold appear on financial statements?

Cost of goods sold is recorded on the income statement whenever inventory is sold. It transfers the costs that were attached to the inventory units to expense. The timing matches expense recognition with related revenues.

Cost of goods sold also appears on the statement of cash flows as a deduction from net income to arrive at operating cash flow. However, it is not considered a true cash outlay since the original product costs were already paid for in prior periods.

Is cost of goods sold an asset?

No, cost of goods sold is an expense account, not an asset account. The product costs were assets when they were still attached to inventory. Cost of goods sold recognizes these costs as expenses as the benefits of the inventory are used up through sales.

Can selling costs be product costs?

Usually not. Most selling costs are period costs by nature. However, some selling costs may be product costs in certain industries like car manufacturing. For example, portion of car salesperson commissions could be considered product costs at auto dealers since the salespeople directly assist buyers in selecting manufactured products. The commissions relate to the specific cars sold.

Can general and administrative costs ever be product costs?

In most cases, G&A costs are period costs. However, an exception is if the G&A department directly benefits or supports the manufacturing process. For example, the G&A department handling factory paperwork may be considered a product cost. But G&A expenses without a strong connection to production units are period costs.

Takeaway

- Product costs attach to inventory and only become expenses upon sale. Period costs directly expense in the period incurred.

- Properly distinguishing between product vs period costs is crucial for accurate financial statements.

- Traceability and allocability determine if a cost is a product cost or period cost.

- Product costs report through inventory and cost of goods sold. Period costs report directly to expense accounts.

Accurately categorizing product and period costs according to these guidelines helps ensure a company’s financial reporting matches GAAP standards. It also provides useful insight into the cost structure of the business.

Product vs. period costs: What’s the difference?

Product costs are always related to production, with period costs being considered indirect or overhead costs. Think of it like this: If you stop production for a month, no product costs will be incurred.

However, you’ll still have to pay the rent on the building, pay your insurance and property taxes, and pay salespeople that sell the products currently in inventory.

The table below highlights some of the differences between product costs and period costs:

| Product Costs | Period Costs |

|---|---|

| Always related to the manufacturing process | Not affected by production levels |

| Related to volume, such as units produced or labor hours | Related to overhead and indirect costs |

| Always variable, depending on production levels | Usually fixed, but can also be semi-variable |

| Include labor, materials, supplies, and factory overhead | Includes administrative, sales, and distribution costs |

| Are recorded on a balance sheet | Are recorded on an income statement |

Final thoughts on product and period costs

Product and period costs are incurred in the production and selling of a product.

By separating these two very different cost types, you can more easily identify potential problem areas in production, such as inefficient labor, inferior machinery, or outdated procedures, while also reviewing production costs, such as raw materials and direct labor.

You’ll also be able to spot trouble spots or overspending in administrative areas or if overhead has ballooned in recent months.

Though it may be tempting to just lump your expenses together, there are three great reasons why you need to separate product and period costs for your business.

Because product and period costs directly impact your financial statements, you need to properly categorize and record these costs in order to ensure accurate financial statements.

Speaking of financial statements, it’s important that you take the time to review your financial statements on a regular basis. As an owner, you rely on their accuracy to make key management decisions. This can be particularly important for small business owners, who have less room for error. If product and period costs are overstated or understated, or not recorded at all, your financial statements will be wrong as well.

Product vs. Period Cost

What is the difference between product costs and period costs?

Product costs are those directly related to the production of a product or service intended for sale. Period costs are all other indirect costs that are incurred in production. Overhead and sales and marketing expenses are common examples of period costs. Product costs are the direct costs involved in producing a product.

Are all costs incurred by a company a period cost?

In short, all costs that are not involved in the production of a product (product costs) are period costs. All costs incurred by a company are either period costs or product costs. Additionally, the two types of costs are recorded differently. See the table below for more comparison:

What is a period cost in accounting?

Period costs are not assigned to one particular product or the cost of inventory like product costs. Therefore, period costs are listed as an expense in the accounting period in which they occurred. Other examples of period costs include marketing expenses, rent (not directly tied to a production facility), office depreciation , and indirect labor.

When are product costs not expensed?

Product costs (direct materials, direct labor and overhead) are not expensed until the item is sold when the product costs are recorded as cost of goods sold. Period costs are selling and administrative expenses, not related to creating a product, that are shown in the income statement in the period in which they are incurred.